& meet dozens of singles today!

User blogs

Ireland’s technology scene has come in leaps and bounds in the last decade, with a growing VC scene, plenty of startups and tech giants attracted by the nation’s favorable tax incentives and talent pool.

Google, Facebook, Slack, Microsoft and Dropbox each have a European headquarters sited in Dublin. As the EU’s only remaining English-language speaking hub, Ireland is attracting more diversity in its founders than ever before, plus the tech diaspora is returning to its roots as the ecosystem matures.

We surveyed five local VCs to find out if they had any wisdom to share with TechCrunch readers who are considering hiring, investing or founding a company in Ireland this year.

VCs in Ireland don’t stray far from home, but there are plenty of great deals to be had there anyway. A small domestic market means Irish startups think internationally from launch, and there are high-quality seed opportunities. Top-tier American VCs like Sequoia are placing bets on Irish companies, sometimes even at a pre-seed stage.

The coronavirus pandemic has not really impacted many investment strategies — aside from the switch to Zoom calls instead of meet-and-greets — but it has made hiring more challenging, given the competitiveness of the local labor market. Still, top engineering talent is cheaper there than in the U.S., which means entrepreneurs can create great companies with less overhead.

We just launched Extra Crunch in Ireland. Subscribe for access to all of our investor surveys, company profiles and other insider coverage for startups everywhere. Save 25% off the cost of a one-year Extra Crunch membership by entering discount code IRISHCRUNCH.

We spoke with the following investors:

- Andrew O’Neill, principal, Act Venture Capital

- Isabelle O’Keeffe, principal, Sure Valley Ventures

- Nicola McClafferty, partner, Draper Esprit

- Michelle Dervan, partner, Rethink Education Management, LLC

- Will Prendergast, partner, Frontline Ventures

Andrew O’Neill, principal, Act Venture Capital

What trends are you most excited about investing in, generally?

We are seeing high-quality seed opportunities that are leading with exciting developer-first/bottoms-up go-to-market strategies in both security and enterprise software. The shift left in security is very well-publicized, but we feel the cultural element of developers truly caring about security and implementing it at design phase is still only beginning … and it’s hugely exciting.

What’s your latest, most exciting investment?

It’s a B2B SaaS design tool, in the world of Figma, Sketch and Invision App … and has some very interesting angels. It is only just complete and not announced yet … and we have not talked to any PR agencies yet, but would be happy to pitch an exclusive to you ;)

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

As a domestic market, Ireland is very small … so by its very nature, we do not see the same level of great B2C as the U.K. The expertise … and second, third-time consumer-tech founders are not as common, but there are still of course huge opportunities in the consumer space and companies like Buymie are proving it can be done in Ireland.

What are you looking for in your next investment, in general?

Like every investment: The people that truly understand the pain point, have passion around the product, have the patience and grit to keep going, and finally the potential for this company to become a category creator.

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

No competition means no market … however there are high volumes of startups empowering remote working, productivity tools and HR tech focused around company culture metrics etc. … but that said, there is a wave of change happening around the future of work that no one has a crystal ball on, and new category winners will still emerge.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

Very focused on Ireland and more than 50% … we can invest in Series A and B across Europe, but we invest at seed exclusively in Ireland.

Which industries in your city and region seem well-positioned to thrive, or not, long term? What are companies you are excited about (your portfolio or not), which founders?

Enterprise software startups have always been well-positioned for success within Ireland, and that has only increased with the secondary effects now appearing from the result of great talent coming out of large MNCs driven by 20+ years of FDI. Act has invested in over 120 companies and over half is in enterprise software. We are excited about seeing a new emerging amount of repeat founders in our portfolio (and Ireland) like Barry Lunn in Provizio, and Cathal McGloin in ServisBOT.

How should investors in other cities think about the overall investment climate and opportunities in your city?

When we looked at all the data in Ireland recently, there has been a 115% increase from €401 million to €860 million invested per annum over the last four years. So the market size has doubled and we are seeing some very exciting seed companies, which bides very well for the future.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

Personally, I do expect to see even more great startups coming out of the south like Cork and Limerick and the west in Galway, but I don’t foresee startup hubs significantly losing people due to the pandemic and remote work.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19?

It’s obvious that there are now serious questions around the level of future of business travel, given how people have been forced to rethink and adapt how they do business. This industry shift alone will create both big winners and losers long term.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

Not hugely, given the long-term timeframe we consider when investing. The bigger question around changing consumer behaviors, the acceleration of e-commerce adoption and digital transformation is something we are of course taking into account. Our advice is always bespoke and contextual to the individual startup, and only given when asked.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Yes, our portfolio has proven itself to be quite robust through COVID and companies like SilverCloud Health, Toothpic and Buymie are experiencing great tailwinds due to the current pandemic environment.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

Personally, seeing some incredibly talented founders with deep expertise at seed stage that are repeat founders. They know exactly what they want and need to do to go bigger this time around, and we believe they can get there much quicker than before.

Isabelle O’Keeffe, principal, Sure Valley Ventures

What trends are you most excited about investing in, generally?

AI/ML, cybersecurity, immersive technologies and gaming infrastructure.

What’s your latest, most exciting investment?

Getvisbility and Volograms.

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now? What are you looking for in your next investment, in general?

Companies that are really creating defensibility using the technology. Companies creating new markets.

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

Ride-sharing, on-demand delivery, payments and challenger banks.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

We invest more than 50% in our local ecosystem versus other startup hubs.

Which industries in your city and region seem well-positioned to thrive, or not, long term? What are companies you are excited about (your portfolio or not), which founders?

