& meet dozens of singles today!

User blogs

Djamo, a financial super app for consumers in Francophone Africa, is the first startup from Ivory Coast to get backing from Y Combinator.

While there has been a huge profusion of financial services that have emerged in recent years in Africa, Djamo’s mission is to try to plug one specific and a very underserved gap in Francophone Africa.

In the region, less than 25% of adults have bank accounts as the focus for banks remains the top 10-20% wealthiest customers. The rest, which is a huge segment of the market of about 120 million people, is not perceived as profitable. But as banks slacked, mobile money from the region’s telcos filled in the gap. In the last 10 years, their wallets have reached more than 60% of the population — proof of how many millions of French-speaking natives were hungry for financial services. Today, this mobile money infrastructure and reach allows startups to build upon their existing payment infrastructure to democratize access through different applications.

Djamo is one of such companies taking advantage of this opportunity to bring affordable and seamless banking to the region.

In 2019, Hassan Bourgi, a second-time founder, returned to Ivory Coast after exiting his Latin American-based startup, Busportal, to Naspers-company redBus. There he met Régis Bamba who was still working at MTN, one of Africa’s largest telcos, leading several mobile money projects.

Frustrated by the unpleasant banking experiences they and many millennials faced in the country, Bourgi and Bamba launched Djamo last year to challenge the banking industry status quo.

“Banking services are really difficult to access here, and we saw that as a huge opportunity,” Djamo CEO Bourgi said to TechCrunch. “Since day one, we wanted to design a mobile-first platform that could break into the masses and our combined experience building mass-market consumer products was very critical to launching Djamo.”

According to Bourgi, the country’s millennials are trying to create relations with technology companies and be served differently from the norm. So, Djamo is providing this audience with a better front end experience and faster customer service.

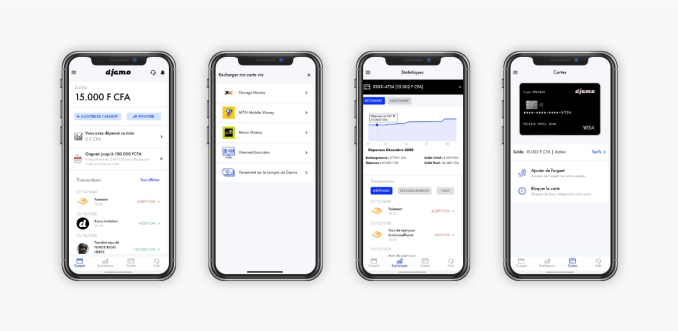

Image Credits: Djamo

Rather than offering a one-size-fits-all approach, they focused on accommodating multiple layers tailored to different user needs. Whether it’s affording Ivorians the luxury to pay for online services like Amazon, Alibaba, or Netflix, or providing VISA debit cards in a timely fashion, these tailored approaches have made Djamo grow organically via word of mouth.

And why not? Before Djamo came along, the CEO says people would need to go to their bank branches and stay in long queues to get their cards or even load them with credit. Djamo relieves that stress and even allows customers to use their cards with zero fees in a wide range of services.

“For us, it was important to offer a zero-fee card with no recurring fee to a certain limit. After that, you pay as you go in transaction fees. There is a premium plan around $4 a month where users can transact to higher limits,” said Bourgi.

Today, Djamo claims to have around 90,000 registered users and processes over 50,000 transactions monthly. However, to get to this point, the company has ridden on sheer resourcefulness around its operations.

Unlike Nigeria, where there are established payment infrastructure players like Flutterwave and Paystack, Ivory Coast doesn’t have such household names.

“We have a couple of providers, but most are unreliable. But this doesn’t matter to the end-user, you have to make it work somehow,” said Bambi, the company’s CPO and CTO.

Lacking better options, Djamo switches from one provider to another to keep operations running. The year-old startup has also faced scepticism issues, common with most African fintech startups when they first launch. In Djamo’s case though, the founders had to go at lengths to prove to banks and customers that the platform was safe to use for onboarding, KYC and transactions.

