& meet dozens of singles today!

User blogs

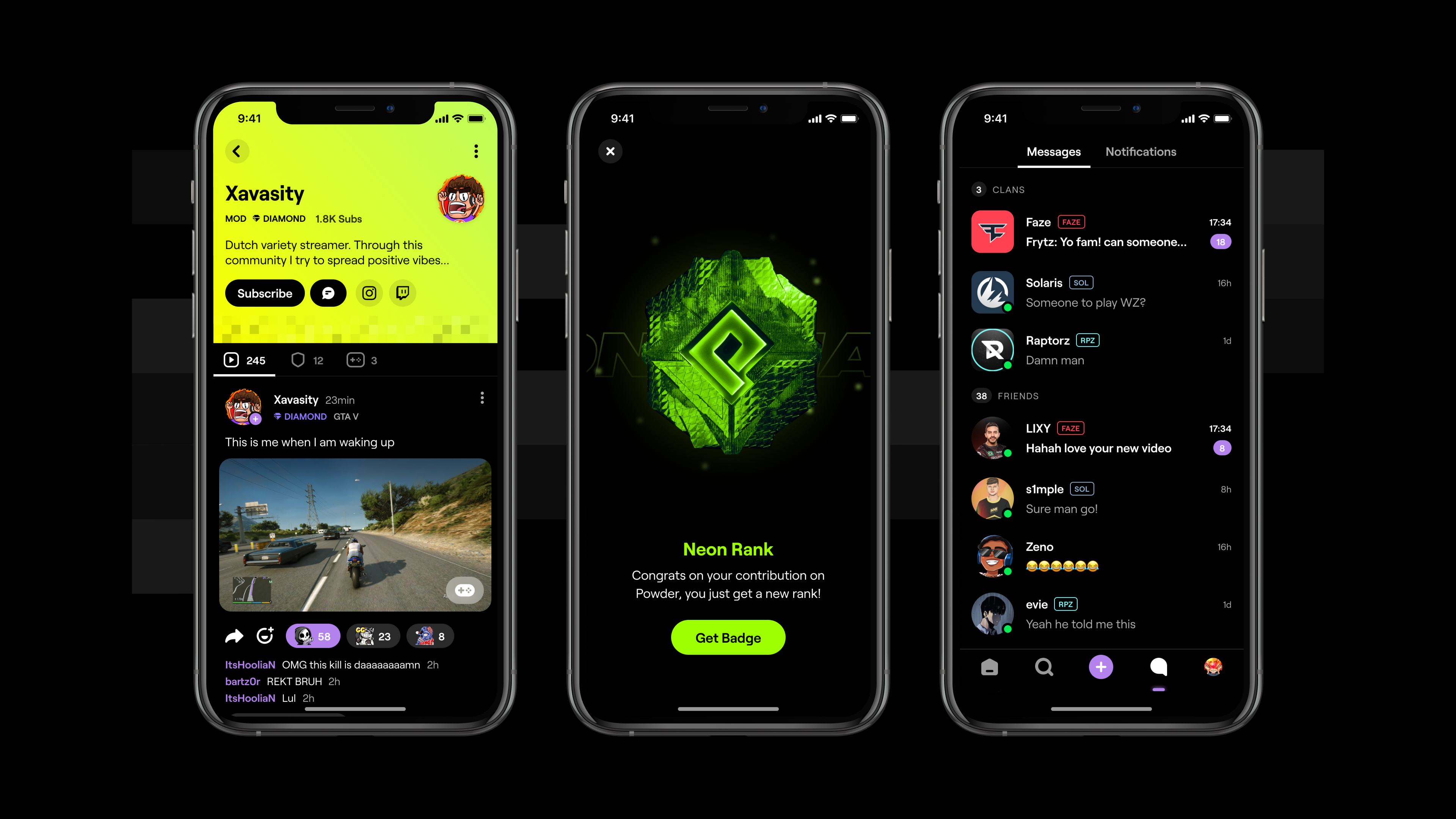

Meet Powder, a French startup that helps you share video clips of your favorite games, follow people with the same interests and interact with them. The company has raised a $14 million Series A round led by Serena.

