& meet dozens of singles today!

User blogs

Welcome back to This Week in Apps, the weekly TechCrunch series that recaps the latest in mobile OS news, mobile applications and the overall app economy. The app industry is as hot as ever, with a record 218 billion downloads and $143 billion in global consumer spend in 2020.

Consumers last year also spent 3.5 trillion minutes using apps on Android devices alone. And in the U.S., app usage surged ahead of the time spent watching live TV. Currently, the average American watches 3.7 hours of live TV per day, but now spends four hours per day on their mobile devices.

Apps aren’t just a way to pass idle hours — they’re also a big business. In 2019, mobile-first companies had a combined $544 billion valuation, 6.5x higher than those without a mobile focus. In 2020, investors poured $73 billion in capital into mobile companies — a figure that’s up 27% year-over-year.

This week we’re looking at the case of the missing Arizona app store bill, the latest on the Dispo drama and Facebook’s new audio efforts, among other things.

This Week in Apps will soon be a newsletter! Sign up here: techcrunch.com/newsletters

Top Stories

So…where did that App Store legislation go?

Arizona’s Senate was supposed to vote on a controversial bill, HB2005, that would make it the first state to regulate the Apple and Google app stores. But though the vote was listed first on the Senate’s livestream agenda on Wednesday, March 24th, the vote never came up.

Basecamp co-founder and Apple critic David Heinemeier Hansson, who submitted testimony in support of HB 2005, basically called the lobbying system corrupt.

Doesn't mean it's guaranteed that it's over in Arizona, but hot diggity damn. Seeing how the corru… I mean.. lobbying works this close and this brazenly is something else. But Apple can't buy all the legislators in all the states. Refuse to believe that.

— DHH (@dhh) March 24, 2021

It’s true that Apple and Google had hired lobbyists to combat the bill, which would have threatened the companies’ ability to continue collecting their 15% or 30% commissions by allowing app developers to use third-party payment processors for sales and in-app purchases.

Apple had its own lobbyist, Rod Diridon, working on the Arizona bill, and was said to have hired Kirk Adams, a former chief of staff to Arizona Gov. Doug Ducey, to negotiate directly with the bill’s sponsor, Rep. Regina Cobb (R).

However, others countered the narrative being laid out by Hansson, saying that the bill’s existence in the first place was the result of lobbying from Epic Games and others, and many lawmakers didn’t even know what they were voting on. A similar bill was already voted down in North Dakota and HB2005 didn’t seem to have much support either, ahead of the would-be vote.

The Coalition for App Fairness (CAF), a group backing these bills, told us it didn’t know what happened to the bill, but was trying to find out.

Pretty weird that this bill ghosted!

Then again, an App Store bill getting mysteriously rejected without sufficient explanation is …fitting. https://t.co/C7ycLqTILc

— Dieter Bohn (@backlon) March 24, 2021

Dispo loses investor support, Dobrik

Once-hot mobile photos app Dispo is becoming a case study as to why partnering with high-profile influencers and YouTuber-types without due diligence is just a bad idea. When a recent investigation exposed that a member of YouTuber David Dobrik’s “Vlog Squad” sexually assaulted her, Dispo’s early investors have been distancing themselves from the app.

Initially, lead investor Spark Capital said it would “sever all ties” with the company, TechCrunch’s Natasha Mascarenhas reported earlier this week. Dobrik also left the board and the company hours later. Two other investors, Seven Seven Six and Unshackled, said they would donate any potential profits from their Dispo investment into organizations working with survivors of sexual assault. (Cynically, one could argue, the firms don’t expect there to be much left to donate with this much of a stain on Dispo’s public image and the loss of its big-name backer in Dobrik).

Dispo had been valued at $200 million after its $20 million Series A, led by Spark Capital only weeks ago. The company released a statement saying it would continue to work on the platform.

Facebook’s Clubhouse rival looks like Clubhouse

Image Credits: Alessandro Paluzzi (opens in a new window)

New screenshots of Facebook’s unreleased audio product, still under development, show what appears to be a live audio broadcast experience that’s more of an extension of Facebook’s existing Messenger Rooms, rather than a standalone app experience. Facebook confirmed the images are examples of the company’s “exploratory audio efforts,” but cautioned that they don’t represent a live product at this time. The images show Clubhouse-like audio rooms with rounded profile icons and a listener section led by the speakers’ friends — very much like Clubhouse.

While the company said not to jump to any conclusions about what this all means in terms of a final product, it’s interesting to see how Facebook is thinking about social audio experiences and where they could fit in on its platform. In this case, it sees it as a third option in Messenger Rooms — users could start either a private video chat with friends or a private audio chat, or they could go live to the public on audio only.

Mark Zuckerberg (rather boldly) went on Clubhouse to praise Clubhouse for what it had pioneered, saying it would end up “being one of the modalities around live audio broadcast.” It seems Facebook sees Clubhouse as just another networking format to be knocked off, like TikTok’s vertical videos or Snapchat Stories — both of which Facebook later adopted for its own platforms.

Weekly News

Platforms: Apple

People noticed that recently created Shortcuts links broke this week, displaying a message “Shortcut Not Found,” instead of opening the Shortcuts app. The issue impacted everyone who has shared shortcuts. Apple said it was aware of the issue and working on a fix.

Apple rolled out its fifth developer betas for iOS 14.5, iPadOS 14.5 and other platforms, which was then shortly followed by the release of the public betas. These may be the last betas before the public launch, though Apple has gone beyond five betas in the past.

Apple responded to Australian Competition & Consumer Commission (ACCC), which is investigating the potential anti-competitive nature of the App Store, by saying that there were other options for developers to reach iOS users — like using a website. Some developers were not amused.

brb, implementing my Apple Watch keyboard as a web app.https://t.co/iDhfvrBvCX

— Kosta Eleftheriou (@keleftheriou) March 25, 2021

"[We] face competitive constraints from distribution alternatives within the iOS ecosystem (including developer websites and other outlets through which consumers may obtain third party apps and use them on their iOS devices) and outside iOS."

