& meet dozens of singles today!

User blogs

The Station is a weekly newsletter dedicated to all things transportation. Sign up here — just click The Station — to receive it every weekend in your inbox.

Hi friends and new readers, welcome back to The Station, a newsletter dedicated to all the present and future ways people and packages move from Point A to Point B.

Let’s dive in …

Email me at kirsten.korosec@techcrunch.com to share thoughts, criticisms, offer up opinions or tips. You can also send a direct message to me at Twitter — @kirstenkorosec.

Micromobbin’

Last week I highlighted how Lime was getting into the shared moped business. Now, shared moped startup Revel is getting into the EV charging game. I wonder if we are starting to witness the beginning of a business diversification trend in micromobility?

Revel said it is building a DC fast-charging station for electric vehicles in New York City, the first in a new business venture that will eventually spread to other cities. The company said this new “Superhub,” which is located at the former Pfizer building in Brooklyn, will contain 30 chargers and be open to the public 24 hours a day. This will be the first in a network of Superhubs opened by Revel across New York City, the company said.

Revel didn’t build the EV charging infrastructure in-house. Instead, it is using Tritium’s new RTM75 model for the first 10 chargers at its Brooklyn site, which will go live this spring. These chargers are designed to deliver 100 additional miles of charge to an electric vehicle in about 20 minutes, according to Revel.

Image Credits: Revel

Deal of the week

Uber announced plans to acquire alcohol delivery service Drizly in a stock-and-cash deal valued at $1.1 billion deal — cementing a strategy that started more than a year ago. The upshot: Uber is betting that its delivery and ride-hailing businesses will provide the fastest path to profitability.

Drizly’s marketplace will be eventually folded into the Uber Eats app. For now, Drizly will maintain the standalone app. The acquisition of Drizly is expected to close in the first half of the year.

For those who don’t follow Uber’s every move, here’s a quick recap. Since early 2020, Uber has offloaded most of its businesses, including shared scooter and bike unit Jump, self-driving subsidiary Uber Advanced Technologies Group and the air taxi moonshot Uber Elevate. It also sold a $500 million stake in its Uber Freight spinoff. Meanwhile, it acquired on-demand delivery app Postmates and now Drizly.

Rad Power Bikes is one other company that had a “deal of the week” worthy funding round. The Seattle-based electric bike seller raised $150 million from institutional investors, including Morgan Stanley’s Counterpoint Global Fund, Fidelity Management & Research Company, TPG’s global impact investing platform The Rise Fund and funds and accounts advised by T. Rowe Price Associates. Existing investors Durable Capital Partners LP and Vulcan Capital also participated in the round.

While $150 million is hardly the biggest raise in transportation, it’s one of the larger ones in the world of electric bikes. The size of round — and the institutions involved — suggests investors see room from growth in the ebike industry and believe in Rad Power’s business model and its ability to expand beyond the $100 million in sales it generated in 2019. Rad Power Bikes declined to disclose its 2020 sales numbers.

Rad Power is a direct-to-consumer electric bike seller known for creating robust products that combine features like fat tires, big batteries and motors with touchscreens, and even cargo carrying capacity — all at prices hundreds of dollars below its competitors.

The company’s founder and CEO Mike Radenbaugh told me that the funds will be used to double its 325-person workforce, increase the number of retail showrooms and service locations, continue to bring on more contract manufacturers to diversify its supply chain and add more accessories so consumers and customize their bikes.

Other deals that got my attention …

Bear Flag Robotics, the Silicon Valley-based startup that is developing autonomous technology for farm tractors, announced last month a $7.9 million seed extension funding round led by True Ventures. (I missed this one last week). The funding comes two years after it raised a $4.6 million seed round also led by True Ventures. Graphene Ventures, AgFunder, D20 and Green Cow VC also participated in the round.

DealerPolicy, an insurance marketplace for automotive retail, raised $30 million in Series B funding led by 3L Capital and Hudson Structured Capital Management Ltd.

Hip, the mobile app startup that connects riders to buses and shuttles, raised $12 million. The company was a consumer-facing business, but has changed its business model to focus on helping employers prepare for, and start to bring their workers back to the office or factory.

Otonomo, the cloud-based software startup that helps companies capture and monetize connected car data, agreed to merge with special purpose acquisition company Software Acquisition Group Inc. II with a valuation of $1.4 billion. The prospectus filed by the Otonomo shows it generated $400,000 in revenue in 2020 with a total operating expenditure of $10 million. Otonomo said it expects to have a negative gross profit through 2021. The company said it expects to be EBITDA positive by 2024.

