& meet dozens of singles today!

User blogs

French startup Seyna is getting a new CEO. Stephen Leguillon is joining the company as chief executive while Philippe Mangematin is stepping back from day-to-day activities for personal reasons — he’ll become honorary chairman.

If you’re not familiar with the company, Seyna is an insurtech startup that has obtained an insurance license focused on property and casualty. This is a significant move as the French regulator (ACPR) hasn’t handed out a new license in this category since 1983.

The company’s go-to-market strategy is also interesting as it doesn’t sell insurance products to consumers directly. Instead, the company is building out insurance-as-a-service products. It partners with other companies that offer Seyna’s insurance products under their own brands.

Behind the scenes, Seyna offers an API to generate insurance contracts on demand — an API is a programming interface that lets two services interact with each other. You can also connect directly to Seyna’s interface to manage contracts.

Seyna has created its own core insurance system, which is an important differentiating factor compared to legacy players. The startup can generate many different variants that cover around 20 different insurance products — pet insurance, ticket cancelation, rent guarantee, etc. Clients include Garantme and Decathlon.

The company’s new CEO Stephen Leguillon previous co-founded La Belle Assiette, a company that lets you hire a chef for a dinner at home and that I covered on TechCrunch. He added a second product called GoCater, a corporate catering service — GoCater was letter spun out from La Belle Assiette and acquired by ezCater.

Seyna has raised a €14 million seed round ($17 million at today’s rate) from Global Founders Capital, Allianz France, Financière Saint James and several business angels. Insurance companies require a ton of capital to operate, that’s why the seed round seems quite big for the French market.

Prakhar Singh and ex-Paystack employee Abdul Hassan have known each other for seven years, building different tech products individually and collectively along the way.

Before joining Paystack in 2018, Hassan co-founded OyaPay, a payments startup the year before. After leaving the Stripe-owned company in 2019, he launched a data startup called Voyance where Singh, who had already exited one of his products — Transferpay.ng, an offline payments startup — was a software engineer.

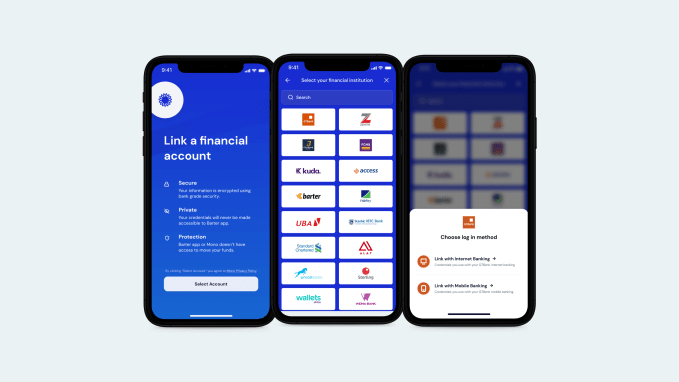

Last June, the duo started working on Mono, a project that would allow companies to access their customers’ financial accounts in Nigeria.

By streamlining various data in a single API, companies and third-party developers can retrieve vital information like account statements, real-time balance, historical transactions, income, expense and account owner identification. Of course, this isn’t without users’ consent as they are required to login with their internet or mobile login credentials before any transaction takes place.

Following a series of tests and iterations, Mono launched its beta version in August, with Hassan as CEO and Singh as CTO. A month later, the startup closed a $500,000 pre-seed investment from early-stage investors like Lateral Capital, Ventures Platform, Golden Palm Investments and Rally Cap. It was one of the notable pre-seed rounds on the continent because of the length of time it took from launch to funding, a trait other API fintech startups in the region share, albeit with significantly longer timelines.

In a region where more than half of the population is either unbanked or underbanked, these open finance players are trying to improve financial inclusion on the continent. Open finance thrives on the notion that with access to a financial ecosystem via open APIs and new routes to move money, access financial information and make borrowing decisions, the barriers and costs of entry for the unbanked and underbanked might come down.