This smacks of disingenuousness. https://t.co/spMxnJDGKo

— Dan Masters – OhMDee.com (@OhMDee) March 25, 2021

Apple also defended its App Review process to the ACCC, saying that it reviews 73% of prospective apps within 24 hours of being submitted by a developer, and offers details as to why an app didn’t comply with its guidelines. It also argued that it offers a worldwide support line that facilitates 1,000 calls per week in all 175 countries where the App Store operates.

A tentative initial witness list in Apple’s courtroom battle with Epic Games over Apple’s alleged monopolist practices includes Apple CEO Tim Cook, Software Engineering SVP Craig Federighi and Apple Fellow Phil Schiller (who helped launch and run the App Store). Epic will be calling its CEO Tim Sweeney and VP Mark Rein. Executives from Microsoft, Facebook and Nvidia are also included.

Platforms: Google

Google announced the Android Ready SE Alliance to make sure that new phones will be ready to support digital alternatives to things like car keys, house keys, wallets (think national IDs, mobile driver’s licenses, passports) and more. This requires that phones include tamper-resistant hardware called a Secure Element (SE) and StrongBox, an implementation of the Keymaster HAL that resides in a hardware security module, which launched with the Pixel 3 in 2018.

A bunch of Android apps, including Gmail and Google Pay, began crashing this week due to an issue with Android System WebView. Google addressed the problem by issuing updates for the standalone WebView app and Google Chrome.

E-commerce

H&M was removed from major e-commerce apps and platforms in China, including Alibaba’s Taobao, JD.com and Pinduoduo, Meituan’s shop-listing app Dianping, map apps from Tencent and Baidu, among other major online platforms. The Swedish retailer had decided to stop buying cotton from Xinjiang, where over 1 million members of the Uyghur and other predominantly Muslim ethnic minorities have been confined to detention camps, which are accused of imposing forced labor. Nike, Adidas, Burberry, Uniqlo and Lacoste also criticized China for expressing concern over Xinjiang, leading dozen of celebs to cancel endorsement deals.

NBCU struck a deal with Facebook and Instagram to extend its “shoppable opportunities” to social media platforms. The e-commerce partnership will put pitches from the TV company’s clients on its social handles on Facebook and Instagram.

Fintech

Robinhood, the free trading app and recent home to the GameStop frenzy, confidentially filed for an IPO. The company confirmed the filing in a blog post after several media outlets broke the news.

Social

TikTok belatedly banned some Myanmar accounts that posted violent videos supporting the military’s violent coup, saying that it was aggressively cracking down on accounts promoting violence. The takedowns of the video — some of which threatened protesters with death or spread hate-fueled claims — didn’t start until early March, a month after the coup began.

TikTok added an Ad Library tool that allows marketers to view the top performing ad campaigns taking place across the app. The “top ads” feature can also be filtered by vertical and region, then by time (last seven or 30 days), and performance (CTR, impressions, video view rate).

Snapchat is developing its own take on TikTok Duets with the test of a Snap Remix feature. Duets are a core part of what makes TikTok feel like a social network, rather than just a platform for more passive video viewing. Remix — which shares the name with an Instagram Duets-style feature that’s soon to launch publicly — lets users repurpose others’ Snaps for use in their own through a variety of formats.

Facebook is testing an app for prisoners who are re-entering society, Bloomberg reports. The “Re-Entry App” was shared at the top of some users’ Instagram feeds this week, offering early access.

Axios reported that Trump was in talks with no-name app vendors about creating his own social networking app. One of the companies he spoke to was the largely unknown platform called FreeSpace, which claims its network is designed to “reinforce good habits and make the world a better place.” The app includes a news feed, user profiles and group messaging features.

Parler says it sent the FBI over 50 posts about the Capitol riot ahead of January 6, The NYT reports. If accurate, it raises the question of whether or not the FBI took the threats seriously. The FBI has refused to comment on Parler’s statement. Meanwhile, Parler is facing a lawsuit by former CEO John Matze who claims he was forced out by conservative donor Rebekah Mercer.

U.K. watchdog says Facebook’s acquisition of Giphy raises competition concerns. The Competition and Markets Authority launched the first phase of its investigation in January, and notes that Giphy had competed with Facebook outside the U.K. in digital ad deals.

Twitter seems to be working on an audience picker for its upcoming communities feature, reports Jane Manchun Wong. This would be accessible from within the tweet composer screen.

Twitter is working on audience picker for communities in the tweet composer pic.twitter.com/aqWQitUP0c

— Jane Manchun Wong (@wongmjane) March 26, 2021

Streaming & Entertainment

Spotify updated its mobile app with several changes to the Home hub. These include a way to rediscover recently played songs as far back as three months ago; a way for Premium users to view new and unfinished podcasts with a blue dot (new) and progress bar (unfinished); and a new section of personalized music recommendations. The company later in the week updated its desktop and web app, as well.

Triller forges licensing agreements with music publishers, Variety reports. The agreement with the National Music Publishers’ Association, which represents most American publishers, follows Universal withdrawing its entire library from the app last month, claiming Triller withheld payments. Triller claimed to have no idea why UMG would do this.

Clubhouse says its Android launch will “take a couple of months.” Before, the company had said it would be “soon” without promising any sort of time frame.

Gaming

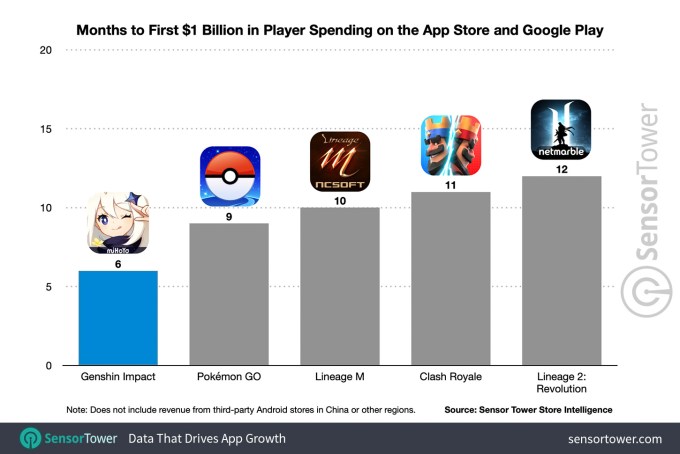

Image Credits: Sensor Tower

Genshin Impact tops $1 billion on mobile in less than six months following its September 2020 launch, says Sensor Tower. During the last 30 days, the game ranked No. 3 on the App Store and Google Play combined, behind Tencent’s PUBG Mobile and Honor of Kings.

