& meet dozens of singles today!

User blogs

Taavet Hinrikus, the first employee of Skype and co-founder of fintech giant Wise (formerly TransferWise), is teaming up with Teleport co-founder and current Topia CPO Sten Tamkivi to create a new investment vehicle.

Both are already seasoned investors — Hinrikus is one of Europe’s bona fide super angels, with over 100 investments to his name — and have already done a number of tickets together. The new as yet unnamed venture will see the pair’s investment activities formalised as an equal partnership and be supported by a team of six people based in Estonia, including an investment analyst.

Just don’t call it a VC fund.

“I’m still not setting up a fund, but am partnering to help do more of the same on the investing side,” Hinrikus told me last week in a text message.

For the last few years — perhaps prompted by swapping the role of CEO of Wise for chairperson — there’s been speculation within London’s increasingly chatty venture capital scene that he might raise a fund of his own or join an A-list VC firm as a partner. The Wise founder actually spent about a year as a venture partner at Mosaic Ventures, which ended last summer and went unreported.

“When you say fund, this means other people’s money and a specific mandate (i.e. invest in seed or late, in biotech or fintech, promise to return the money in a certain time, etc.),” Hinrikus said in an email earlier this week. He also explained that the new firm will not be seeking outside LPs and will be “evergreen”, enabling it to make considerably longer-term bets than many VC funds. Instead, Hinrikus and Tamkivi are happy to hold investments for 10-20 years.

“This structure is both liberating and differentiating, because without strict external mandates we can go after the missions we feel passionate about and be really patient about how long we stay involved in our companies,” said Tamkivi in an email.

“[We] will not be the one pushing a founder to sell,” underlines Hinrikus. “Will always stay on the founder’s side as we’ve been in that position ourselves”.

The pair’s combined portfolios focus mostly on Europe but also further afield, including the U.S., Japan and Singapore. Mutual investments (or shareholdings) include Wise, Bolt, Veriff, LHV, Xolo, Oyster HR, Pactum, Starship, Curve, Sunrise and Acapela.

Hinrikus and Tamkivi have also jointly contributed to several “mission driven” nonprofit endeavours such as Jõhvi School of Technology, Good Deed Education Fund or Vabamu Museum of Freedom and Occupations, which they, and the new firm’s back office, will continue to support. Most recently, Hinrikus co-founded Certific, which is building the rails for home health testing.

Hinrikus and Tamkivi say their new investment firm will back tech companies with a €250,000 to €1 million seed investment, but also has the freedom to follow on right up to an IPO. In most instances, it doesn’t expect to lead rounds but hopes to be seen as more collaborative than competitive.

“In short, we will be doing more of the same: give founder-backing to more upcoming founders,” said Hinrikus. “What excites us most is the future ahead and finding positive missions that improve our future. So far it’s been lots of future of work, future of finance, but in the future we’d love to think more about future of health and climate as well”.

“It will take a bit more conscious effort to figure out what our theses and strategy will be for completely new areas,” adds Tamkivi. “As humans, we both care about longevity, health, education, democracy — if we find ways how to move these huge problem spaces along with capital, we are very eager to learn”.

The pair are also willing to take positions in crypto tokens, real assets or any alternative financial instruments.

“On a high level you can think of DeFi as just a natural extension of our broader ‘future of money’ financial freedom thesis,” said Tamkivi. “When it comes to technical execution, we’ve benefited a lot from the freedom to invest not just in equity of established companies, but to also take token positions, use on-chain yield strategies or work with specialized venture funds. Whatever helps our founders”.

To that end, the new investment fund is breaking cover with very little fanfare — and, as mentioned, it doesn’t even have a name yet. “’Have you talked to Taavet and Sten yet?’ should work fine for now,” quipped Hinrikus, in his own deadpan style of humour I’ve become accustomed to over the years.

“More seriously, we are just getting started together,” clarified Tamkivi. “[We’re] still figuring out what kind of structure, processes, new talent and other things, such as additional branding, we’ll need as we scale up the activities from our lives as individual angels to date”.

mPharma, a Ghanaian health tech startup that manages prescription drug inventory for pharmacies and their suppliers, today announced its expansion to Ethiopia.

The company was founded by Daniel Shoukimas, Gregory Rockson and James Finucane in 2013. It specializes in vendor-managed inventory, retail pharmacy operations and market intelligence serving hospitals, pharmacies and patients.

In Africa, the pharmaceutical market worth $50 billion faces challenges such as sprawling supply chains, low order volumes, and exorbitant prices. Many Africans still suffer preventable or easily treated diseases because they cannot afford to buy their medications.

With a presence in Ghana, Kenya, Nigeria, Rwanda and Zambia, as well as two unnamed countries, mPharma wants to increase access to these medications at a reduced cost while assuring and preserving quality. The company claims to serve over 100,000 patients monthly and has distributed over a million drugs to Africans from 300 partner pharmacies across the continent.