Powder wants to build the video infrastructure for social gaming. While many communities of gamers already share content on Twitch, Discord and Reddit, there isn’t a dominant mobile app focused on gaming.

You could call it an Instagram or Snapchat for gamers, but the startup has built specific tools that make it similar and yet different from those mainstream social platforms.

Powder can capture video content from any platform. You can record with your console and access your footage by connecting your account with Powder. You can capture videos on your PC using the company’s desktop app. You can also capture videos of mobile games.

The company tries to identify the most relevant events in your favorite game — it can be when you score a goal on Rocket League, when you are the last person standing in Fortnite, etc.

You can then trim your video, add filters, music and stickers and share a video with your followers. Other users can share reactions, add comments and send messages.

Image Credits: Powder

Overall, the company has raised $18 million and is pretty transparent about its funding story. In August 2018, the company raised a $400,000 pre-seed round with Kima Ventures and the co-founders of Zenly Antoine Martin and Alexis Bonillo. In March 2019, General Catalyst, Slow Ventures, Dream Machine, SV Angel, Brian Pokorny, Florian Kahn and Guillaume Luccisano invested $1.5 million.

Around May 2020, the company had to raise a $1.3 million seed extension with Alven Capital, Seraam Invest, Farmers, Maxime Demeure, Jean-Nicolas Vernin and some existing investors. Bpifrance and CNC also put some money in the company. And now, Serena is leading the $14 million Series A round with General Catalyst, Slow Ventures, Alven Capital, Bpifrance’s Digital Venture fund, Secocha Ventures, Turner Novak and Kevin Hartz also participating in today’s round.

As you can see, it’s been a long and winding road. That’s because Powder didn’t come up with its social app for gamers overnight. The company tried many different consumer apps. It would iterate on an idea for a few weeks and then kill the concept if it didn’t pan out. With Powder, the company seems to have found a great distribution mechanism to attract more downloads, leading to more users.

“The idea behind Powder started in December 2019. We had already worked on several projects and none of them really took off. We thought we would create a community first and then a product,” co-founder and CEO Stanislas Coppin told me. He previously co-founded Mindie, a music video app.

Powder started as a Discord server with tens of thousands of members. The team then developed an app that would appeal to that community, the “metaverse camera” as Coppin says. Overall, 1.5 million people have downloaded the iOS app since its launch.

There are three other co-founders, Barthélémy Kiss, Yannis Mangematin and Christian Navelot. There are 18 employees and the company just launched on Android.

Image Credits: Powder

Source: https://techcrunch.com/2021/02/10/powder-raises-14-million-for-its-social-app-for-game-clips/

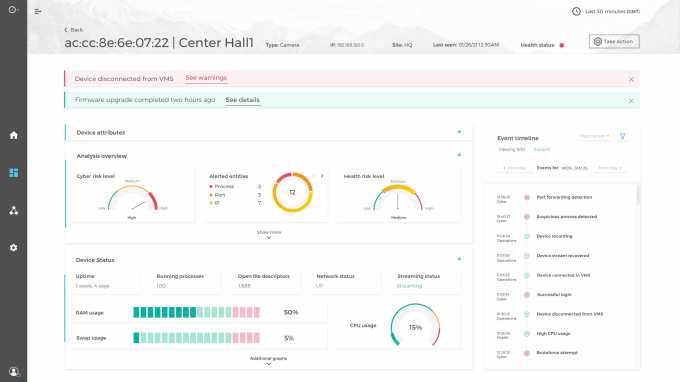

Managing IoT devices in a large organization can be a messy proposition, especially when many of them aren’t even managed directly by IT and often involve integrating with a number of third-party systems. SecuriThings wants to help with a platform of services to bring that all under control, and today the startup announced a $14 million Series A.

Aleph led the round with participation from existing investor Firstime VC and a number of unnamed angels. The company has raised a total of $17 million, according to Crunchbase data.