Gaming voice and text chat service Discord, which has expanded into other forms of social networking, is said to be exploring a sale that could be worth over $10 billion. Bloomberg reported Microsoft was in talks to buy the service for more than $10 billion but no deal was imminent and Discord may choose to go public instead.

PUBG Mobile has grossed $5 billion in revenue after generating an average of $7.4 million per day in 2020, Sensor Tower reports. Like many games, PUBG Mobile’s revenue soared during the height of the pandemic with record spending of $300 million last March, during lockdowns.

Google Stadia may soon get touchscreen controls on Android, 9to5Google found by digging into the Android app’s code. The controls would allow users to use gestures like tapping, swiping and pinching.

Education

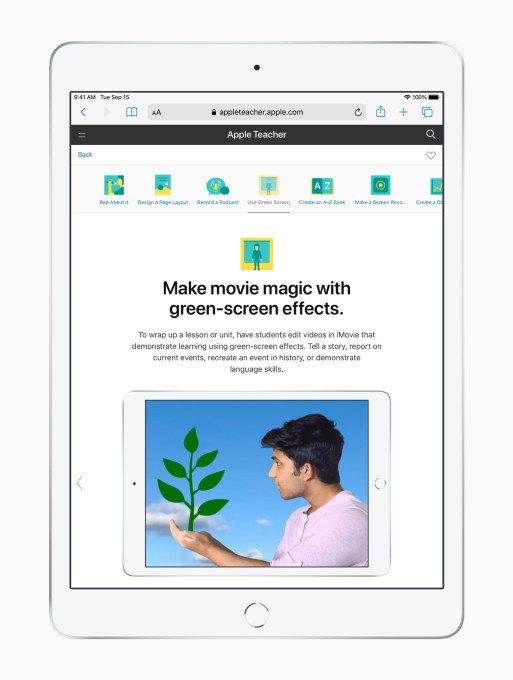

Image Credits: Apple

Apple updated its Schoolwork and Classroom apps with a few more features aimed at making it easier to share projects and support remote learning, among other things. The company also announced a Teacher Portfolio badge that would be awarded to teachers who completed a series of lessons focused on learning foundational skills on iPad and Mac.

Health & Fitness

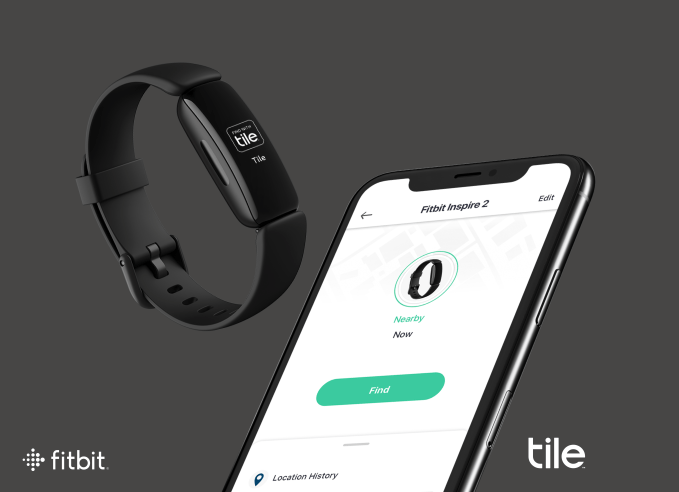

Image Credits: Tile

Tile’s lost item-tracking service arrived on wearables for the first time thanks to a new partnership with Google’s Fitbit. Through a Fitbit app update, new and existing Fitbit Inspire 2 owners will gain access to Tile’s Bluetooth-based finding network to locate their misplaced Fitbit.

Tile brings its lost item-tracking service to wearables with Google Fitbit deal for Inspire 2 owners

Health and fitness apps’ downloads increased 20% in 2020 due to the pandemic and users shifting to at-home workouts, says App Annie. In the IoT and fitness-tracking app space, Mi Fit, Strava, MyFitnessPal, Google Fit, Fitbit, BetterMe, Runtastic, Nike Training Club, Step Tracker by Leap Fitness and Samsung Health saw the most downloads last year.

Data shared by Uswitch notes that demand for sleep apps increased by 104% during the pandemic, while demand for wellness apps grew 26% since March 2020.

Productivity

Slack CEO Stewart Butterfield teased new Slack features were in beta testing: an asynchronous audio messages feature, a Clubhouse-like drop-in voice chat and Slack Stories. The exec announced the news in the PressClub show on Clubhouse, adding “good artists copy, great artists steal.”

Slack also this week launched a new universal DM system called Connect DMs, which allows any Slack user to direct message any other Slack user. The system was immediately called out for potentially enabling harassment and abuse, leading the company to pull the ability to customize the invite message.

Cortana has begun to warn its iOS and Android users that it will be shut down on March 31st. Microsoft pulled back on Cortana last year, but Cortana is still accessible on Windows. The company is also discontinuing Cortana support on the Harman Kardon Invoke speaker, as well.

Opera’s Touch iOS web browser app, now rebranded just Opera, released a major update that modernized the UI with a more flat look, a new color palette, reworked text and new icons in the bottom bar and in the “Fast Action” button, which lets you get to favorite destinations quickly. It also adds a built-in Ethereum wallet.

Privacy & Security

China defined new rules over information apps can collect, saying that users of short video, news, browser and utility apps can access basic services on these platforms without providing their personal info. The new regulation goes into effect May 1 and covers 39 app categories — including also messaging, online shopping, payments, ride hailing, short video, livestream and mobile games — where it specifies what information is necessary to use the app (e.g. if e-commerce, a user’s phone number, name, address, and payment info).