CEO Rockson says that when mPharma started eight years ago, he wanted to own a pan-African brand with operations in Ethiopia, Kenya, and Nigeria from the get-go.

By 2018, mPharma went live in the West African country. In 2019, the health tech acquired Haltons, the second-largest pharmacy chain in Kenya, subsequently entering the market and gaining 85% ownership in the company. However, it seemed like a stretch to the Ghanaian-based company to expand to the East African country as it met several pushbacks. Rockson attributes this to the harsh nature of doing business with foreign companies.

“Ethiopia is one of the most closed economies on the continent. This has made it a bit hard for other startups to launch there just because the government rarely allows foreign investments in the retail sector.”

According to Rockson, most foreign brands operate in the country through franchising, a method mPharma has employed for its expansion into Africa’s second most populous nation.

The company signed a franchise agreement with Belayab Pharmaceuticals through its subsidiary, Haltons Limited. Belayab Pharmaceuticals is a part of the Belayab Group — a conglomerate that is also an official franchisee of companies like Pizza Hut and Kia Motors in Ethiopia.

Rockson says we should expect the partnership to open two pharmacies in Addis Ababa this year. Each pharmacy will offer the company’s consumer loyalty membership program called Mutti, where they’ll get discounts and financing options to access medication.

Image Credits: mPharma

This franchising is a part of mPharma’s growth plans of enabling companies looking to enter the pharmacy retail sector. The plan is to provide access to a “pharmacy-in-a-box” solution where mPharma handles every infrastructure involved, and the pharmacy is just concerned about the consumer.

“What we’ve done is that we enable these pharmacies with our software, and we have the backend physical infrastructure and warehousing,” he said. ‘They can rely on mPharma to do all the background work from getting the products into your pharmacy and also providing the software infrastructure to be able to run delivery services while they focus on clinical care.”

mPharma is one of the well-funded healthtech startups in Africa and has raised over $50 million. Last year when it secured a Series C round of $17 million, Helena Foulkes, former president of CVS, the largest pharmacy retail chain in the U.S., was appointed to its board. She joined Daniel Vasella, ex-CEO and Chairman of Novartis as members who have decades of experience in the pharmaceutical industry.

This sort of backing, both in expertise and investment, has proven vital to how mPharma runs operations. Rockson doesn’t mince words when saying the company wants to dominate African healthcare with Ethiopia, its toughest market to enter, already secured.

“There are issues of fragmentation in pharmacy retailing, poor standards and high prices that haven’t been fixed. The African opportunity is still huge, and we are still at the beginning stages of privatisation of healthcare on the continent,” he said.

Snyk, a developer of application security technology, is now worth $4.7 billion after a new fundraising and secondary sale that totaled $300 million.

In all, investors have poured $470 million into the company after this new investment, which was led by Accel and Tiger Global, with participation from a host of existing investors including Addition, Boldstart Ventures, Canaan Partners, Coatue, GV, Salesforce Ventures, and funds managed by Blackrock.

New investors joining Accel and Tiger on the cap table included Alkeon, Atlassian Ventures, Franklin Templeton, Geodesic Capital, Sands Capital Ventures and Temasek.

Withe big valuation and very very late stage investors on the cap table, it’s likely that this will be Snyk’s last round before a public offering. And the markets for enterprise software companies have been white hot recently, so the reception for Snyk should be positive.

Snyk’s value and sky high valuation comes from its ability to offer an application security platform that the company said is designed to provide security visibility and remediation for every component of modern applications — including their code, open source libraries, container infrastructure and infrastructure as code.

Investors seem to believe the company’s claims and so do a clutch of key new hires including Chief Marketing and Customer Experience Officer Jeff Yoshimura, a former executive at Elastic; CIO Erica Geil, who previously worked at Groupon; and Vice President, Asia Pacific Japan (APJ) Sales, Shaun McLagan, who previously worked for EMC.

After the funding, Michael Scarpelli, the Chief Financial Officer of the enterprise software darling and last year’s blockbuster public offering, Snowflake, and Ping Li, a longtime enterprise software investor and a Partner at Accel.

“We first met the Snyk team at the start of their journey, as early investors,” said Li, in a statement. “Throughout our partnership, we’ve witnessed first-hand Snyk’s unshakeable dedication to developer and security teams and their original vision become a reality. We’re looking forward to supporting the successes of Snyk in 2021 and beyond.”

Snyk’s financing comes as application vulnerabilities are becoming an increasingly popular attack vector for hackers. Roughly 43% of data breaches have been linked back to flaws in applications, according to the company.

Meanwhile, a dearth of developers focused on security means that automation has to do more heavy lifting. Snyk says it provides that through automated remediation and the integration of security features directly into developer workflows. The company also offers real-time answers to coders’ security questions.

So far, that suite of services has meant more than 27 million developers around the world are using Snyk tools and the company also provides a marketplace for security coders to pitch their own tools on the Snyk platform.