The industries that will continue to thrive include: financial services, property and construction, pharmaceuticals, manufacturing and Big Tech. We’re very excited about some of our portfolio companies including VividQ, Admix, Buymie, Nova Leah and WarDucks.

How should investors in other cities think about the overall investment climate and opportunities in your city?

Dublin and Ireland have a growing and prosperous tech ecosystem and there are plenty of great investment opportunities there.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

Yes I would agree that we will see some of this happening. However, I do think that once there is a vaccine that we will see the return of cities and people will naturally be attracted back there.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

We have seen limited impact of COVID on some of segments that we invest into. The opportunities exist for companies operating in the future or work including remote working, e-commerce, on-demand grocery delivery, cybersecurity, gaming and immersive technologies.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

COVID has not really impacted our investment strategy bar the fact that we have had to get comfortable with a lot of the process being conducted via Zoom. We have not shifted away from certain sectors or industries as we have tended to invest into areas that are relatively unaffected. The biggest worries for founders in our portfolio are around raising their next round of funding, hitting key milestones, achieving a repeatable go-to-market strategy and hiring great talent.

My advice to startups in my portfolio now is to keep a very close eye on burn, ensure that if they are going out to fundraise that they realize it can take at least two months longer than they originally anticipated and to continue to be working on the product and technology at times when sales have slowed down as when they emerge from this period they will be in a much stronger position with their products and technology and the sales will follow.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Yes we have “green shoots’ regarding momentum in Buymie, which is an “on-demand grocery delivery” company who have seen a surge in demand for the service due to the pandemic. Getvisibility, which is a cybersecurity company, has also seen a surge in interest from companies in the financial services, and pharmaceutical and defense industries as they adapt to their employees working from home and where there are greater risks of cyberattacks.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

I think the moment for everyone recently has been the announcement that we could be closer to a vaccine than we originally thought and that we may be able to resume normal life next year.

Nicola McClafferty, partner, Draper Esprit

What trends are you most excited about investing in, generally?

Future of work/consumerization of enterprise, machine-learning applications.

What’s your latest, most exciting investment?

Sweepr — automation of customer care for connected homes.

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

True AI, digital health.

What are you looking for in your next investment, in general?

Global ambition.

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

E-scooters.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

~20%.

Which industries in your city and region seem well-positioned to thrive, or not, long term? What are companies you are excited about (your portfolio or not), which founders?

Software application, AI, machine learning, life sciences. key companies, WorkVivo, Manna Aero, Open, Sweepr, Roomex and Evervault.

How should investors in other cities think about the overall investment climate and opportunities in your city?

Unfortunately seed stage is dramatically underserved by local players. Hiring can be challenging given competitiveness of labor market with large tech MNCs. However deep entrepreneurship culture, global thinking from day one, incredibly strong pool of technical talent from Irish universities. It’s also a key destination of other European founders. Brexit opens even more opportunity for this.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

Startup economy will likely become a bit more distributed around the country but this will be a positive. Cities like Dublin, Cork and Galway will however remain strong hubs.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

Travel tech extremely challenged but the best companies will survive and huge winners will emerge in the COVID recovery when travel returns. Big opportunity to accelerate enterprise SaaS adoption and automation as budgets have shifted dramatically to digital infrastructure and cost-cutting and productivity becomes key focus.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

Strategy remains largely intact with some further reserves used to support companies. For those businesses very directly impacted (e.g., travel) — concern is visibility and timing of recovery that is largely out of founder control. Other concerns include cash runway in times of uncertainty — how will the market view performance for future fundraise; in big enterprise how to adapt your sales model for a remote world.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Most definitely. As tech businesses most have been very adaptable and are responding to customer needs as they change. After a slow Q2 many businesses rebounded very well in Q3 and have returned to strong growth. Early churn has been flushed out already.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

Announcement of the vaccine! Path to recovery is nearing.

Michelle Dervan, partner, Rethink Education Management, LLC

What trends are you most excited about investing in, generally?

I am deeply specialized in education technology investing. Interested in seeing tailored Zoom alternatives for the classroom, tech-enabled vocational training programs, corporate learning solutions for the distributed workforce.

What’s your latest, most exciting investment?

Crehana, an online skills training platform serving Latin America.

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

Upskilling and reskilling programs for displaced workers.

Shorter, cheaper training programs and credentialing for middle-skills jobs.

Software to help high school students prep for college and career.

Effective remediation programs that can help students catch up on lost learning during COVID.

What are you looking for in your next investment, in general?

Outliers in terms of evidence of product market fit, proof of efficacy, impact baked into the business model, team with unique understanding of the problem and ability to execute against it.

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

K-12 supplemental apps, games, content.

Tech bootcamps.

Corporate LMS.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

80% U.S.-focused, 20% outside of the U.S.

Which industries in your city and region seem well-positioned to thrive, or not, long term? What are companies you are excited about (your portfolio or not), which founders?

Ireland has traditionally had a very strong e-learning/edtech startup sector. Exciting growth companies include LearnIpon, Learnosity, Alison, Touch Press. Early-stage companies include Avail Support, Zhrum, Robotify.

How should investors in other cities think about the overall investment climate and opportunities in your city?