The Indian government is trying to stop WhatsApp’s controversial privacy policy update with an antitrust investigation into the policy changes, in order to determine the full extent of the app’s data-sharing practices enabled through the “involuntary consent” of WhatsApp users.

An investigation by The NYT found that Britain’s top gambling app, Sky Bet, was compiling extensive records about users. Either the app or one of the data providers it hires to collect info on users had access to users’ banking records, mortgage details, location and gambling habits.

Apple responded to ProtonVPN’s claims that Apple was standing in the way of human rights by rejecting one of its app updates. The VPN maker attempted to tie the rejection to the coup in Myanmar, saying that people in the country use its app to bypass internet crackdowns and share information about the ongoing “crimes against humanity” taking place in the country. Apple responded to the attack by noting that it had only asked the developer to reword its description so it doesn’t read like it’s encouraging users to bypass geo-restrictions or content limitations (you know, which would be illegal). And it pointed out that all Proton’s apps have remained available in Myanmar this whole time.

Facebook caught Chinese hackers using fake personas to target Uyghurs abroad. The social network caught the network of China-based hackers using fake Facebook accounts where they posed as activists, journalists and other sympathetic figures to send the targets to compromised websites. The hacking groups are aiming to gain access to the targets’ devices by getting them to install malicious apps for surveillance purposes.

A cybersecurity review of TikTok by the University of Toronto’s Citizen Lab says it’s not worse than Facebook in either data privacy or security. This, however, may be a low bar.

Scam apps have stolen more than $400 million from users across the App Store and Google, according to a study by Avast. The company reported 204 so-called “fleeceware apps” with over a billion combined downloads that trick users into free trials but then overcharge them with subscriptions that are as high as $3,432 per year.

“Apart from the financial harm… users affected by such scams will be less inclined to download apps or engage with app stores in general. Therefore, these fleeceware appls have a negative impact on legitimate developers that use the subscription model in an ethical manner.” https://t.co/4ec5AtF0s3

— David Barnard (@drbarnard) March 25, 2021

Funding and M&A

Messaging app Telegram raised over $1 billion through bond sales to multiple investors, including a combined $150 million investment by Mubadala Investment Co. and Abu Dhabi Catalyst Partners, which is part-owned by the Abu Dhabi state fund. Last week, this column noted that the app had owed its creditors around $700 million by the end of April, per The WSJ’s report.

Messaging app Telegram raised over $1 billion through bond sales to multiple investors, including a combined $150 million investment by Mubadala Investment Co. and Abu Dhabi Catalyst Partners, which is part-owned by the Abu Dhabi state fund. Last week, this column noted that the app had owed its creditors around $700 million by the end of April, per The WSJ’s report.

Fortnite and Houseparty owner Epic Games is reportedly closing on $1 billion in new funding that will value its business at $28 billion.

Twitter acqui-hired the team from API integration platform Reshuffle to work on its own developer API platform. The team of seven, including two co-founders, will immediately begin work on building tools for Twitter developers while Reshuffle’s business is wound down.

Twitter acqui-hired the team from API integration platform Reshuffle to work on its own developer API platform. The team of seven, including two co-founders, will immediately begin work on building tools for Twitter developers while Reshuffle’s business is wound down.

Link-in-bio company Linktree, whose mini websites get linked to by creators in your favorite social apps, raised $45 million to develop new social commerce tools. The company says a third of its 12 million users have signed up within the last four months — a trend partially driven by the pandemic.

South Korea’s largest travel app Yanolja is in talks with banks to go public through a dual listing in Seoul and overseas. The company is aiming for a $4 billion valuation.

South Korea’s largest travel app Yanolja is in talks with banks to go public through a dual listing in Seoul and overseas. The company is aiming for a $4 billion valuation.

ironSource, a business platform for the app economy, reached an agreement with Thoma Bravo’s blank-check firm to go public via a SPAC at a $11.1 billion valuation.

Ryu Games raised a seed round of $2.3 million for its service that helps developers add cash tournaments to their mobile games. The company is aiming to be present on a few dozen games this year.

Nigerian fintech Bankly raised $2 million for its app that digitizes cash for the unbanked, in a round led by led by Vault.

Mumbai-headquartered Indian fantasy sports app Dream11’s parent firm, Dream Sports, raised $400 million in a round led by TCV, D1 Capital Partners and Falcon Edge, valuing the business at nearly $5 billion.

Indian social network Public App raised $41 million just six months after its $35 fundraise, valuing the business at over $250 million — or more than double the valuation since the prior fundraise. The app now has over 50 million users, including over 50,000 elected officials, government authorities and citizen journalists.

U.K.-based stock trading app Freetrade raised a $69 million Series B from Left Lane Capital. The Robinhood-like app offers free trades and the ability to buy fractional shares. The company is now valued at $366 million.

Indonesian savings and investment app Pluang raised $20 million in pre-Series B funding led by Openspace Ventures. The company offers savings and investments products that allow users to make contributions starting at 50 cents (USD).

AR pioneer Blippar returns with $5 million in funding after 18 months of repositioning as a B2B company in the AR space. Blippar’s AR Studio can help brands with AR on the web and inside their apps or Blippar’s own app.

Downloads

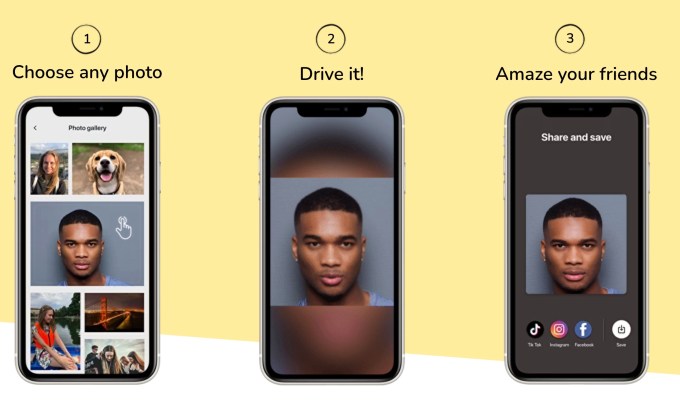

Avatarify

Image Credits: Avatarify

Avatarify is another app benefitting from the current interest in bringing photos to life. We’ve already seen apps like MyHeritage, TokkingHeads, Wombo and Piñata Farms introduce their own ideas in this space — whether it’s recalling long-lost relatives or just making a celeb lip sync to Michael Jackson. Avatarify, meanwhile, will let you record a short video which it then uses to animate any photo of your choice — even photos of art, babies or pets. The app is moving up the charts to now No. 28 on the App Store.