REE Automotive has reached merger agreement with special purpose acquisition corporation 10X Capital Venture Acquisition Corp. The combined company, which will be listed on the NASDAQ under the new ticker symbol “REE,” will have an equity valuation of $3.6 billion. The startup has developed flat and modular EV platforms with fully autonomous-ready independent drive-by-wire, brake-by-wire and steer-by-wire technology for each wheel.

The company said it raised $300 million in private investment in public equity, or PIPE, from investors including Koch Strategic Platforms and Mahindra & Mahindra and Magna International.

The transaction is expected to provide more than $500 million of gross proceeds to the company.

Urban SDK, a connected mobility and safety analytics platform, raised $1.66 million in a funding round led by the Florida Opportunity Fund and matched by DeepWork Capital, a venture capital firm investing in early-stage companies in Florida.

Wheels Up, the private jet subscription service, announced plans to go public through a merger with special purpose acquisition company Aspirational Consumer Lifestyle Corp. The deal, which is expected to close in the second quarter, would give Wheels Up a valuation of more than $2 billion — more than twice its 2019 value.

Ford ramps up EV and AV spending

Ford said this week it will spend $22 billion on electrification — double its previous commitment — and invest $7 billion on autonomous vehicles through 2025. It should be noted that $2 billion of that AV budget has already been spent, leaving $5 billion left to invest over the next four years.

“We are accelerating all our plans — breaking constraints, increasing battery capacity, improving costs and getting more electric vehicles into our product cycle plan,” Ford CEO Jim Farley said. “People are responding to what Ford is doing today, not someday.”

The announcement comes at the beginning of a critical two-year period for Ford and on the heels of a fourth quarter that delivered a $2.8 billion loss. The automaker will ramp up deliveries of its all-electric Mustang Mach-E vehicle and the Bronco Sport (which is not an EV). The first electric E-Transit commercial vans will come off the line in late 2021. Meanwhile, development continues on an all-electric F-150 pickup that is coming in mid- 2022.

And don’t forget that Ford is also planning to use Google’s Android Automotive operating system in new vehicles, beginning in 2023 as part of a six-year partnership announced February 1 that will bring embedded Google apps and services to drivers.

Ford’s announcement comes a week after GM said it aspired to produce only electric vehicles by 2035.

We often hear about companies working to improve the customer experience, but for IT their customers are the company’s employees. Nexthink, a late stage startup that wants to help IT serve its internal constituents better, announced a $180 million Series D today on a healthy $1.1 billion valuation.

The firm, which was founded in Lucerne, Switzerland and has offices outside of Boston, received funding from Permira with help from Highland Europe and Index Ventures. The company has now raised over $336 million, according to Crunchbase data.

As you might imagine, understanding how folks are using a company’s technology choices internally is always going to be useful, but when the pandemic hit and offices closed, having access to this type of data became even more important.

Nexthink CEO and co-founder Pedro Bados says that most monitoring tools are focused on figuring out if the systems are working correctly and finding ways to fix them. Nexthink takes a different approach, looking at how employees are adopting the tools a company is offering.

“What we do at Nexthink is to take the [monitoring] problem from a completely different perspective. We say that we’re going to give your IT department a real time understanding of how employees are experiencing IT [at your company],” Bados told me.

He says that they do this by looking at the problem from the employees’ perspective. “At the end of the day we’re giving all the insights to IT departments to make sure they can improve the digital experience of their employees,” he said.

This could involve querying the user base in the same way that HR and marketing survey tools allow companies to check the pulse of employees or customers. By gathering this type of data, it helps IT understand how employees are using the company’s technology choices.

This software is aimed at larger organizations with at least 5000 employees. Today, the company has over a 1000 of these customers including Best Buy, Fidelity, Liberty Mutual and 3M. What’s more, the company has surpassed $100 million in annual recurring revenue, a success benchmark for SaaS companies like Nexthink.

Nexthink currently has 700 employees with plans to reach 900 by the end of this year, and as a maturing startup, Bados has given a lot of thought on how to build a diverse workforce. Just being spread out in two countries gives an element of geographic diversity, but he says it takes more than that, and it all starts with recruitment.

“The way to make sure we get more diversity is we look at recruitment and make sure that we have a balanced pipeline. That’s something we measure as a company,” he said. They also have a diversity committee, which is charged with delivering diversity training and figuring out ways to hire a more diverse and inclusive workforce.