Dublin is a really vibrant startup ecosystem. Young population. Lots of government supports to encourage entrepreneurship. Excellent experienced talent pool coming out of multinationals and existing startups. English speaking. Great connectivity to rest of Europe/U.S.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

I recently relocated to Dublin after 10 years in NYC. There has been a mass exodus from cities like NYC and SF during the pandemic as the economics of living there plus the space constraints, etc. no longer make sense in a prolonged period of WFH and while most amenities are closed. Dublin is also a high-cost location so will likely also see some exodus although I think to a lesser extent.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

The COVID environment has caused a mass acceleration in the adoption of education technology across all age groups from K-12, higher education to corporate and workforce learning. This was already a secular trend albeit at a much slower pace of adoption. I believe that the prolonged period of reliance on a tech-enabled learning experience and the potential need to revert to this in the future will have a lasting effect on how we teach and learn.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

Our investment strategy has not been impacted by COVID. We are seeing a greater degree of opportunity and interest in our sector. The biggest concerns for founders are unpredictability in the sales funnel, potential delays to purchasing decisions and resultant cashflow implications. Even for companies that have been net beneficiaries of the COVID environment, it has injected a very high degree of unpredictability and that is very stressful for founders.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Yes, as mentioned above.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

Biden’s election and the list of people that he is evaluating for Education Secretary and for his cabinet.

Will Prendergast, partner, Frontline Ventures

What trends are you most excited about investing in, generally?

We take an opportunistic approach to investing at Frontline and are open to any number of different trends within the B2B space. Generally, we are excited to back founders working on:

- Complexity in the software/product development stack: As more and more businesses become software businesses and software products become more complex there will be a layer of tools that abstract away that complexity and provide connections between them. Software using other software will be an exciting space in the decade to come, facilitated by many API-first companies.

- Embedded finance: We are excited by fintechs that are helping non-financial institutions leverage their customer base to provide financial products. Open banking is an enormous enabler of embedded finance.

- Process augmentation rather than process automation: There are a number of key skill gaps emerging in many different sectors right now and software is emerging as the bridge for companies to handle the shortfall. These are products that help highly skilled workers maximize their productivity.

In the current environment, we are also highly interested in startups that are broadly targeting the key trends below brought on by COVID-19:

- Hospitals and clinics seek to increase efficiency and reach patients remotely.

- Banks cautious as financial crime grows.

- Remote employee management tools for HR and finance teams.

- Debt collection automation due to SME liquidations.

What’s your latest, most exciting investment?

We recently invested in a German business that aims to become the Moody’s of financial crime.

Since 2008, large banks have become less willing to transact with regional retail banks. They were unfairly deemed “too risky” in their portfolio. This company aims to create a fundamental shift in the industry — from old school box ticking compliance to data-driven ways of determining the risk. We are very excited to increase fairness and transparency between banks, which will inevitably create more value to the end consumer.

Are there startups that you wish you would see in the industry but don’t? What are some overlooked opportunities right now?

B2B payments are undergoing a renaissance at the moment with companies like Bill.com dominating in the public markets. As fintech creeps into more aspects of the product stack, payments is just the first part to produce huge winners. Solving the nuts and bolts of business finance is still a hugely overlooked opportunity for both large and small companies.

We’d also love to see more companies dedicated to reducing the CFO burden at SME and enterprise level. From real-time payroll to treasury and employee pension management, so much of a CFO’s work is manual and time consuming.

We have supported companies that make a significant dent in the specific parts of the funnel (for example, Payslip — a global payroll automation platform), but we feel like there is more room for end-to-end automation in this realm.

What are you looking for in your next investment, in general?

We’re looking for challengers who seek out other strong minds; whether you’re a first-time founder building something that matters, or a seasoned entrepreneur that knows how hard it is to “make it.” In all of our investments, we prize self-awareness above all else in our founders; key to building great teams and scaling a global business. Ambition does not require experience. We’re looking to invest in pioneers across Europe from the world of tech, computer science and engineering, due to our own deep knowledge of technology. In return, we use our personal experience in building and scaling business across both sides of the Atlantic to help founders get off the ground — and go global.

Which areas are either oversaturated or would be too hard to compete in at this point for a new startup? What other types of products/services are you wary or concerned about?

Products that are being built specifically with the conditions created by COVID-19 today may find themselves in a wildly different environment in 18 months. We’re looking to speak to founders who see how things are now and have a strong opinion on how they’re going to affect things in the years to come.

How much are you focused on investing in your local ecosystem versus other startup hubs (or everywhere) in general? More than 50%? Less?

We support founders with global ambition across both sides of the Atlantic. Frontline Seed is a pan-European early-stage fund investing all across Europe. Frontline X is a growth-stage fund, for fast and frictionless U.S.-Europe expansion.

When we first started Frontline, the vast majority of our investments came out of Ireland. Since 2012 we have expanded our scope, and for the last few years have been very much pan-European and now invest across Ireland, the U.K., Germany, the Netherlands and Southern Europe.

Which industries in your city and region seem well-positioned to thrive, or not, long term? What are companies you are excited about (your portfolio or not), which founders?

U.S. tech companies like Amazon, Facebook, Google, Zendesk Hubspot (among many others) have a “pied-à-terre” in Ireland.

In most cases, top-class engineering talent is sourced more cheaply there than in the U.S., creating a self-fulfilling prophecy. They upskill great engineers, who then go on to create great companies.

We’ve seen startup developer tools thrive in Ireland as a result; an example of which is Tines.io. This Accel-and-Index-backed company was built by the world-renowned security team in Dublin.

How should investors in other cities think about the overall investment climate and opportunities in your city?

Ireland is a hidden gem — we’ve had the privilege of reaping the rewards. However, I suspect that the likes of Tines.io, Intercom and Stripe are stirring investor curiosity.

We’re already seeing top-tier U.S. VCs like Sequoia placing bets in Irish companies at a pre-seed stage, for example Evervault, one of our portfolio companies.

Do you expect to see a surge in more founders coming from geographies outside major cities in the years to come, with startup hubs losing people due to the pandemic and lingering concerns, plus the attraction of remote work?

As a global fund, part of our core belief is that great companies and exceptional founders can come from anywhere in the world. COVID-19 has had a significant and eroding effect on traditional “tech hub” models and we have seen founders of all walks of life realize that companies can not only run, but thrive in a remote world.