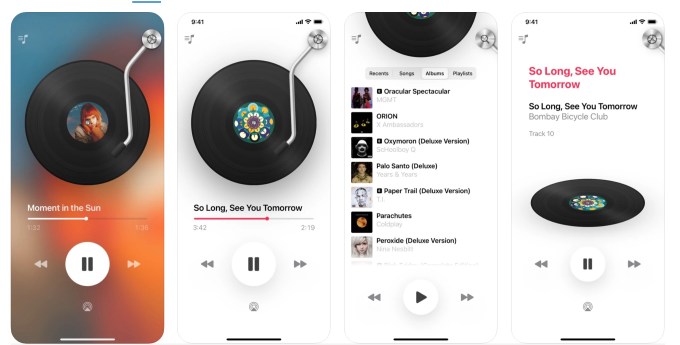

Vinyls

Image Credits: Vinyls

Vinyls, reviewed this week by iMore and recently by 9to5Mac as well, is a minimalist music player for Apple Music subscribers. The app was built by the developer behind the Twitter client Aviary, and displays a spinning vinyl record when music is playing. The app also animates a tonearm that aligns itself with the current playback time and moves in and out when playing and pausing the music. You can also “scrub” the vinyl to seek forwards and backwards. Vinyls is available on Mac, iPhone and iPad.

John Ruffolo isn’t as famous as some investors but he’s very well-known in Canadian business circles. The longtime head of Arthur Andersen’s tech, media, and telecommunications practice, he joined OMERS roughly a decade ago when a former colleague became CEO and brought him aboard the pension giant to create a venture fund.

The idea was to back the most promising Canadian companies, and Ruffolo steered the unit into investments like the social media management Hootsuite, the recently acquired storytelling platform Wattpad, and the e-commerce platform Shopify, among other deals. The last was particularly meaningful, given that OMERS owned around 6% of the company sailing into a 2015 IPO that valued it at roughly $1.3 billion at the time. Alas, owing to the pension fund’s rules, it also began steadily selling that entire stake, even as the company’s valued ticked upward. (Shopify’s market cap is currently $130 billion.)

Indeed, after helping OMERS subsequently get a growth equity unit off the ground, an antsy Ruffolo left to launch his own fund. Then came COVID, and as if the pandemic weren’t bad enough, Ruffolo further underwent a harrowing ordeal last summer. An avid cyclist, he last September set out to ride 60 miles one sunny morning on a country road, was knocked far off his bike by a Mack truck in an accident that shattered most of his bones and left him paralyzed from the waist down.

That kind of one-two punch might drive someone to the brink. Instead, six months and multiple surgeries later, Ruffolo, is undergoing training and therapy and intends to bike someday again. He is also very much back to work and just taking the wraps off his new Toronto-based firm, Maverix Private Equity, which has $500 million to invest in “traditional businesses” that already produce at least $100 million revenue and are using tech to grow but could use an outside investor for the first time to really hit the gas.

We talked with Ruffolo about the accident and his new fund this morning. You can hear that conversation here (it starts nearly seven minutes into things and it’s worth a listen). In the meantime, below are excerpts from that conversation.

TC: You’re surely tired of answering the question, but how are you doing?

JR: Well, when somebody says it’s great to be alive, it is. I actually never knew how close I was to death, to be honest, until about eight days after the accident. When I asked for my phone, just to kind of see what’s going on in the world, there was thousands of messages coming through. And I’m like, ‘What the hell?’

People were copying various articles. I picked off the first one, and it said, ‘John suffered a life threatening injury.’ And I’m kind of thinking, ‘Life threatening? Why are they saying that? And the doctors came in and said, ‘Because it was. We thought that you were going to die in the first 48 hours.’ I subsequently spoke to some of the top physicians [in Canada], and they don’t understand why I didn’t die on impact. That kind of scared me a little bit, but I’m so glad to be alive. And my recovery is far ahead of schedule. It was only within a couple of weeks where I started feeling my legs again.

TC: You were basically pulverized, yet a recent piece about your recovery in The Globe & Mail notes that within a month or so, you were back to thinking about your new fund. Do you think you might be . . . a workaholic?

JR: Some people call it stupid. [Laughs.] But for the two months, my first memory was worrying about my family and stuff [but] I have group of cycling friends — we’re called Les Domestiques — who have committed to cycling, and it’s a lot of folks who are investors, CEOs of big banks in Canada, we’re all close friends, [and] they all came to cocoon the family to make sure that nothing went wrong. So very quickly, all of these folks take over every element of the family, and the kids were fine, everybody was fine. I then had a lot of this time in hospital, and I do get antsy, and I started placing the calls to the investors who were committing to this fund pre COVID . . . I just really wanted to tell them, ‘Hey, I’m not dead. All my faculties are there. Are you still gonna be there when I get out of hospital?’

TC: Because they’re really investing in you and your track record.

JR: That’s exactly right. And I gotta tell you, it’s an interesting comparison. I’ve had American investors, and Canadian investors. American investors are very transactional. They’re very fast to come in if they see a great value proposition. Canada is not the same thing. In Canada, I’m extremely well-known as an investor and there, it’s actually relationship-driven, which is both good and bad. It’s tough in Canada because they’re more conservative, however, they stick with you in bad times. In my case, every single investor, everyone that had committed on pre- COVID, came in. Then one in particular doubled the size of the investment. They just felt bad for me, and I was like, ‘Hey, dude, I will take that sympathy card. Anytime.’

TC: You also see a real market for a Canadian-led firm to invest in Canadian companies versus taking money from American counterparts.