Roy Dagan, company CEO and co-founder says that he sees organizations with many different connected devices running on a network and it’s difficult to manage. “We enable organizations to manage IoT devices securely at scale in a consolidated and cost efficient manner,” Dagan told me.

This could include devices like security cameras along with access control systems and building management systems involving thousands — or in some instances, tens of thousands — of devices.”The technology we build, we integrate with management systems, and then we deploy our capabilities which are focused on the edge devices. So that’s how we also find the devices, and then we have these different capabilities running on the edge devices or fetching information from the edge devices,” Dagan explained.

Image Credits: SecuriThings

The company has formed partnerships with a number of key device manufacturers including Microsoft, Convergint Technologies and Johnson Controls, among others. They work with a range of industries including airports, casinos and large corporate campuses.

Aaron Rosenson, general partner at lead investor Aleph, says the company is solving a big problem managing the myriad devices inside large organizations. “Until SecuriThings came along, there were these massive enterprise software categories of automation, orchestration and observability just waiting to be built for IoT,” Rosenson said in a statement. He says that SecuiThings is pulling that all together for its customers.

The company was founded in 2016 originally with the idea of being an IoT security company, and while they still are involved in securing these devices, their ability to communicate with them gives IT much greater visibility and insight and the ability to update and manage them.

Today, the company has 30 employees, and with the new investment it will be doubling that number by the end of the year. While Dagan didn’t cite specific customer numbers, he did say they have dozens of customers with deal sizes of between five and seven figures.

Fiverr is adding a new way for freelancers on the marketplace to charge for their work — three- or six-month subscriptions.

Through this feature, sellers on Fiverr can offer to provide a defined set of work each month. They can also offer discounts to subscribers, although it’s not required. The buyer or seller can cancel at any time, with no fees paid on the remaining months of the subscription — but the savings only start in the second month, to prevent situations where buyers might try to use subscriptions just to get a one-time discount.

Product Manager Natasha Shine-Zirkel told me that that while Fiverr built its reputation as a marketplace to hire freelancers on a “one-time or per-project basis,” it’s increasingly become a home for ongoing work as well. So the company decided to make it easier to provide and pay for that work.

She said businesses who sign up for a subscription will get access to “high-quality sellers and build long-term relationships,” and it also “saves them hassle of filling out their requirements each time.” Sellers, meanwhile, will get more predictability in their workload and revenue.

Fiverr Subscriptions are being made available to what the company said are the “top freelancers” in eight categories, including social media marketing, SEO and voice overs.

Shine-Zirkel said Fiverr is starting out small to “learn from sellers who are really high quality and already have existing relationships.” She added that the initial categories represent a mix of work that’s normally retainer-based and other jobs that are more project-based, allowing the company to observe “how buyers and sellers use the feature” in different contexts.

At the same time, Shine-Zirkel described this as “just the beginning,” with Fiverr rolling the feature out to more freelancers in more categories over time.

In addition to launching support for subscriptions, Fiverr is introducing another feature around longer-term work called Milestones, where a bigger job is broken down into smaller pieces, with the buyer paying for each milestone as it’s completed.

Source: https://techcrunch.com/2021/02/10/fiverr-subscriptions/

If you are a founder and launched a startup last February of 2020 just before the pandemic hit, then you may have felt like you were living the ultimate business nightmare. But if your company serves to stabilize the supply-chain business, then, in fact, you may have hit the ground running at just the right time. So is the story of Miami-based startup SmartHop, an AI-powered app that helps interstate truckers make their routes more efficient and lucrative, while removing a lot of the administrative hassle for drivers.

SmartHop announced today that it raised $12 million in a Series A round, bringing the company’s total funding to date to $16.5 million. The round was led by Union Square Ventures, whose past investments include Stripe, Twitter, Coinbase, Etsy, MeetUp, SkillShare and Duolingo, among others.

SmartHop takes a complex problem with lots of moving parts and offers a simple solution. To understand the gap in the market, you need to understand the hurdles that interstate truck drivers face. And since Garcia is a former truck driver himself (he was a pet food delivery driver while in college in his native Venezuela and scaled his business to a 500-person trucking company), he has a good grasp on the pain points and intricacies of the industry.

