& meet dozens of singles today!

User blogs

Last week, another container security startup came off the board when Rapid7 bought Alcide for $50 million. The purchase is part of a broader trend in which larger companies are buying up cloud-native security startups at a rapid clip. But why is there so much M&A action in this space now?

Palo Alto Networks was first to the punch, grabbing Twistlock for $410 million in May 2019. VMware struck a year later, snaring Octarine. Cisco followed with PortShift in October and Red Hat snagged StackRox last month before the Rapid7 response last week.

This is partly because many companies chose to become cloud-native more quickly during the pandemic. This has created a sharper focus on security, but it would be a mistake to attribute the acquisition wave strictly to COVID-19, as companies were shifting in this direction pre-pandemic.

It’s also important to note that security startups that cover a niche like container security often reach market saturation faster than companies with broader coverage because customers often want to consolidate on a single platform, rather than dealing with a fragmented set of vendors and figuring out how to make them all work together.

Containers provide a way to deliver software by breaking down a large application into discrete pieces known as microservices. These are packaged and delivered in containers. Kubernetes provides the orchestration layer, determining when to deliver the container and when to shut it down.

This level of automation presents a security challenge, making sure the containers are configured correctly and not vulnerable to hackers. With myriad switches this isn’t easy, and it’s made even more challenging by the ephemeral nature of the containers themselves.

Yoav Leitersdorf, managing partner at YL Ventures, an Israeli investment firm specializing in security startups, says these challenges are driving interest in container startups from large companies. “The acquisitions we are seeing now are filling gaps in the portfolio of security capabilities offered by the larger companies,” he said.

SoftBank reported earnings today, including the performance of its $98.6 billion Vision Fund. The numbers were enticing given the recent exit of DoorDash, which returned billions to SoftBank and represents one of its first truly blockbuster investments out of the fund. The company has now seen 18 investments exit, including 10 fully exited and eight that are now trading on the public markets.

Yet, tucked away deeply in the company’s earnings statement was a note that the company has cut the performance incentive earmarked for the Vision Fund’s leadership in half, from $5 billion to $2.5 billion.

That $5 billion incentive scheme was controversial when news of it was first reported by publications like the Financial Times back in April 2018. In the model, SoftBank essentially loaned its employees money to buy into the Vision Fund, a structure that was designed to accelerate the closing of the fund’s $100 billion fundraise. The company first added language about the incentive scheme in its 2018Q2 earnings, writing:

On October 19, 2018, SoftBank Vision Fund completed an interim closing with additional committed capital of $5 billion. This brought the total committed capital of the Fund to $96.7 billion. The additional committed capital is intended for the installment of an incentive scheme for operations of SoftBank Vision Fund.

Since then, the company has had consistent language about the $5 billion figure in every quarterly earnings report. However, in today’s latest earnings for fiscal 2020Q3, the company noted that the incentives are now “$2.5 billion (decreased from the previous $5.0 billion).”

The incentive scheme for SoftBank has been a huge point of discussion for industry observers. Four top executives at SoftBank — Rajeev Misra, Marcelo Claure, Katsunori Sago and Ken Miyauchi have collectively been loaned $600 million to buy into the Vision Fund, according to a report two weeks ago in the Financial Times. Some of that money was derived from the $5 billion (now $2.5 billion) incentive scheme, although it isn’t clear if all that money was earmarked exclusively from this particular pool.

SoftBank’s pullback on incentives for the Vision Fund is seemingly a response to the fund’s overall lackluster performance and the fund’s disastrous investment in WeWork, which led to wide losses at the telecom group. While more recent performance has been much better for the fund, eliminating some of those incentives should improve overall performance of the fund and ultimately SoftBank’s bottom line.

Vision Fund I has stopped investing in new companies as of last year. A second fund has $10 billion in capital — all from SoftBank itself — and has been making regular investments. The Vision Fund has also been raising SPACs, including two new ones it announced late last week.