JR: So now this is going a little bit to the thesis, which is not a new thesis from a US perspective but is new from a Canadian perspective: the great firms in the U.S., like an Insight [Partners], like a Madison Dearborn, Bain Capital, General Atlantic, Summit — we don’t have any of those in Canada. We have great venture capital firms, and we have great buyout private equity firms. But what was really happening here is the entrepreneurs who are building great businesses are not really tech entrepreneurs; they’re just traditional industry entrepreneurs. And really, all I’m doing is planting a Canadian flag and saying, Hey, we have a Canadian firm that will lead or highly participate in these deals [to help you scale that business].

TC: You’re drawing a distinction between old-line industries and growth-stage tech companies, in other words, and you’re going after the former?

JR: [To me] a true technology company is one that actually builds the tool sets that are used by other businesses to make them bigger, faster, and stronger and I’ve been investing in those companies for 10 years with great success, but there’s a massive oversupply of capital in those spaces, particularly in the SaaS software space. It’s just not making mathematical sense on when it comes to a lot of these valuations. Meanwhile, when it comes to financial services, health care, travel, whatever, these are not tech entrepreneurs but they’re enlightened. We’re not introducing technology into the business, they already have it. But in one case, with a travel company we’re looking at closely, they want somebody who understands the travel space and also who understands technology and the impact as you scale globally.

The profile of the companies that I’m talking about have, on average, $100 million dollars of top line [growth], with flattish EBITDA, and that haven’t done any external financing with institutions. They’re growing at 20% to 50% a year, but they really want to become the next billion-dollar company.

TC: How much of these companies do you think you can own and for what size checks?

JR: We’re looking at 20% to 40% stakes in the business, so I’d say a significant minority, and we’re cutting checks of $50 to $75 million (U.S.)

TC: There aren’t a lot of massive companies in Canada, Shopify notwithstanding. How do you get the companies you plan to work with thinking on a different scale?

JR: Canadians might be a little bit more conservative, but the irony is, take a survey and [you’ll see] how many Canadians are running huge firms in the United States or in the Valley. It’s not inherent in Canadians [that they are risk averse].

Part of why I got into venture capital was I was so frustrated in the number of companies that were building products but couldn’t even generate revenues. Since then, I think we solved in Canada the zero to $10 million problem, then the $10 million to $100 million [challenge]. But starting around 2016 or so, I started to see companies that had $50 million, $60 million, $70 million in revenue starting to plateau, and the issue was global scalability.

In the U.S., so many companies can be a domestic company and be a billion-dollar company. In Canada, our market is too small; you’re forced to sell on a global scale, and many Canadian companies struggle with that. So my focus now is that last part of the piece. How do we get these companies from $100 million businesses into $1 billion-plus?

Since the pandemic began, I have been pushing the limits of my imagination to try to picture what cities will look and feel like in the coming years.

If your town looks like San Francisco, where I live, it’s a pressing question: Our once-bustling financial district is a ghost town, but even in outer neighborhoods, the number of vacant storefronts is unsettling. People are starting to emerge after sheltering in place for a year, but we are a long way from fully restoring our shared spaces.

What’s going to happen to those semi-vacant office towers, some of which are still under construction? There’s been renewed talk of converting some skyscrapers into residential housing, but there are real economic/logistic hurdles to clear before that can be broadly applied. Scores of restaurants have closed in recent months; who will take over those spaces? I spend a lot of time walking around, and it’s been a long time since I’ve noticed a “Grand Opening” sign.

Seeking answers, Managing Editor Eric Eldon interviewed 10 VCs who are active in proptech and found that most were generally “optimistic.”

Several expressed genuine uncertainty about the future of offices, but most were bullish about prospects for remote work, the rebirth of physical retail and the emergence of “third spaces” that will fill the gap between work and home.

In a companion article on TechCrunch, Eric explores these broader shifts, concluding, “you can start to see a world emerging that sounds a lot more like the fantasies of a New Urbanist than the world before the pandemic.”

Here’s who he interviewed:

- Clelia Warburg Peters, venture partner, Bain Capital Ventures

- Christopher Yip, partner and managing director, RET Ventures

- Zach Aarons, co-founder and general partner, MetaProp

- Casey Berman, general partner, Camber Creek

- Vik Chawla, partner, Fifth Wall

- Adam Demuyakor, co-founder and managing partner, Wilshire Lane Partners

- Robin Godenrath and Julian Roeoes, partners, Picus Capital

- Stonly Baptiste, founding partner, and Shaun Abrahamson, managing partner, Urban Us

- Andrew Ackerman, managing director, Dreamit

Thanks very much for reading Extra Crunch this week. Have a great weekend!

Walter Thompson

Senior Editor, TechCrunch

@yourprotagonist

Full Extra Crunch articles are only available to members.

Use discount code ECFriday to save 20% off a one- or two-year subscription.

It’s time to abandon business intelligence tools

Image Credits: Jon Feingersh Photography Inc / Getty Images

Ideally, BI transforms raw data into actionable information, but according to Charles Caldwell, VP of product management at Logi Analytics, “a gap exists between the functionalities provided by current BI and data discovery tools and what users want and need.”

Few BI tools actually integrate with existing workflows and most offer clunky user experiences, “leaving many individuals feeling like they need an advanced computer science degree to actually be able to pull insights out.”

Instead of requiring workers to abandon workflow applications to access data, embedded analytics are more efficient and easier to use, says Caldwell.

In short, “it’s time to abandon BI — at least as we currently know it.”

Pre-seed round funding is under scrutiny: Is VC pandemic posturing here to stay?

Image Credits: nadia_bormotova / Getty Images

Amid the pandemic, investors became laser-focused on sections of the pitch deck that address monetization and business viability — signs that founders need to come to the table with better-defined businesses in order to succeed.

Investors’ heightened expectations for monetization potential and a company’s positioning within its competitive landscape are unlikely to lessen in the years to come, even in a post-COVID economy.

Clubhouse UX teardown: A closer look at homepage curation, follow hooks and other features

Image Credits: Rafael Henrique/SOPA Images/LightRocket via Getty Images

Clubhouse’s hockey-stick growth is something most startups would kill for.