That said, we also believe that geography will continue to matter. Where you set up your HQ in Europe as a growth-stage B2B SaaS business expanding from the U.S. (for example) will continue to matter in a post-COVID world — because legal entities will continue to matter.

Which industry segments that you invest in look weaker or more exposed to potential shifts in consumer and business behavior because of COVID-19? What are the opportunities startups may be able to tap into during these unprecedented times?

- The closure of retail stores = tremendous growth in e-commerce. Companies big and small are vamping up their back and front ends, and attempting to get more visibility on their supply chain for better customer service.

- Payments transition online = more financial crime. Banks need tools that help them detect fraud.

- Consumers are tight on cash = HR departments want to provide more salary liquidity and help employees save for their pensions to create better financial wellness.

These are just to name a few.

How has COVID-19 impacted your investment strategy? What are the biggest worries of the founders in your portfolio? What is your advice to startups in your portfolio right now?

COVID-19 has not changed our investment strategy but it will have lasting impact on the way businesses are run and built. That said, the pandemic has given us a new filter: “How successful can this product/business model be in a post-COVID world?”

At the moment, our founders are most worried by engagement (maintaining company culture) and talent (team expansion, senior leadership recruitment).

Every company is different and we shy away from blanket statements, but what we do advise is that founders spend time to identify what working format works best for their company and that they listen carefully to their employees. How can you continue to grow your business, whilst maintaining and nurturing an inclusive and engaged company culture?

Also — while you can, shore up your balance sheet. Believe it or not, VC funding was at an all-time high in Europe last quarter. Go fundraise to extend your runway as much as possible. No one really knows what the next 12 months is really going to hold.

Are you seeing “green shoots” regarding revenue growth, retention or other momentum in your portfolio as they adapt to the pandemic?

Three companies in our portfolio stand out as pandemic green shoots:

- Workvivo is designed to promote team culture and communication digitally. They have successfully raised a Series A midpandemic with U.S. investor Tiger Global to cope with demand from large customers.

- Qualio is another portfolio company selling quality management software into life sciences and pharmaceutical companies. They blew out their Q2 targets and raised an $11 million Series A.

- Signal AI: Media monitoring is an attractive proposition to PR and comms teams in turbulent times. Signal AI has recently partnered with Deloitte to produce COVID-19 curated reports on how the pandemic has and is continuing to affect supply chains, business, society and travel.

What is a moment that has given you hope in the last month or so? This can be professional, personal or a mix of the two.

Seeing how well the many teams in our portfolio focused on employee health, well-being and safety and how hard they have all worked to keep their companies going strong.

Source: https://techcrunch.com/2021/01/29/despite-brexit-and-covid-19-irish-investors-remain-bullish/

Earlier this week, Science Inc, the 10-year-old, L.A.-based incubator and venture firm, rolled out a blank-check company onto the Nasdaq, raising $270 million for what firm founders Peter Pham and Mike Jones say will be used to take public a company in the mobile, entertainment or direct-to-consumer service space — or maybe one that combines all three.

If they have one of their own portfolio companies in mind to take public, they wouldn’t say in conversation yesterday. Science would have some interesting candidates from which to choose if so. It helped incubate the amateur esports platform PlayVS after Pham met its founder, Delane Parnell, on a dance floor at a South by Southwest festival. It’s also an investor in Bird, the micro-mobility company that is reportedly working with Credit Suisse to strike a deal with a blank-check company. And it helped create and grow Liquid Death, a company with a tongue-in-cheek marketing strategy that’s selling mountain water in aluminum cans — a lot of it, says Pham.

Indeed, we spent much of our time with the duo talking about how to create a powerful consumer brand in 2021 when so many are vying for attention over the same, saturated platforms. More from that talk follows, edited lightly for length and clarity.

TC: You have this new blank-check company. You’re about to start talking with potential targets. Will you consider a company that you’ve incubated or else funded at Science?

MJ: No. So the SPAC is an independent entity. We think that there’s a universe of well over 100 companies that would fit the credentials of what we’re looking for within the stack. Some of those companies, we may or may not have investment exposure [to them], but the process of analysis is independent of the Science portfolio.

TC: So you wouldn’t rule it out.

MJ: We have independent directors. So there’s a different process that would go through if we were looking at a company in the portfolio. But right now we’re just aggregating the right universe of potential targets. And then we’ll go through a formal process on it.

TC: What are the metrics you want to see? You are specialists, including in direct-to-consumer companies. Do the companies that you’re targeting have to be profitable?

MJ: When we look at the different, potential companies that we’re interested in, we’re not saying that they have to have some specific level of profitability or specific level of revenue . . . We don’t expose the the core metrics and revenue drivers that we think make for successful companies within sectors. But we’re a super data-focused team. We’re very much on the forefront of next-generation Gen Z and millennial-oriented marketing. And there are very specific things we look for that we think may build breakout brands.

TC: Both of you know the social media space. There are new social media plays that are gaining a lot of attention, such as Clubhouse. Back to your core business at Science, are there any investments in those areas in that area that you’re looking at?

PP: A decade ago is when YouTube became a platform for marketing. Then six of seven years ago, Instagram [became a platform for marketing]. And then Snapchat came along, and then all of a sudden Instagram stories [emerged], and then TikTok and now another platform, which is Clubhouse. There’s always something new coming around the corner.

You can’t take your eye off of Facebook, Instagram, and Snapchat, but Clubhouse is real. It’s almost radio, but it’s participatory. If you go to South by Southwest, it’s almost like SWSX panels around the clock. There’s this really interesting dynamic where you could be in crowd, raise your hand, and if they pull you up on stage, now you’re part of the panel. That’s why a lot of people are there — for the chance of getting discovered [and] the chance of letting their voice be heard by a larger audience.