Hassan Bourgi (CEO) and Régis Bamba (CTO & CPO)

Onboarding customers also came with its own set of problems: the delivery of Djamo VISA cards. Bourgi says unlike more developed countries on the continent, it is a Herculean task to access efficient delivery and logistics services in Ivory Coast. So, the startup built a delivery app with in-house delivery agents for this particular purpose. “The objective for our customers is that after registering with us, they get their cards the next day in a timely fashion,” Bourgi added.

But even before pushing out its MVP, Djamo had already received monetary validation for its product. In June 2019, it raised a pre-seed investment of $350,000 from private investors — arguably the largest round at this stage in the Francophone region. The ingenuity of the solution, at least to French-speaking Africa, and the founders’ track record was crucial to Djamo closing the round, Hassan explained.

For a long time, Francophone Africa has been underrated by international investors despite signs pointing to the emergence of a budding startup scene. Part of this has to do with language barriers and the region’s GDP and income per capita where English-speaking countries, excluding South Africa, contribute to 47% of sub-Saharan Africa’s average GDP, while French-speaking countries boast of only 19%.

However, with the World Bank stating that the region will have 62.5% of Africa’s fastest-growing economies by 2021, there’s bullishness around its growth in the coming years.

With so many untapped opportunities, underrepresented regions like Francophone Africa are ripe for disruption. Investors know this and though their checks are still skewed towards Anglophone Africa, million-dollar raises from Senegalese energy startup, Oolu and Cameroonian healthtech startup, Healthlane in 2020 show their keenness on the market.

Like Djamo, both startups are YC-backed and are the other Francophone startups to have made it into the accelerator. But with this Winter 2021 batch, Djamo becomes the first fintech startup from the region. Following Healthlane’s acceptance in 2020, it is also the first time French-speaking Africa has had representatives for consecutive years.

To the founders, YC’s backing validates Djamo’s premise that financial service distribution across the Francophone Africa region is fundamentally changing towards applications.

“In Ivory Coast, people always say that the banking industry is too complex and we can’t do anything about it. But we saw it as a huge opportunity and a great industry to take on. Everywhere you see frustration, customers in pain, there is an opportunity for a business to come and do it better,” said Régis.

After participating in the three-month-long program which culminates in a Demo Day on March 23rd, Djamo will also take part in Visa’s Fintech Fast Track Program, an avenue for the company to leverage the fintech giant’s network to introduce new payment experiences.

Twinco Capital, a Madrid and Amsterdam-based startup making it easier to access supply chain finance, has raised €3 million in funding.

Leading the round is Spanish VC fund Mundi Ventures, with participation from previous backer Finch Capital and several unnamed angels. Twinco Capital also has a debt facility with the Spanish investment bank EBN Banco de Negocios, which is common for any type of lending company.

Founded in 2016 by Sandra Nolasco and Carmen Marin Romano, Twinco Capital offers a supply chain finance solution that includes purchase order funding. To do this, it integrates with large corporates on the purchase side and then funds suppliers by paying up to 60% of the purchase order value upfront and the remainder immediately upon delivery.

The entire process is digital, promising a quick decision and fast deployment of funds, and is powered by Twinco’s supply chain analytics and the data it is able to access by partnering with both sides of the supply chain.

“The financing of global supply chains is expensive and inefficient, the burden of the cost is mostly borne by the suppliers and in particular by those that are SMEs in emerging markets,” explains Twinco Capital co-founder and CEO Sandra Nolasco.

“Take any global supply chain, such as apparel, automotive, electronics etc. Exporters in countries like Bangladesh, China or Vietnam that have been supplying European companies for years, with stable commercial relationships. However, their creditworthiness is still measured only on the basis of annual financials, making access to competitive liquidity a major obstacle for growth”.

By having visibility on both sides, including upcoming orders, Twinco provides liquidity to the suppliers “from purchase order to final invoice payment”.

“We do that by analyzing supply chain data – the performance of the suppliers, the network effects between common suppliers and buyers (and many more data points I am not allowed to mention!),” says the Twinco CEO. “In short, using advanced data analytics we can better assess, price and significantly mitigate risk. The good news is that the more transactions we fund, the more suppliers and buyers we add, the more robust is our risk assessment. We believe there is a strong network effect”.