However, for Hassan, Mono’s play overlaps open finance and open banking. Although the two terminologies portray what these African startups want to accomplish, the CEO believes that they are subject to regulation from the government and apex financial institutions. Mono is a data company playing in the fintech space, he says.

Prakhar Singh (CTO) and Abdul Hassan (CEO)

He likened Mono to how Google was in its early days when it started with a simple mission to organize the world’s information and make it accessible. Decades later, Google has metamorphosed into an internet giant playing in a plethora of sectors.

“If you ask me, I’ll say we don’t see ourselves entirely in open banking or finance,” he told TechCrunch. “Today, we’re concerned about how we can get data from different sources and aggregate into a database where businesses can get access to them with our users’ consent. Down the line, we can use this data for different use cases and solve various problems.”

Mono has already secured partnerships with more than 16 financial institutions in Nigeria and has a little over a hundred businesses like Carbon, Renmoney, Flutterwave and Indicina using its platform. They process about 5 million datasets per hour, the CEO claims.

These clients are mainly lending companies with a few others in proptech and health tech, which allow users to pay for their services in installments. But there are plans to diversify this clientele. One such way will be to improve onboarding processes on applications through its one-click signup feature.

From a user’s perspective, here’s how it works when considering two savings applications: Users submit their KYC to the first savings app. But for one reason or the other, maybe due to a better interest rate, some users switch to a second savings app.

However, there’s a little hassle in that a second KYC is needed for this process. What Mono has done with the one-click signup feature is to let users transfer their data from the first app to the second without repeating the process. And to that end, Mono has partnered with two of Nigeria’s leading savings and investment platforms to roll out the service.

“First, we’ve enabled companies with a new infrastructure that allows them to get access to customers’ financial accounts and understand their history before giving them loans or any financial service. Now, we think with the new generation of companies coming up in Africa, Mono will be the one to power their onboarding processes,” Hassan remarks on the platform’s offerings.

Image Credits: Mono

For any investor, Mono’s sticky features, coupled with explosive growth, looks too good of an opportunity to pass on. Today, the six-month-old startup announced that it has been accepted into Y Combinator’s Winter 2021 batch. It will receive $125,000 in seed funding with an opportunity to receive follow-up investment after graduating in March. The startup also joins 39 other African startups per YC data which have passed through the accelerator since 2009.

Getting into the accelerator helps Mono with one of its biggest challenges. According to Hassan, Mono has come across users who are still skeptical to input their internet banking details on the platform due to personal experiences with online fraud in the country.

“To date, we’ve been focusing on building, and I think we’ve gotten to a stage where we’re seeing some people not wanting to use their internet banking on Mono.” But with YC’s backing and a conscious offline marketing plan afterwards, the founder thinks Mono’s credibility can get a lift.

At Paystack, where Hassan was a product manager, he was privileged to experience firsthand the company’s innovation and growth before it was acquired by Stripe last year. He says he learned the ropes of product development and management, and hiring — lessons that have stuck with him to Mono, a company now with 13 staff across Nigeria and India.

The plan for Mono is to be a global company and getting into YC provides the perfect opportunity to do so. The company is also planning an imminent pan-African expansion to Ghana and Kenya, and from all indication, Mono might execute one if not the two before the end of Q1. Setting the company up for expansion and the hiring spree that comes with it will require capital, so a seed round is in the works to facilitate the whole process.

Digital ordering and paying at restaurants was already gaining much ground in China before the COVID-19 pandemic hit. The tap-to-order method on a smartphone is part of the greater development in China where cash and physical documentation is increasingly being phased out. Many restaurants across large cities go as far as making digital menus mandatory, cutting staff costs.

Meanwhile, there has been pushback from the public and the authorities over aggressive digitization. An article published this week by People’s Daily, an official paper of the Chinese Communist Party, was titled: “Scan-to-order shouldn’t be the only option.”

Aside from harming consumers’ freedom of choice and removing the human interaction that diners might appreciate, mandatory smartphone use also raises concerns over data privacy. Ordering on a phone often requires access to a person’s profile on WeChat, Alipay, Meituan or other internet platforms enabling restaurants’ digital services. With that trove of data, businesses will go on to span users with ads.