TC: What makes you think its growth is sustainable?

PP: The moment marketers join a platform [you know]. When real marketers, people who are selling classes on how to make money, how to have real estate, how to make money [selling] real estate, that type of marketing — when [they show up], it’s an arbitrage. It’s basically very smart people who make a lot of money realizing for that every minute they spend doing this, it’s more valuable in terms of ROI, customer acquisition cost, and revenue, than spending time on this other thing that everyone else is on.

TC: How do your portfolio companies use these platforms in 2021? You are investors in Liquid Death. You helped incubate MeUndies, a subscription underwear company that raised saw $40 million late last year. You were involved in the early days of Dollar Shave Club. How do you break through the noise with things like water, underwear and razors?

PP: Platforms are always just a springboard. You can’t rely on these places long term because the rules of the game change, the feed changes. Ten years ago, when we launched Dollar Shave Club, we had on the homepage an autoplay of this YouTube video that was just about driving customers to buy something. At the time, no one thought about posting YouTube videos to get somebody to buy something. MeUndies [used] Instagram. Who would imagine subscription underwear? But every month, there’s a holiday — Christmas, New Year’s, Valentine’s Day, St. Patrick’s Day. What if there was something interesting and fun that you could wear?

With Liquid Death, it’s still very much [focused on] Instagram and now probably TikTok. But in all cases, the brand has to be worthy for somebody to talk about what’s interesting about it and even to defend it.

Mike underplays our data side, but we measure incessantly everything that’s happening in terms of the each one of our businesses, including their social reach, their engagements, business retention, how often customers are coming back, how much revenue we’re generating from each individual, what each piece of marketing is worth. All of these tie into this complex engine that [helps us determine], is there a business behind this thing? Can it grow on its own without a reliance on Facebook? With most companies, if you don’t understand how to build your own community, your own brand, and your own audience, ultimately the winner on the back end is Google or Facebook.

TC: How do you build that community right now?

I’ve handed out 4,000 cans personally. In the early days of Liquid Death, I just remember handing it to a bunch of teenagers, and six out of 10 would take a photo and Snap it to their friend. It was just this instant moment I kept seeing over and over, and I just knew, this is gonna work. If you noticed in March and April and May how boring your Instagram feed was, [it was] because everyone was staying home and there was nothing to do. But we [had this insight to] give somebody a piece of content.

TC: Liquid Death is now available in some stores, including 7-Elevens. Are people buying the water online? What percentage of them buy it through a subscription?

PP: One third of our customers who buy online [at the site] buy merchandise. They’re buying $24 hats, $45 hoodies — we’re selling out merch constantly. It’s the brand, it’s a lifestyle. Mike Cessario, the CEO, says he’s building something that’s like your favorite band. The product lets you be a fan of the thing [including] because it’s not a piece of plastic that’s going to go the ocean [like other water bottles]. It’s not sugar. It’s not alcohol that might result in a drunk driving incident.

It’s flair. It’s a reason to say hi to somebody. It’s an icebreaker. It’s fun. It’s irreverent. It’s dumb. It’s funny. It’s everything to everybody, but something worthy to talk about, something to look at.

The trajectory we’re on is hard to measure, You have to see it, and when you see it over and over, it’s obvious.

Robinhood caps a wild week for new funding, Coinbase is going public and Johnson & Johnson reveals new vaccine trial data. This is your Daily Crunch for January 29, 2021.

The big story: Robinhood raises $1B

I know the newsletter has been dominated by Robinhood and stock market news for the past few days but, well, so have the headlines.

The latest news is that after reportedly tapping its credit lines, Robinhood raised $1 billion in new funding from existing investors. It seems the company needed the money in order to meet regulatory minimums and other requirements tied to users’ trading activity.

Meanwhile, the SEC has issued a statement that doesn’t specifically mention Robinhood or GameStop by name, but it says that “extreme stock price volatility has the potential to expose investors to rapid and severe losses” that could “undermine market confidence.”

The tech giants

You can now give Facebook’s Oversight Board feedback on the decision to suspend Trump — The board says the point of the public comment process is to incorporate “diverse perspectives” from third parties who wish to share research that might inform their decisions.

Uber’s Autocab acquisition gets eyed by UK competition watchdog — Autocab makes booking and dispatch software for the taxi and private-hire vehicle industry.

Startups, funding and venture capital

Coinbase is going public via direct listing — The company has raised over $540 million in funding as a private company.

Firehawk Aerospace extends seed funding to $2.5M with $1.2M from Harlow Capital — Firehawk has developed a new kind of hybrid rocket fuel that greatly enhances rocket launch safety, cost and transportation using additive manufacturing.

SoftBank earmarks $100M for Miami-based startups — The fund will back companies that are in Miami or plan to move there.

Advice and analysis from Extra Crunch

Customer advisory boards are a gold mine for startup brand champions — Some considerations to make certain your customer advisory board is a success.

Rising African venture investment powers fintech, clean tech bets in 2020 — The Exchange looks at a report from Briter Bridges, a research group that focuses on Africa’s private capital market.

Subscription-based pricing is dead: Smart SaaS companies are shifting to usage-based models — That’s according to Open VP of Growth Kyle Povar.

(Extra Crunch is our membership program, which helps founders and startup teams get ahead. You can sign up here.)

Everything else

Johnson & Johnson’s COVID-19 vaccine is 85% effective against severe cases, and 66% effective overall per trial data — Johnson & Johnson’s vaccine is a single shot rather than a two-course treatment.