To that end, Twinco makes money by charging a “discount fee” for each purchase order it funds. “Since default rates are a fraction of that fee, we can unlock significant value,” says Nolasco.

Meanwhile, the fintech is also unlocking an asset class for investors and competes with local banks that are much more manual and don’t benefit from increased visibility via network effects. Nolasco says that to ensure interests are aligned, the company uses a portion of equity to also invest in the purchase orders it funds.

PayPal is shutting down its domestic business in India, less than four years after the American giant kickstarted local operations in the world’s second largest internet market.

“From 1 April 2021, we will focus all our attention on enabling more international sales for Indian businesses, and shift focus away from our domestic products in India. This means we will no longer offer domestic payment services within India from 1 April,” said a company spokesperson.

In a long statement, PayPal did not say why it was winding down its India business, but a report recently said the company, which has amassed over 360,000 merchants in the country, had failed to make inroads in India. .

Indian news outlet The Morning Context reported in December that PayPal was abandoning its local payments business in India, a claim the company had refuted at the time.

Nonetheless, the move comes as a surprise. The company said last year that it was building a payments service powered by India’s UPI railroad, suggesting the level of investments it was making in the country.

PayPal had also partnered with a range of popular Indian businesses such as ticketing services BookMyShow and MakeMyTrip and food delivery platform Swiggy to offer a faster check out experience. At the time of writing, PayPal website in India appears to have removed all such references.

India has emerged as one of the world’s largest battlegrounds for mobile payments firms in recent years. Scores of heavily-backed firms including Paytm, PhonePe, Google, Amazon, and Facebook are competing among one another to increase their share in India, where the market is estimated to be worth $1 trillion by 2023. Several of these firms also offer a range of payments services for merchants.

The company, which says it processed $1.4 billion worth of international sales for merchants in India last year, added that it will continue to invest in “product development that enables Indian businesses to reach nearly 350 million PayPal consumers worldwide, increase their sales internationally, and help the Indian economy return to growth.”

Source: https://techcrunch.com/2021/02/04/paypal-is-shutting-down-domestic-payments-business-in-india/

Kuaishou, a Chinese video app that’s largely underappreciated outside China, has just completed a massive initial public offering in Hong Kong. The app is by far the biggest rival for Douyin, TikTok’s Chinese version, and unlike many Western video platforms that make money from ads and subscriptions, Kuaishou’s cash cow is its tipping business.

Kuaishou’s shares opened in Hong Kong on Friday at HK$338 ($43.6) apiece, a 194% jump from its IPO price of HK$115 ($14.8). That catapults its market cap to nearly HK$1.4 trillion ($180 billion). The company pocketed approximately $5.4 billion from the listing with a total of 365,218,600 shares, excluding the overallotment option.

Kuaishou, which is backed by Tencent, now has a replenished coffer to invest in growth and hopefully work towards profitability. In the first nine months of 2020, the app posted an adjusted net loss of 7.2 billion yuan ($1.1 billion), compared to an adjusted profit of 1.8 billion yuan in the same period a year earlier.

Kuaishou’s stock is a huge hit with both institutional financiers and retail investors from China, many of whom are familiar with the app that boasted 481 million monthly users in the 11 months ended November. The app set a record as the most oversubscribed deal in Hong Kong, attracting retail investor demand totaling $164.8 billion, the South China Morning Post reported. Its share reached HK$322.8 on the gray market platform operated by Phillip Securities Group and HK$421 on online broker Futu Securities.

Like Douyin, Kuaishou began as a platform for people to create and share 15-second short videos (following a brief period as a GIF app) and later expanded into live streaming. The transition is natural, as creators who have built a name may seek further interaction with followers, and followers may want to express their loyalty and affection to creators. Live streaming and virtual gifting fill that need.

Kuaishou has three main monetization methods, with live streaming making up the majority of its revenue. Fifty-eight million users on Kuaishou spent on live videos monthly in the 11 months ended November, and on average every paying user brought 47.6 yuan ($7.36) in revenue.