“I lived with my parents in Caracas and I asked my parents to empty their garage and that was my first distribution center,” said Guillermo Garcia, CEO and co-founder of SmartHop, of his experience starting his first trucking company. “The trucking market moves like the stock market,” he added, explaining that it’s ever-changing and therefore impossible to predict.

According to a 2019 study by The American Trucking Associations, the trucking industry is a $791.7 billion industry, representing 80.4% of the nation’s freight bill. Additionally, 91% of trucking companies are small businesses, meaning they have six trucks or fewer. Many are owner-operators. Traditionally, to get loads, truckers had to scour apps or websites of about 15,000 different brokers. It was a total uncoordinated, inefficient, free-for-all approach that left drivers unable to predict their monthly revenues, among many other things.

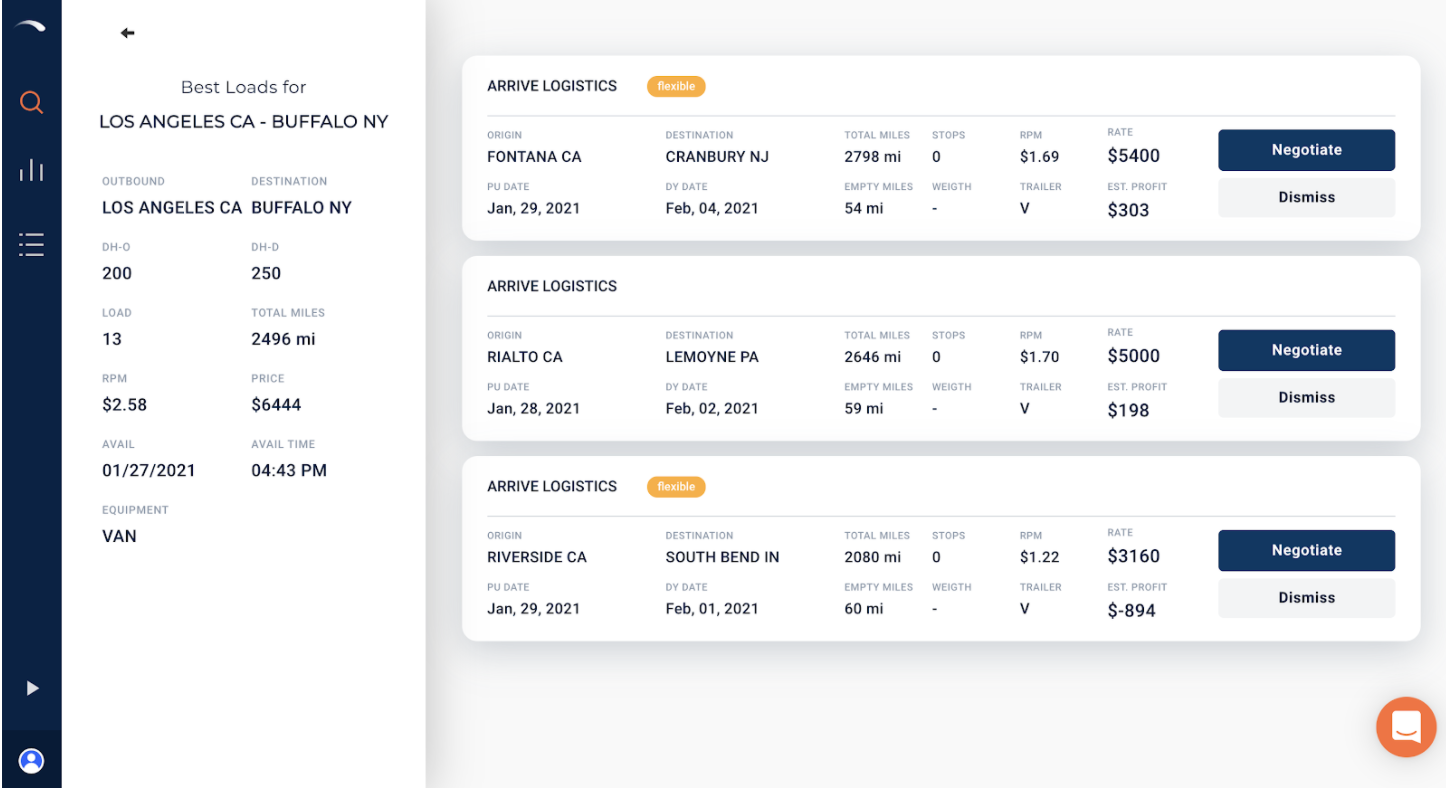

This is how SmartHop helps those drivers. Let’s say Bob lives in Atlanta and he has a single truck; he’s an owner-operator. He has a load that’s going to take him all the way to Seattle, and it’s going to take him several days to get there. Financially, it doesn’t make a lot of sense for Bob to start the trip without knowing what else he can pick up along the way, or if Seattle should really be his turnaround point. Maybe there’s not a lot of freight leaving Seattle these days, but there’s a lot going out of Chicago. There’s no way for Bob to know these things.

Before SmartHop, Bob had to pick up the phone, call brokers and make deals. Most of this work was done while on the road and Bob had no foresight into his next couple of weeks of work – or life, for that matter.

With SmartHop, Bob can enter details about his truck’s capacity, cities he doesn’t like driving through and other details, and SmartHop will recommend loads to him that optimize his profits and travel time. Think of it like when you’re driving and using Waze and it asks if you want to drive to Starbucks because it’s a couple of minutes out of the way. All you have to do is accept, and Waze does the rest. SmartHop operates similarly.

SmartHop technology giving a driver three load booking options, which the platform’s tech will negotiate and book (image: SmartHop).

“Some truckers don’t like to drive through New York City because there are a lot of tolls, bridges and traffic,” said Garcia, “So it doesn’t matter the value of the load, he’s just not going to pick it up,” he added.