‘Frozen’ CG snow and crash-test cadavers offer hints for 60-year-old Russian mystery deaths — New research uses simulation techniques from multiple eras to advance what is perhaps the least implausible explanation for a tragic mystery.

Reap big benefits when you attend both TC Early Stage 2021 events — TechCrunch Early Stage is a two-day virtual bootcamp that gives early founders access to leading experts.

The Daily Crunch is TechCrunch’s roundup of our biggest and most important stories. If you’d like to get this delivered to your inbox every day at around 3pm Pacific, you can subscribe here.

Source: https://techcrunch.com/2021/01/29/daily-crunch-robinhood-raises-1b/

Robinhood has detailed its latest step in the complex quagmire of market manipulation that is this week’s GameStop hedge fund Reddit army debacle. Users will for the present be limited to holding a single share of GameStop and dozens of other stocks.

Several stocks were limited to five shares, and options contracts are likewise limited on many of the most-traded stocks this week, such as AMC and Blackberry. Positions exceeding these amounts will not be automatically sold, but they will apply if the user goes under them and tries to buy again. Fractional shares are also prohibited.

Any other specifics about positions, expiring options contracts and so on can be found in the announcement and related FAQs.

Robinhood has said that it has halted and now limited trading because of “financial requirements, including SEC net capital obligations and clearinghouse deposits” — essentially, the volume and value of the trading going on was beyond its ability to legally or realistically cover. Trading of certain stocks was halted or restricted earlier this week, but the new post details exactly which stocks are affected and how.

The company had to hastily raise funds totaling over a billion dollars from its existing investors after reportedly maxing out half a billion in credit lines.

With widespread outrage at the handling of the situation and the U.S. government taking notice, it’s unlikely Robinhood’s troubles (not to mention other trading apps and platforms) are anywhere near over. With new developments appearing seemingly every few hours, it’s hard to know how this particular story will develop.

Edtech is so widespread, we already need more consumer-friendly nomenclature to describe the products, services and tools it encompasses.

I know someone who reads stories to their grandchildren on two continents via Zoom each weekend. Is that “edtech?”

Similarly, many Netflix subscribers sought out online chess instructors after watching “The Queen’s Gambit,” but I doubt if they all ran searches for “remote learning” first.

Edtech needs to reach beyond underfunded public school systems to become more sustainable, which is why more investors and founders are focusing on lifelong learning.

Besides serving traditional students with field trips and art classes, a maturing sector is now branching out to offer software tutors, cooking classes and singing lessons.

For our latest investor survey, Natasha Mascarenhas polled 13 edtech VCs to learn more about how “employer-led up-skilling and a renewed interest in self-improvement” is expanding the sector’s TAM.

Here’s who she spoke to:

- Deborah Quazzo, managing partner, GSV Ventures

- Ashley Bittner, founding partner, Firework Ventures (a future of work fund with portfolio companies LearnIn and TransfrVR)

- Jomayra Herrera, principal, Cowboy Ventures (a generalist fund with portfolio companies Hone and Guild Education)

- John Danner, managing partner, Dunce Capital (an edtech and future of work fund with portfolio companies Lambda School and Outschool)

- Mercedes Bent and Bradley Twohig, partners, Lightspeed Venture Partners (a multistage generalist fund with investments including Forage, Clever and Outschool)

- Ian Chiu, managing director, Owl Ventures (a large edtech-focused fund backing highly valued companies including Byju’s, Newsela and Masterclass)

- Jan Lynn-Matern, founder and partner, Emerge Education (a leading edtech seed fund in Europe with portfolio companies like Aula, Unibuddy and BibliU)

- Benoit Wirz, partner, Brighteye Ventures (an active edtech-focused venture capital fund in Europe that backs YouSchool, Lightneer and Aula)

- Charles Birnbaum, partner, Bessemer Venture Partners (a generalist fund with portfolio companies including Guild Education and Brightwheel)

- Daniel Pianko, co-founder and managing director, University Ventures (a higher ed and future of work fund that is backing Imbellus and Admithub)

- Rebecca Kaden, managing partner, Union Square Ventures (a generalist fund with portfolio companies including TopHat, Quizlet, Duolingo)

- Andreata Muforo, partner, TLCom Capital (a generalist fund backing uLesson)

Full Extra Crunch articles are only available to members

Use discount code ECFriday to save 20% off a one- or two-year subscription

In other news: Extra Crunch Live, a series of interviews with leading investors and entrepreneurs, returns next month with a full slate of guests. This year, we’re adding a new feature: Our guests will analyze pitch decks submitted by members of the audience to identify their strengths and weaknesses.

If you’d like an expert eye on your deck, please sign up for Extra Crunch and join the conversation.

Thanks very much for reading! I hope you have a fantastic weekend — we’ve all earned it.

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

13 investors say lifelong learning is taking edtech mainstream

Image Credits: Bryce Durbin

Rising African venture investment powers fintech, clean tech bets in 2020

Image Credits: Nigel Sussman (opens in a new window)

After falling into yesterday’s wild news cycle, Alex Wilhelm returned to The Exchange this morning with a close look at venture capital activity across Africa in 2020.

“Comparing aggregate 2020 figures to 2019 results, it appears that last year was a somewhat robust year for African startups, albeit one with fewer large rounds,” he found.

For more context, he interviewed Dario Giuliani, the director of research firm Briter Bridges, which focuses on emerging markets in Africa, Asia and Latin America.

Talent and capital are shifting cybersecurity investors’ focus away from Silicon Valley

Image Credits: MCCAIG (opens in a new window) / Getty Images

New cybersecurity ecosystems are popping up in different parts of the world.