The French government and the government-backed initiative La French Tech unveiled the new indexes that identify the most promising French startups. The 40 top-performing startups are called the Next40, and the top 120 startups are grouped into the French Tech 120.

The Next40 and French Tech 120 are somewhat new as this is only the second version of those indexes. Out of the 120 startups that were already in last year’s French Tech 120, 90 of them are still in this year’s index — 30 are newcomers as there were 123 startups in last year’s French Tech 120.

Combined, they generate close to €9 billion in revenue and provide a job to 37,500 people. Revenue in particular is up 55% compared to last year’s French Tech 120.

Here’s a list of the French Tech 120 — the red logos are part of the Next40:

Image Credits: La French Tech

There are two different ways to get accepted in the Next40:

- You have raised more than €100 million over the past three years ($120 million at today’s rate) or you are a unicorn, which means your company’s valuation has reached $1 billion or more.

- You generate more than €5 million in revenue with a year-over-year growth rate of 30% or more for the past three years.

As for the remaining 80 startups in the French Tech 120:

- 40 of them have raised more than €20 million in a funding round over the past three years.

- 40 of them are selected based on the annual turnover and growth rate.

Of course, those indexes are limited to private French companies. For the French Tech 120, there are at least two startups per administrative region.

Based on those metrics, only a handful of the startups in the French Tech 120 have a female CEO and the French government thinks tech startups should do more when it comes to diversity and inclusion. That’s why a small group of people are going to work on a roadmap and some recommendations to improve those numbers.

Representatives of six different startups in the French Tech 120 as well as people from Sista, Tech Your Place and Future Positive Capital will get together to work on those topics.

In addition to a cool logo for your website, being part of the French Tech 120 comes with some perks. Those companies can access a network of French Tech representatives in different public administrations.

For instance, it’s easier for your company if you want to get visas for foreign employees, obtain a certification or a patent, if you want to sell your product to a public administration, etc.

There are two new additions to the French Tech network. Someone from the Conseil d’État can help you when it comes to legal compliance. The government has also signed a partnership with Euronext to educate entrepreneurs about going public.

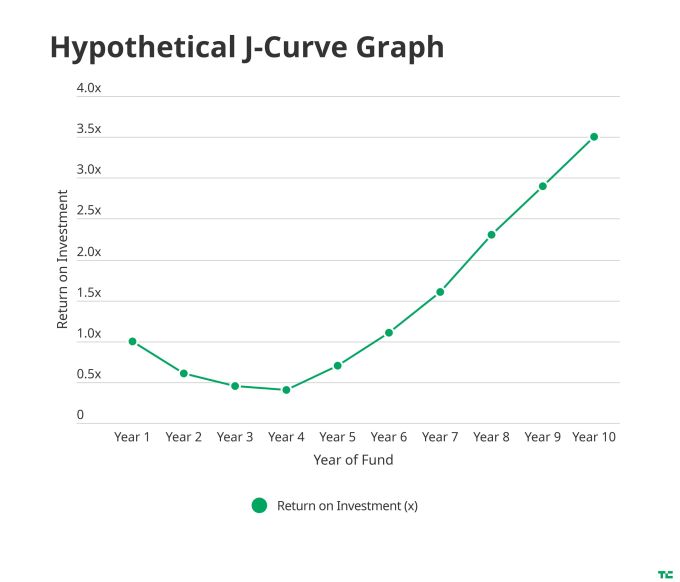

SoftBank had some good data to report overnight with its third-quarter earnings, which covers the last quarter of 2020 through December 31. The company’s first Vision Fund reported large gains driven by DoorDash, where the company’s $680 million investment blew up to just shy of $9 billion — a 13.2x return in SoftBank’s math. While not the first exit from the fund nor the first high-returning exit SoftBank has had, it is the first exit that meaningfully shakes up the prognosis for the Vision Fund’s returns.

Now seems as good a time as any to ask a question we first started pondering when SoftBank launched the Vision Fund way back in 2017: what does a return profile look like at such a late stage of investment?