But if you really want to go full autopilot, SmartHop can take over and autonomously book the loads for you – all you have to do is drive and take care of the truck, Garcia said.

The more a trucker uses SmartHop, the more the company learns the driver’s preferences and makes better suggestions or bookings.

SmartHop charges a transaction fee of 3% of the gross sale. “Our incentives are very aligned, so when they make money, we make money, and when they are taking days off, we don’t charge anything,” said Garcia.

“[Union Square Ventures] is focused on businesses that utilize technology to build networks and broaden access,” said Rebecca Kaden, managing partner at Union Square Ventures. “We were particularly excited to meet Guillermo and the SmartHop team, because that’s exactly what they are doing — software empowers the owner-operator trucking company to optimize their business and compete with players far bigger in number.”

Ryder, the Miami-based logistics company, also participated in the round through its new venture arm, RyderVenture. SmartHop is its first investment. Equal Ventures and Greycroft, from SmartHop’s seed round, also invested.

“A lot of startups have a lot of good technology and no one to test it on,” said Karen Jones, Ryder executive VP, CMO and head of new product innovation. “And the software doesn’t go very far if there is no one in the real world to try it.” Prior to the RyderVenture investment, Ryder partnered with SmartHop to test the product on its own trucks, of which they have 275,000.

The company, which was part of the 2019 New York City Techstars cohort, currently has 50 full-time employees and 100 trucks using the product. Each truck, on average, grosses between $10K – $15K per month.

The latest funding round will go toward product development as well as embedded financial products. Unlike big companies, smaller trucking companies don’t have the leverage to negotiate better rates on fuel or insurance, but with SmartHop’s volume of drivers, it can change that. Additionally, they’ll be offering to factor invoices, so drivers can sell a 45-day invoice and get paid within just 24 hours by SmartHop. “Because we have so much data, we become the ultimate underwriter so I’m able to underwrite in advance, and much smarter,” said Garcia.

Source: https://techcrunch.com/2021/02/10/smarthop-raises-a-12m-series-a-to-ease-trucking-logistics/