Some of of that growth has been fueled by an exodus from the Bay Area, but many early-stage security startups already have deep roots in East Coast cities like Boston and New York.

In the United Kingdom and Europe, government innovation programs have helped entrepreneurs close higher numbers of Series A and B rounds.

Investor interest and expertise is migrating out of Silicon Valley: This post will help you understand where it’s going.

Will Apple’s spectacular iPhone 12 sales figures boost the smartphone industry in 2021?

Image Credits: NurPhoto (opens in a new window) / Getty Images

Today’s smartphones are unfathomably feature-rich and durable, so it’s logical that sales have slowed.

A phone purchased 18 months ago is probably “good enough” for many consumers, especially in times of economic uncertainty.

Then again, of the record $111.4 billion in revenue Apple earned last quarter, $65.68 billion came from phone sales, largely driven by the release of the iPhone 12.

Even though “Apple’s success this quarter was kind of a perfect storm,” writes Hardware Editor Brian Heater, “it’s safe to project a rebound for the industry at large in 2021.”

The 5 biggest mistakes I made as a first-time startup founder

Image Credits: Randy Faris (opens in a new window) / Getty Images

Finmark co-founder and CEO Rami Essaid wrote a post for Extra Crunch that candidly describes the traps he laid for himself that made him a less-effective entrepreneur.

As someone who’s worked closely with founders at several startups, each of the points he raised resonated deeply with me.

In my experience, many founders have a hard time delegating, which can quickly create cultural and operational problems. Rami’s experience bears this out:

“I became a human GPS: People could follow my directions, but they struggled to find the way themselves. Independent thinking suffered.”

Dear Sophie: How can I sponsor my mom and stepdad for green cards?

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie:

I just got my U.S. citizenship! My husband and I want to bring my mom and her husband to the U.S. to help us take care of our preschooler and toddler.

My biological dad passed away several years ago when I was an adult and my mom has since remarried.

— Appreciative in Aptos

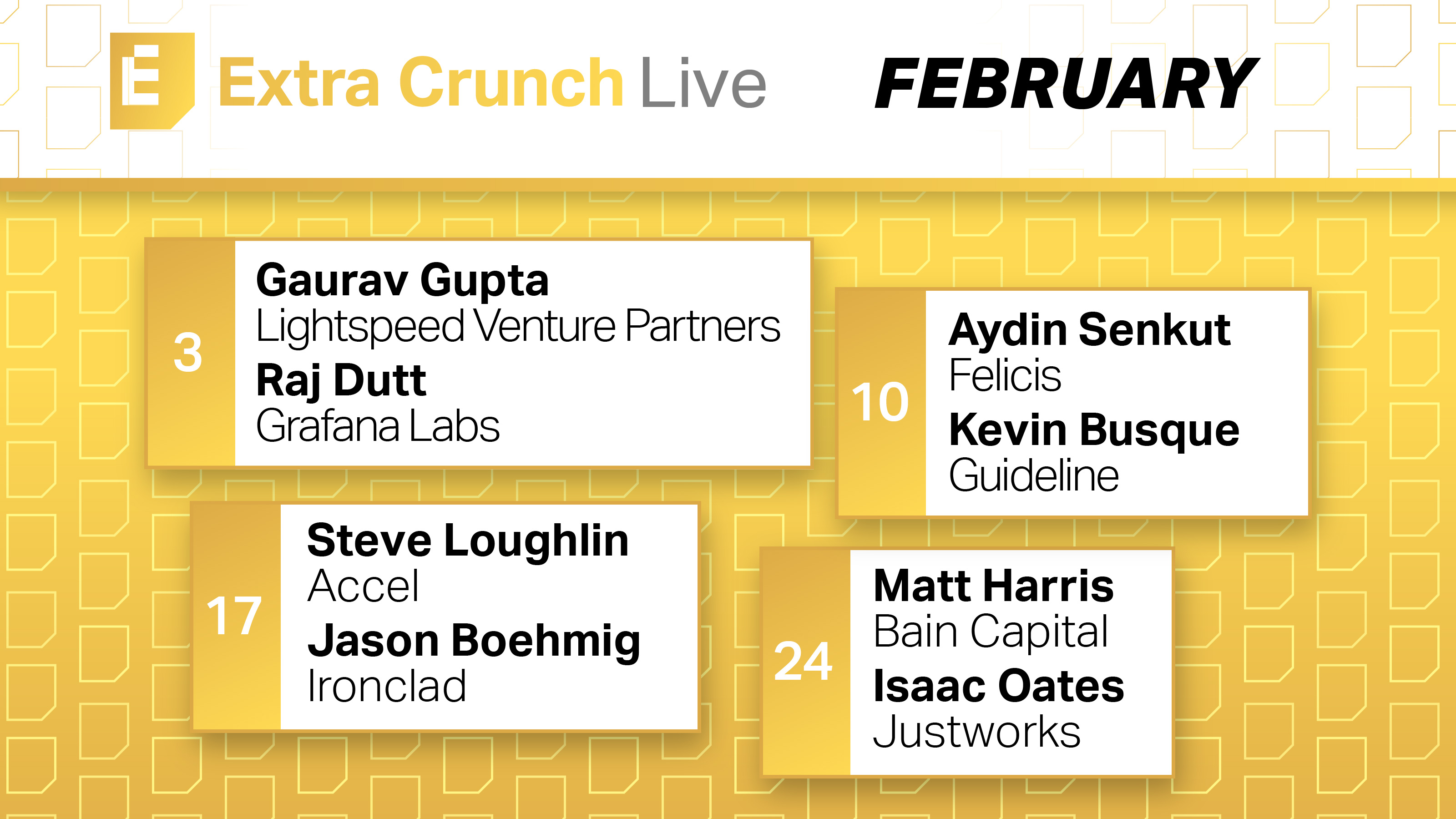

Check out the amazing speakers joining us on Extra Crunch Live in February

Next month, Extra Crunch Live returns with a lineup of guests who are extremely well-qualified to discuss early-stage startups.