Early-stage venture capital has a return profile dubbed the “J-curve.” Given a cohort of startups in a venture portfolio, the failures of that cohort tend to materialize quite quickly. Those startups can’t raise money, and thus, they run out of runway and either die or are sold off. That means that the losses from those investments are recognized by investors right away. Meanwhile, the successful startups keep growing and raising venture capital, but funds won’t realize their gains for potentially a decade or more. Thus, the J-curve describes the early years of a fund where the losses are visible but the future gains have not yet materialized.

The Vision Fund pioneered a much more muscular form of traditional mezzanine (pre-IPO) capital, where it would barge into a company’s cap table with big dollars and high valuations with the dream that these companies would go big. While not true of all of the Vision Fund’s investments, many of these startups were quite mature with serious revenues where the alternative to mezzanine capital was an IPO.

That brought up an interesting fund construction question: the sort of immediate failures that create the J-curve for early-stage investors shouldn’t presumably exist at later stages, where startups are less risky investments. Sure, some startups may grow more slowly than other companies and exit for a middling return, but few startups should actually fail entirely.

So what does the SoftBank data look like today and what can it tell us about late-stage fund performance?

SoftBank Vision Fund I made a total of 92 investments from summer of 2017 to mid 2020, of which 10 have fully exited, and 8 are now traded on the public markets. According to SoftBank, 25 of its Fund I portfolio companies received another venture capital round in calendar year 2020 as well, giving the firm some upticks in its fair-market valuation.

Source: https://techcrunch.com/2021/02/08/softbank-and-the-late-stage-venture-capital-j-curve/

InEvent, a startup powering virtual and hybrid events, is announcing that it has raised $2 million in seed funding from Storm Ventures.

That’s just tiny fraction of the $125 million that online events platform Hopin raised last fall — in fact, a recent Equity episode suggested that Hopin might be the fastest growth story of the current startup era.

CEO Pedro Góes told me that even in a world of more established and better-funded platforms, his team sees an opportunity to break out by focusing on business-to-business events.

“There’s an opening in the space space for us to be the leader that we want on B2B,” Góes said. “We don’t intend to compete with platforms in the B2C market.”

Put another way, InEvent is less focused on replicating giant consumer events and more on helping businesses hold virtual events where they can connect with clients and partners. Góes said this is something that he and his co-founder saw Mauricio Giordano and Vinicius Neris saw in their previous work running a digital agency, where they were often asked to help with events in this vein.

“Since we had a lot of experience with events, we could see where the industry was broken and how to fix it,” he said.

Image Credits: InEvent

Góes suggested that two of the big needs for B2B events are customization and support, so InEvent has created what he described as a “really beautiful” product that can still be customized with the organizer’s branding, and the company also offers 24-hour support.

The platform that a virtual lobby where participants can browse all the programming, a video player, a registration system, the ability to create a conference mobile app and more. Góes said the goal was to build something that was “really flexible,” allowing organizers to run everything from within InEvent while also allowing them to incorporate outside tools, whether that’s video platforms like Zoom or CRM software like Salesforce, Marketo and Hubspot.

InEvent’s founders are from Brazil, but the startup is headquartered in Atlanta and has employees in 13 countries. It says it’s been used by more than 500 customers including DowDupont, Coca-Cola and Santander for global events.

With the new funding, Góes told me that startup will be able to expand the team (he was proud to note the team’s diversity — 50% of its managers are women, and 50% of its managers come from a Latinx background). It will also continue to develop the product, for example by improving the video player and adding more marketing automation.

And when the pandemic ends and large-scale, in-person conferences become possible again, Góes predicted that there will still be plenty of appetite for what InEvent can do, because more events will bring online and in-person elements together.

“We have different clients where we have a website, we have a mobile app, but we also have hardware [to] connect with in-person,” he said. After all, if you’re at a sprawling conference like CES, it might still be convenient to chat with another attendee through the mobile app, rather than traveling two miles to see them face-to-face. “For us, what we are building, the technology for virtual and in-person, is the same thing.”

Source: https://techcrunch.com/2021/02/08/inevent-seed-fundng/