While the company has a healthy valuation and a good amount of money in the bank, Bados doesn’t see an IPO for at least a couple of years. He says he wants to double or triple the business before taking that step. For now, though with $180 million in additional runway and a $100 million in ARR, the company is well positioned for whatever future moves it chooses to make.

Source: https://techcrunch.com/2021/02/08/nexthink-nabs-180m-series-d-on-1-1b-valuation/

Elon Musk notified the world that he would be donating $100 million to pursue new technologies for carbon capture, methods through which carbon dioxide can be actively extracted from the atmosphere as a means to help stave off climate change. As TechCrunch reported in January when he made the tweet, Musk’s sizeable pool of monetary incentive would be going to the Xprize foundation, a non-profit that has organized similar ambitious technology competitions aimed at developing world-changing tech. Now, Xprize and Musk have released new details of the competition.

The entire $100 million prize pool is up for grabs with this competition, which will seek solutions that can “pull carbon dioxide directly from the atmosphere or oceans and lock it away permanently in an environmentally benign way.” That’s an ambitious goal, and one that seeks methods for carbon extraction which have a net negative effect on the overall global balance of the element’s presence. Xprize aims to award up to 15 finalists $1 million each, along with three top winners, with $50 million to the Grand Prize victor, and $20 million and $10 million respectively for second and third place. 25 student scholarships valued at $250,000 each will also be up for grabs specifically for student team entrants.

To qualify for victory, solutions must be able to extract 1 ton of CO2 per day, and be viable in a scaled, validated model at time of presentation, with the ability to scale it to “gigaton levels” in commercially viable ways in future. Those are big goals for new technologies, but the competition’s stakes are high: Musk has frequently referred to climate change as an existential threat to humanity, and carbon capture is one key means to combat it.

Carbon capture methods exist, and some are at the center of new startups and emerging businesses, like Canadian company Carggon Engineering which uses CO2 extracted from the atmosphere to create new types of fuel, or Air Vodka, a carbon negative vodka distilled using C02 removed from the atmosphere. Though there are a handful of companies pursuing this, the problem is that it’s typically very expensive to remove carbon in a way that is both safe and that has no subsequent impact on the environment from its resulting byproducts.

The new Xprize competition hopes to spur the development of a wide range of emerging companies in a way similar to how the the 2004 $10 million private spaceflight Ansari Xprize led the development of a whole new era in the space industry. The competition will officially begin on April 22, 2021, at which time full guidelines will be made available and registration will open. Applicants will have up to four years to submit their solution, with the competition closing on Earth Day 2025 and the initial $1 million awards distributed after 18 months following that. That will provide the funding necessary for teams to build out their full-scale demos to claim the top prizes.

VerSe Innovation, the parent firm of popular news and entertainment app Dailyhunt and short video app Josh, said on Monday it has raised over $100 million as part of a Series H financing round from Qatar Investment Authority and Glade Brook Capital Partners.

The announcement follows another $100 million+ investment the startup secured from Google, AlphaWave, and Microsoft in December last year. That investment, also part of Series H, had turned Dailyhunt into a unicorn (giving it a valuation of $1 billion or higher). The startup has to-date raised about $430 million.

Dailyhunt, co-run by Virendra Gupta and former Facebook India head Umang Bedi, is a popular news and entertainment app that serves more than 285 million users each day in 14 local languages in India. Its reach in India, the world’s second largest internet market, would explain why Twitter last month partnered with the Indian firm to bring Moments to Dailyhunt.

VerSe Innovation expanded to short form videos last year, with Josh, after New Delhi banned TikTok and created a theoretical void for snacking content in the country. Scores of large giants and startups — including MX Player and ShareChat — have attempted to try their hand at short form videos in the recent quarters.

Facebook launched Instagram Reels in India last year, and YouTube launched Shorts, which is already garnering over 3.5 billion daily views in India, it said last month. (With over 450 million users in India, YouTube is closing in on WhatsApp’s market lead in India.)

Josh appears to have emerged as one of the leading players: The startup says Josh has amassed over 85 million monthly active users — 40 million of whom check the app each day — and the app sees more than 1.5 billion video plays everyday.