“We believe Snyk’s developer-first approach to security is a fantastic tool for developers and organizations today,” said Chris Hecht, Head of Corporate Development, Atlassian. “Snyk has already showcased some amazing integrations with our tools, and we’re now thrilled to extend our partnership with them through an Atlassian Ventures investment.”

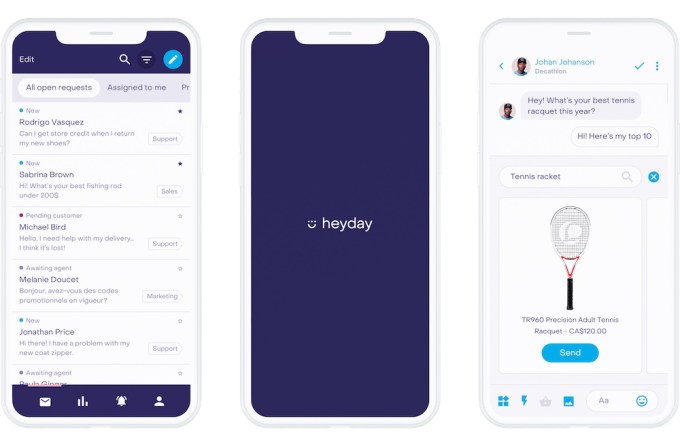

Montreal-based Heyday announced today that it has raised $6.5 million Canadian ($5.1 million in US dollars) in additional seed funding.

Co-founder and CEO Steve Desjarlais told me that the startup’s goal is to allow retailers to support more automation and more personalization in their online customer interactions, while co-founder and CMO Etienne Merineau described it as an “all-in-one unified customer messaging platform.”

So whether a customer is sending a message from Facebook Messenger, WhatsApp and Google’s Business Messages or just via email, Heyday brings all that communication together in one dashboard. It then uses artificial intelligence to determine whether it’s a customer service or sales-related interaction, and it automates basic responses when possible.

Heyday chatbots can provide order updates or even recommend products (it integrates with Salesforce, Shopify, Magento, Lightspeed and PrestaShop), then route the conversation to a human team member when necessary.

There are other platforms that combine customer service and sales, but at the same time, Merineau said it’s important to treat the two categories as distinct and trust that a good service experience will lead to sales in the feature.

Image Credits: Heyday

“We believe that helping is the new selling,” he said.

Desjarlais added, “We’re really against the ticket ID system. A customer is not a ticket …

I truly believe that every single customer is a relationship with a brand that needs to be nurtured over time and that will give more value to the brand over time.”

Heyday was founded in 2017 and says that over the past two quarters, it has doubled recurring revenue. Customers include French sporting good company Decathlon, Danish fashion house Bestseller to food and consumer product brand Dannon — Merineau noted that the platform was “bilingual out of the box” and has seen strong international growth.

“Retailers who believe that [the changes brought about by] COVID-19 are temporary are in the wrong mindset,” he said. “The new mantra of future-forward brands is ‘adapt or die.’ … Brands obviously want to delvier great service, but they care about the bottom line. We help them kill two birds with one stone.”

The startup had previously raised $2 million Canadian, according to Crunchbase. This new round comes from existing investors Innovobot and Desjardins Capital. Merineau said the money will help Heyday “double down on the U.S. and scale.”

The U.S. Department of Defense is setting up a working group to focus on climate change.

The new group will be led by Joe Bryan, who was appointed as a Special Assistant to the Secretary of Defense focused on climate earlier this year.

The move is one of several steps that the Biden administration has taken to push an agenda that looks to address the dangers posed by global climate change.

Bryan, who previously served as Deputy Assistant to the Secretary of the Navy for Energy under the Obama administration, will oversee a group intended to coordinate the Department’s responses to Biden’s recent executive order and subsequent climate and energy-related directives and track implementation of climate and energy-related actions and progress, according to a statement.

The Department of Defense controls the purse strings for hundreds of billions of dollars in government spending and is a huge consumer of electricity, oil and gas, and industrial materials. Any steps it takes to improve the efficiency of its supply chain, reduce the emissions profile of its fleet of vehicles, and use renewable energy to power operations could make a huge contribution to the commercialization of renewable and sustainable technologies and a reduction in greenhouse gas emissions.

The Pentagon is already including security implications of climate change in its risk analyses, strategy development and planning guidance, according to the statement, and is including those risk analyses in its intallation planning, modeling, simulation and war gaming, and the National Defense Strategy.

“Whether it is increasing platform efficiency to improve freedom of action in contested logistics environments, or deploying new energy solutions to strengthen resilience of key capabilities at installations, our mission objectives are well aligned with our climate goals,” wrote Defense Secretary Lloyd Austin, in a statement. “The Department will leverage that alignment to modernize the force, strengthen our supply chains, identify opportunities to work closely with allies and partners, and compete with China for the energy technologies that are essential to our future success.”