However, it also means that UX problems can only be addressed while in “full flight” — and that changes to the user experience will be felt at scale rather under the cover of a small, loyal and (usually) forgiving user base.

Our favorite companies from Y Combinator’s W21 Demo Day

![]()

We’re not investors, so we’re not pretending to sort the unicorns from the goats.

But TechCrunch reporters spend a lot of time talking with startups, hearing pitches and telling their stories; if you’re curious about which companies stood out from Y Combinator’s W21 Demo Day, read on.

A look at 4 IPO updates and 2 late-stage funding rounds

Image Credits: Nigel Sussman (opens in a new window)

There’s a lot going on: The venture capital market is redlining its engines while public markets remain sympathetic to growing, unprofitable companies.

Let’s round up IPO news from DigitalOcean, Kaltura, Robinhood and Zymergen, and big rounds for Lattice and goPuff.

Dear Sophie: When can I finally come to Silicon Valley?

Image Credits: Bryce Durbin/TechCrunch

Dear Sophie:

I’m a startup founder looking to expand in the U.S. I was originally looking at opening an office in Silicon Valley to be close to software engineers and investors, but then … COVID-19 :)

A lot has changed over the last year — can I still come?

— Hopeful in Hungary

Staying ahead of the curve on Google’s Core Web Vitals

Image Credits: Aleksei Naumov / Getty Images

Aside from improved SEO, small business websites optimizing for Google’s new Core Web Vitals will reap the rewards of an improved user experience for their site visitors.

While many are looking at the Core Web Vitals as a big hoop to jump through to please the search powers that be, others are seeing — and seizing — the opportunities that come along with this change.

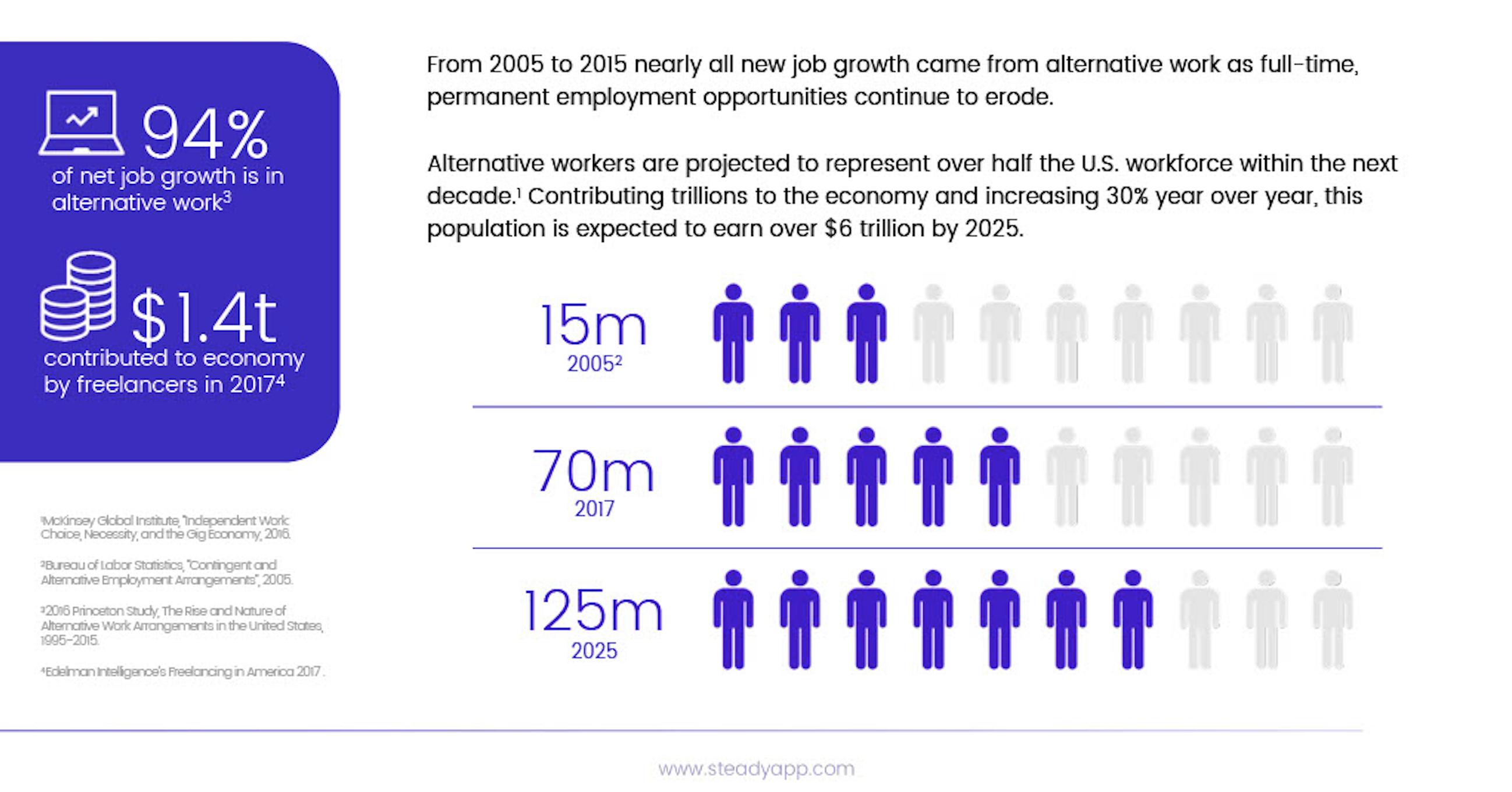

Steady’s Adam Roseman and investor Emmalyn Shaw outline what worked (and what was missing) in the Series A deck

Image Credits: Steady

When it comes to Steady — the platform that helps hourly workers manage and maximize their income and access deals on things like benefits and financial services — the strengths of the business are clear.

But it took time for founder and CEO Adam Roseman to clearly define and communicate each of them in his quest for fundraising.

Discord’s reported $10B exit; Compass and Intermedia Cloud Communications set IPO price ranges

Image Credits: Nigel Sussman (opens in a new window)

Alex Wilhelm dug into Discord’s possible $10 billion exit to Microsoft and explored IPO price ranges for real estate tech company Compass and Intermedia Cloud Communications, a unified-communications-as-a-service company.