Each Wednesday at noon PPST/3 p.m. EST, join a conversation with founders and the investors who backed their companies:

February 3:

Gaurav Gupta (Lightspeed Venture Partners) + Raj Dutt (Grafana Labs)

February 10:

Aydin Senkut (Felicis Ventures) + Kevin Busque (Guideline)

February 17:

Steve Loughlin (Accel) + Jason Boehmig (Ironclad)

February 24:

Matt Harris (Bain Capital) + Isaac Oates (Justworks)

Also, we’re adding a new feature to Extra Crunch Live — our guests will offer advice and feedback on pitch decks submitted by Extra Crunch members in the audience!

10 VCs say interactivity, regulation and independent creators will reshape digital media in 2021

Image Credits: Aleksandar Nakic (opens in a new window) / Getty Images

Since the pandemic disrupted the social rhythms of work and school, many of us have compensated by changing our relationship to digital media.

For instance, I purchased a new sofa and thicker living room curtains several months ago when I realized we have no idea when movie theaters will reopen.

Last year, podcast sponsors spent almost $800 million to reach listeners, but ad revenue is estimated to surpass $1 billion this year. Clearly, I’m not the only person who used a discount code to buy a new product in 2020.

At this point, I can scarcely keep track of the multiple streaming platforms I’m subscribed to, but a new voice-activated remote control that comes with my basic cable plan makes it easier to browse my options.

Media reporter Anthony Ha spoke to10 VCs who invest in media startups to learn more about where they see digital media heading in the months ahead. For starters, how much longer can we expect traditional advertising models to persist?

And in a world with hundreds of channels, how are creators supposed to compete for our attention? What sort of discovery tools can we expect to help us navigate between a police procedural set in a Scandinavian village and a 90s sitcom reboot?

Here’s who Anthony interviewed:

- Daniel Gulati, founding partner, Forecast Fund

- Alex Gurevich, managing director, Javelin Venture Partners

- Matthew Hartman, partner, Betaworks Ventures

- Jerry Lu, senior associate, Maveron

- Jana Messerschmidt, partner, Lightspeed Venture Partners

- Michael Palank, general partner, MaC Venture Capital (with additional commentary from MaC’s Marlon Nichols)

- Pär-Jörgen Pärson, general partner, Northzone

- M.G. Siegler, general partner, GV

- Laurel Touby, managing director, Supernode Ventures

- Hans Tung, managing partner, GGV Capital

Normally, we list each investor’s responses separately, but for this survey, we grouped their responses by question. Some readers say they use our surveys to study up on an individual VC before pitching them, so let us know which format you prefer.

Does a $27 billion or $29 billion valuation make sense for Databricks?

Image Credits: Nigel Sussman (opens in a new window)

Data analytics platform Databricks is reportedly raising new capital that could value the company between $27 billion and $29 billion.

By the end of Q3 2020, Databricks had surpassed a $350 million run rate — a $150 million YoY increase, reports Alex Wilhelm.

At the time, he described the company as “an obvious IPO candidate” with “broad private-market options.”

Which begs the question: “Can we come up with a set of numbers that help make sense of Databricks at $27 billion?”

End-to-end operators are the next generation of consumer business

Image Credits: Natalia Timchenko (opens in a new window) / Getty Images

Rapid shifts in the way we buy goods and services disrupted old-school marketplaces like local newspapers and the Yellow Pages.

Today, I can use my phone to summon a plumber, a week’s worth of groceries or a ride to a doctor’s office.

End-to-end operators like Netflix, Peloton and Lemonade take a lot of time and energy to reach scale, but “the additional capital required is often outweighed by the value captured from owning the entire experience.”

Unpacking Chamath Palihapitiya’s SPAC deals for Latch and Sunlight Financial

Image Credits: Nigel Sussman (opens in a new window)

On January 25, Social Capital CEO Chamath Palihapitiya tweeted that he was making two blank-check deals.

Enterprise SaaS company Latch makes keyless entry systems; Sunlight Financial helps consumers finance residential solar power installations.

“There are nearly 300 SPACs in the market today looking for deals,” noted Alex Wilhelm, who unpacked both transactions.

“There’s no escaping SPACs for a bit, so if you are tired of watching blind pools rip private companies into the public markets, you are not going to have a very good next few months.”

Fintechs could see $100 billion of liquidity in 2021

Image Credits: dan tarradellas (opens in a new window) / Getty Images

On Monday, we published the Matrix Fintech Index, a three-part study that weighs liquidity, public markets and e-commerce trends to create a snapshot of an industry in perpetual flux.

For four years running, the S&P 500 and incumbent financial services companies have been outperformed by companies like Afterpay, Square and Bill.com.

In light of steady VC investment, increasing consumer adoption and a crowded IPO pipeline, “fintech represents one of the most exciting major innovation cycles of this decade.”

Drupal’s journey from dorm-room project to billion-dollar exit

Image Credits: Acquia

On January 15, 2001, then-college student Dries Buytaert released Drupal 1.0.0, an open-source content-management platform. At the time, about 7% of the world’s population was online.

After raising more than $180 million, Buytaert exited to Vista Equity Partners for $1 billion in 2019.

Enterprise reporter Ron Miller interviewed Buytaert to learn more about his 18-year journey.

“His story is compelling, but it also offers lessons for startup founders who also want to build something big,” says Ron.