“These approaches harm consumers’ data protection rights,” the People’s Daily quotes a senior personnel at the consumer rights unit of China Law Society, China’s official organization of legal academic professionals, as saying.

China has similarly targeted the ubiquity of cashless payments. In 2018, China’s central bank called rejecting cash as a form of payment “illegal” and “unfair” to those not accustomed to electronic payments, such as senior citizens.

The elderly also face a dilemma as digital health codes, which are normally generated by tracking people’s movement history using location data from SIM cards, becomes a norm amid the pandemic. Without a smartphone-enabled health pass, senior citizens could be turned away by bus drivers, subway station guards, restaurant staff and gatekeepers at other public venues.

To bridge the digital divide, the southern province of Guangdong recently began allowing citizens to check their health status by tapping their physical ID cards on designated scanners.

Cashless payment is an irreversible trend though. Between 2015 and 2020, the digital payments penetration rate amongst China’s mobile internet users went from less than 60% to over 85%, according to official data. Moreover, the government is hastening the pace to roll out digital yuan, which, unlike third-party payments methods, is issued and managed by the central bank and serves as the statutory, digital version of China’s physical currency.

Source: https://techcrunch.com/2021/02/01/china-criticize-contactless-payments/

Two years after launching its $56 million debut fund, Kindred Ventures, a San Francisco-based pre-seed and seed-stage venture fund founded by Steve Jang and Kanyi Maqubela, has closed its second fund with $100 million in capital commitments.

Jang is himself a founder who later jumped into investing. In more recent years, he cofounded Bitski, a crypto-asset wallet startup, and previously founded Schematic Labs, an early social music app that was brought into Rhapsody in 2014, and co-created the music streaming service imeem, whose assets were later acquired by MySpace.

Jang was also an early advisor to Uber, and individually invested in a number of breakout companies, including the delivery company Postmates, the synthetic biology company Zymergen, the fitness company Tonal, and the crypto exchange Coinbase.

Maqubela has similarly worn the hats of both founder and investor, spending six years as an investor with the seed- and early-stage firm Collaborative Fund before joining forces with Jang, as well as cofounding Heartbeat Health — a platform that invites patients who are at risk of heart disease and other chronic ailments to talk remotely with experts for care management.

The fund is notable, including because it doesn’t zero in on one or two sectors of tech. Why is that interesting? Well, because the venture landscape is now so crowded that institutional investors typically prefer to see seed-stage funds with a specific sector focus or an angle of some sort. It’s a way for these limited partners to better diversify their own investments and keep from backing managers who are investing in the very same deals.

Indeed, that Jang and Maqubela secured commitments from a mix of major university endowments, foundations, fund-of-funds, and strategic investors despite being generalists is something a feat.

No doubt investor interest ties to some of their earlier investments, like Coinbase — bets that underscore they are in the right entrepreneurial circles. Yet they say that another aspect of their pitch also resonated with investors, which is their “high concentration, high conviction” approach. Part of their workflow, for example, involves creating a Signal group or Slack channel as soon as they invest in a team so there can be a constant back-and-forth and to bolster the sense that Jang and Maqubela are extensions of a founding team.

Kindred says it also schedules weekly one-on-one chats with the founders it funds until their startup has designated a product launch date, after which “we move into a less rigorous, less frequent meetings,” says Jang, describing the firm’s approach very “programmatic and designed.”

But another way Kindred tries to gain an edge over competitors is by moving as close to the concept stage as possible — even helping to form startups. Jang and Maqubela point back to Heartbeat Health and Bitski, which they helped incubate and spin out. Another startup born of their “formation investing” approach is a payments company called Otto, and they say to expect more to come.

In some cases, they start the company and assemble the founding team. In other cases, they help a new founder evolve from concept to prototype to landing the right cofounder. What it asks for in exchange is an ownership stake that ranges from between 5% of a company to 20% percent, with an average ownership position of 11%, they say, and ticking upward as the firm matures.