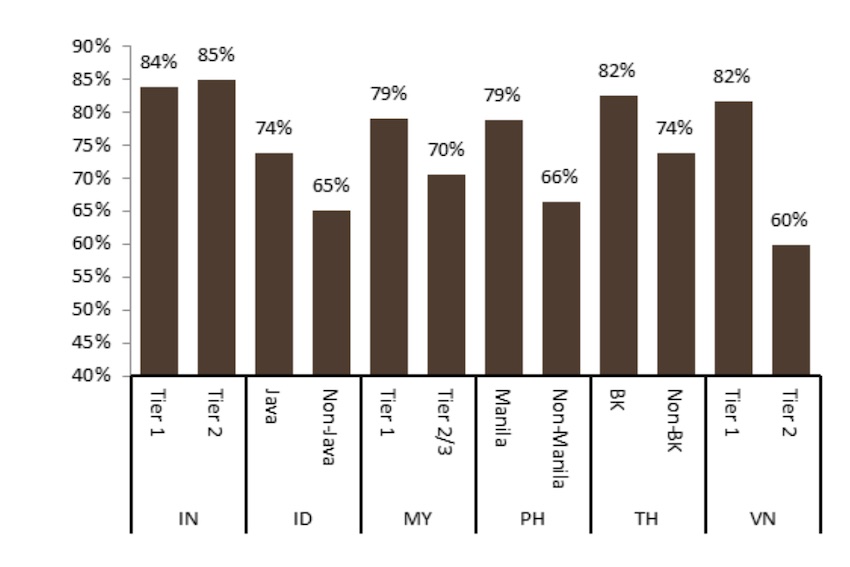

India’s internet economy is expected to be worth $639 billion by 2030, analysts at Citi wrote in a report to clients late last month. The coronavirus pandemic accelerated digital adoption and users’ appetite to transact online, a report from analysts at UBS said last week.

India leads with Tier 2 cities comparable to Tier 1. Biggest catch up opportunity in Philippines and Vietnam (UBS)

“Josh represents a confluence of India’s top 200+ best creators, the 10 biggest music labels, 15+ million UGC creators, best in class content creation tools, the hottest entertainment formats, and formidable user demographics. Josh has been consistently rated as the leading Indian short-video app in India on the Play store,” the startup said in a statement.

The startup said it will deploy the fresh capital to broaden its local languages content offering, and expand its creators ecosystem and AI and ML tech stacks.

Source: https://techcrunch.com/2021/02/07/dailyhunt-and-joshs-parent-firm-raises-over-100-million/

ByteDance is bringing its battle with archrival Tencent to the court at a time when the Chinese government moves to curve the power of the country’s internet behemoths.

The Beijing Intellectual Property Court has permitted a ByteDance lawsuit brought against Tencent to proceed, a ByteDance spokesperson confirmed with TechCrunch. Upstart new media company ByteDance alleged that Tencent’s restrictions on Douyin, the Chinese version of TikTok, are in violation of China’s anti-monopoly draft rules. Douyin is headquartered in Beijing while Tencent’s base is in Shenzhen.

For three years, Tencent has blocked Douyin from its flagship networking apps WeChat and QQ, which bans users from viewing or sharing content from the short video app. Tencent’s behavior “no doubt” constitutes “monopolistic behavior achieved by abusing market domination to exclude and limit competition,” which the proposed anti-monopoly law prohibits, Douyin, said.

“We believe that competition is better for consumers and promotes innovation. We have filed this lawsuit to protect our rights and those of our users.”

Tencent said in response the accusation is false and malicious defamation. It further asserted that Douyin, which is used by 600 million users every day, uses illegal and anti-competitive methods to access WeChat’s user data, and it’s planning to sue ByteDance for harming its platform ecosystem and user rights.

ByteDance and Tencent each covet the other’s turf. ByteDance debuted a chat app to take on Tencent’s dominance in social networking, while Tencent countered Douyin’s popularity by introducing a slew of short video apps. Neither has managed to threaten the other’s dominance in their respective field.

Early signs show that the Chinese government is increasingly willing to rein in monopolistic behavior on the Chinese internet following two decades of relatively lax regulations.

In November, the country’s top market regulator unveiled the draft version of its first anti-monopoly law, opening a floodgate to lawsuits and investigations. In December, regulators launched an antitrust probe into Alibaba for forcing vendors to sell exclusively on its platform. Just this month, a court in Beijing imposed a 3 million yuan ($464,000) fine on fashion e-commerce site Vipshop over anti-competitive behavior. It won’t be surprising to see more Chinese internet giants getting hit by anti-trust actions in the upcoming months.

Source: https://techcrunch.com/2021/02/07/bytedance-tencent-lawsuit/