The app also sells ads, with each user driving 71.4 yuan ($11) in marketing revenue for the period. Lastly, Kuaishou allows creators to hawk products. The gross merchandise value — an industry metric used loosely to measure e-commerce transactions — generated directly on Kuaishou reached 332.7 billion yuan ($51.4 billion) in the period.

For comparison, the live streaming feature on Alibaba’s Taobao bazaar generated over 400 billion yuan in GMV for the twelve months ended December.

While Kuaishou enjoys growing revenue from live streaming, regulatory risks loom in the background. The Chinese government has banned users under the age of 18 from purchasing virtual gifts. It has also urged platforms to put a cap on users’ monthly spending on virtual gifts, though regulators haven’t specified or suggested a limit.

Kuaishou is aware of the risk, noting in its prospectus that “any limits on user spending on virtual gifting ultimately imposed may negatively impact our revenues derived from virtual gifting and our results of operations.”

Until regulators take further action to rein in virtual gifting, Kuaishou will likely continue to thrive while it works on diversifying its business.

Democrats in the House voted to strip freshman Georgia Representative Marjorie Taylor Greene of some of her responsibilities Thursday, citing her penchant for violent, extreme and at times anti-Semitic conspiracy theories.

Greene has expressed support for a range of alarming conspiracies, including the belief that the 2018 Parkland school shooting that killed 17 people was a “false flag.” That belief prompted two teachers unions to call for her removal from the House Education Committee — one of her new committee assignments.

The vote on a resolution to remove Greene from her committee assignments broke along party lines, with nearly all Republicans opposing the resolution to remove Greene. Some of her colleagues even voted in Greene’s defense in spite of condemning her behavior in the past.

As the House moved to vote on the highly unusual resolution, the new Georgia lawmaker claimed that her embrace of QAnon was in the past.

“I never once said during my entire campaign “QAnon,'” Greene said Thursday. “I never once said any of the things that I am being accused of today during my campaign. I never said any of these things since I have been elected for Congress. These were words of the past.”

But as the Daily Beast’s Will Sommer reported, a deleted tweet from December shows Greene explicitly defending QAnon and directing blame toward the media and “big tech.”

Marjorie Taylor Greene claimed today that she hasn't promoted QAnon since being elected. But on Dec. 4, she praised an article promoting Q in a now-deleted tweet. The story Greene praised as "accurate" calls QAnon an "objective flow of information” that's "uniting Christians." pic.twitter.com/nN3bnTCyPa

— Will Sommer (@willsommer) February 4, 2021

In another recently-uncovered post from January 2019, Greene showed support for online comments calling for “a bullet to the head” for House Speaker Nancy Pelosi and executing FBI agents.

Greene has also shared openly racist, Islamophobic and anti-Semitic views in Facebook videos, a track record that prompted Republican House Minority Leader Kevin McCarthy to condemn her statements as “appalling” last June. More recently, McCarthy defended Greene against efforts to remove her from committees.

Greene was elected in November to represent a conservative district in northwest Georgia after her opponent Kevin Van Ausdal dropped out, citing personal reasons. Greene beat her opponent in the Republican primary in August, winning 57% of the vote.

QAnon, a dangerous once-fringe collection of conspiracy theories, was well-represented in January’s deadly Capitol riot and many photos from the day show the prevalence of QAnon symbols and sayings. In 2019, an FBI bulletin warned of QAnon’s connection to “conspiracy theory-driven domestic extremists.” A year later, at least one person who had espoused the same views would win a seat in Congress.

The overlap between Greene’s beliefs and those of the violent pro-Trump mob at the Capitol escalated tensions among lawmakers, many of whom feared for their lives as the assault unfolded.

A freshman representative with no apparent appetite for policy, Greene would wield little legislative power in the House. But as QAnon and related conspiracies move from the fringe to the mainstream and possibly back again — a trajectory largely dictated by the at times arbitrary decisions of social media companies — Greene’s treatment in Congress may signal what’s to come for a dangerous online movement that’s more than demonstrated its ability to spill over into real-world violence.

Source: https://techcrunch.com/2021/02/04/marjorie-taylor-greene-qanon-congress-committees/