As for deal flow, they say they source their deals through introductions from the founders in their portfolio, through their own outreach based on ideas that excite them, and from employees of past portfolio companies.

Interestingly, though the bets they make range widely in focus, different themes do emerge, including around digital health, where in addition to Heartbeat Health and Tonal they backed Color, whose at-home tests can help people understand if they are at risk of hereditary cancer, as well as whether they have been exposed to COVID-19. (It closed its newest round at a $1.5 billion valuation earlier this month.)

Kindred is focused on community, too, with bets that include the audio social network Clubhouse. And Kindred is writing checks to the occasional security company, including Anjuna Security, which aims to protects applications and data from insiders by seamlessly encrypting everything end to end.

Not last, finance is plainly an area of interest. In addition to Coinbase, for example, Kindred more recently invested in dYdX, an open trading platform for crypto assets that just last announced it had raised $10 million in Series B funding.

As for how the two — who wound up funding 25 companies altogether in their first fund — can continue to cover so much ground as they set out to invest this new, bigger vehicle, Maqubela says the question came up “more than half the time” in conversations about this next fund with its investors. But their secret sauce is no great mystery, they insist. They say they just happen to be incredibly curious people who are willing to get up to speed however possible when they meet a founder with whom they want to partner.

“It ultimately comes down to who Kanyi is and who I am,” says Jang, “and we’re both voracious about learning, it’s what drives us.”

Though both have experience and know-how about a wide number of verticals at this point, they’re “absolutely novices” at times, and they don’t let that stop them, both say.

“If we’re inspired by the founder, their intellect, their dedication to a problem, and why they’re doing what they’re doing, we’re happy to go learn as quickly as possible,” offers Jang. “We’re very dutiful students.”

Google has agreed to pay $2.59 million to more than 5,500 current employees and former job applicants as part of a settlement with the U.S. Department of Labor over allegations of systemic discrimination as it relates to compensation and hiring. Google has also agreed to reserve $250,000 a year for the next five years to address any potential pay equity adjustments that may come up. That brings Google’s total financial commitment to $3.8 million — a drop in the bucket for the company, whose parent company Alphabet has a market cap of $1.28 trillion.

The settlement comes after the DOL’s Office of Federal Contract Compliance Programs found pay disparities affecting female software engineers at Google’s offices in Mountain View, as well as in offices in Seattle and Kirkland, Washington. The OFCCP also found differences in hiring rates that “disadvantaged female and Asian applicants” for engineers roles at Google’s locations in San Francisco, Sunnyvale and Kirkland. The OFCCP’s evaluation covered Sept. 1, 2014 through Aug. 31, 2017.

As part of the settlement, Google has agreed to pay $1.35 million in back pay and interest to 2,565 female software engineers at the company ($527.50 per employee), and $1.25 million in back pay and interest to 1,757 women and 1,219 Asian applicants for software engineering roles they were not hired for ($414 per person).

Lastly, Google will reserve $1.25 million of the money to go toward pay-equity adjustments for the next five years for U.S. engineers at Google’s Mountain View, Kirkland, Seattle and New York offices.

“We believe everyone should be paid based upon the work they do, not who they are, and invest heavily to make our hiring and compensation processes fair and unbiased,” a Google spokesperson said in a statement to TechCrunch. “For the past eight years, we have run annual internal pay equity analysis to identify and address any discrepancies. We’re pleased to have resolved this matter related to allegations from the 2014-2017 audits and remain committed to diversity and equity and to supporting our people in a way that allows them to do their best work.”

“The U.S. Department of Labor acknowledges Google’s willingness to engage in settlement discussions and reach an early resolution,” Office of Federal Contract Compliance Programs Regional Director Jane Suhr said in a press release. “The technology industry continues to be one of the region’s largest and fastest growing employers. Regardless of how complex or the size of the workforce, we remain committed to enforcing equal opportunity laws to ensure non-discrimination and equity in the workforce.”

Source: https://techcrunch.com/2021/02/01/google-dol-discrimination-settlement/