“It’s a lot,” he noted, “but if we don’t get through it all now, we’ll fall behind and feel silly later.”

Will fading YOLO sentiment impact Robinhood, Coinbase and other trading platforms?

Image Credits: Nigel Sussman (opens in a new window)

The consumer trading frenzy could be slowing.

What would happen to Robinhood and its cohorts if the apparent cooling in consumer trading demand continues?

How VC and private equity funds can launch portfolio-acceleration platforms

Image Credits: Miguel Navarro (opens in a new window) / Getty Images (Image has been modified)

Almost every private equity and venture capital investor now advertises that they have a platform to support their portfolio companies, “however, most of us don’t have the budget of an Andreessen Horowitz to support almost every major need” for each startup they’ve bet on, says Versatile VC founder David Teten.

If you’re prioritizing a platform buildout for your firm, consider using the framework he’s outlined.

Automakers, suppliers and startups see growing market for in-vehicle AR/VR applications

Image Credits: Bryce Durbin

Despite all of the pomp and promises about the potential for AR and VR, there isn’t a clear understanding of market demand for bringing the technology to cars, trucks and passenger vans.

Estimates of the global market range from $14 billion by 2027 to as much as $673 billion by 2025, showing just how nascent the market currently is and how much opportunity is present.

Amid pandemic, Middle East adtech startups play essential role in business growth

Image Credits: phototechno / Getty Images

The Middle East is a promising region with growing digital advertising solutions despite locals’ attachment to traditional means of advertising.

In recent years, there has been a shift to the active use of social media and online shopping, meaning the Middle East embodies great potential for adtech startups.

Social+ payments: Why fintechs need social features

Image Credits: Getty Images

Social+ products are seeing mass adoption because they marry community with functionality.

This applies even to fintech companies as taboos around money fall away.

The lightning-fast Series A that was 3 years in the making

Image Credits: Mironov Konstantin / Getty Images

It took Christine Tao, founder of Sounding Board, just over three years to recognize the value of executive coaching and get her company to a Series A.

Here’s how she did it.

NFTs could bridge video games and the fashion industry

Image Credits: Amber J. Dickinson (opens in a new window)

Music companies, celebrities and fashion brands are some of the latest entities to dip a toe into the burgeoning NFT market.

In part two of a three-part series, we take a look at why NFTs are “the next chapter of digital art history.”

Where is the e-commerce app ecosystem headed in 2021?

Image Credits: Charday Penn (opens in a new window) / Getty Images

The pandemic-induced growth of e-commerce is, by now, well documented.

What is happening in the app ecosystem that supports e-commerce? Is it growing, or are we more likely to see consolidations and IPOs?

Let’s explore.

ironSource is going public via a SPAC and its numbers are pretty good

Image Credits: Nigel Sussman (opens in a new window)

You’ll want to pay attention to this one: Israel’s ironSource, an app-monetization startup, is going public via a SPAC.

It’s the second SPAC-led debut from an Israeli company in recent weeks worth more than $10 billion, and ironSource is actually a pretty darn interesting company from a financial perspective.

Coursera set to roughly double its private valuation in impending IPO

Image Credits: Bryce Durbin / TechCrunch

The market views Coursera’s edtech business warmly ahead of its impending public offering.

Coursera is being valued as a software company, likely a breathe-easy moment for still-private edtech companies, since the debut could be an industry bellwether.

There’s certainly no shortage of SaaS performance metrics leaders focus on. While all SaaS companies do, and must, home in on acquisition metrics, there’s also massive revenue potential within your current customer base.

I think NRR (net revenue retention) is without question the most underrated metric out there. NRR is simply total revenue minus any revenue churn plus any revenue expansion from upgrades, cross-sells or upsells. The greater the NRR, the quicker companies can scale. Simply put: the power of compound math!

One of the biggest and most impactful changes we made was to move new business, retention and account management all under our chief revenue officer.

Over the course of two quarters, Terminus grew its NRR by more than 30 points, opening up incredible new levels of growth opportunities.

To boost our NRR for the better, I focused on three core pillars within our organization.

People

We took a holistic look at the organization and our org structure. One of the biggest and most impactful changes we made was to move new business, retention and account management all under our chief revenue officer. At the end of the day, it just makes a ton of sense to have acquisition and retention living under the same roof — why bother acquiring new customers if you can’t retain them?

We also rolled out a surround-sound team (around three or four people per customer) who onboard and help customers with their account from day one. In total, we have about a quarter of our company dedicated to this 24/7 support and hands-on guidance to ensure we’re enabling customers immediately.

Process

“Headless commerce” is a phrase that gets thrown around lot (I’ve typed it several times today already), but Vue Storefront CEO Patrick Friday has an especially vivid way of using the concept to illustrate his startup’s place in the broader ecosystem.

“Vue Storefront is the bodiless front-end,” Friday said. “We are the walking head.”

In other words, while most headless commerce companies are focused on creating back-end infrastructure, Vue powers the front-end, namely the progressive web applications with which consumers actually interact. The company describes itself as “the lightning-fast frontend platform for headless commerce.”

Friday said that he and CTO Filip Rakowski created the Vue Storefront technology as an open-source project while working at e-commerce agency Divante, before eventually spinning it out into a separate startup last year. The company was also part of the most recent class at accelerator Y Combinator, and it recently raised $1.5 million in seed funding led by SMOK Ventures and Movens VC.

“We had to set up a new entity in the middle of COVID, we had to raise in the middle of COVID and we had to convince the agency get rid of the product in the middle of COVID,” Friday said. He even recalled signing papers with an investor one morning in early December and doing an interview with Y Combinator that evening.

Image Credits: Vue Storefront

As they’ve built a business around the core open-source technology, Friday and his team have realized that Vue has more to offer than just building web apps, because it connects e-commerce platforms like Magento and Shopify with headless content management systems like Contentstack and Contentful, payments systems like PayPal and Stripe and other third-party services.

In fact, Friday said customers have been telling them, “You are like the glue. Headless was so complex to me, and then I got this Vue Storefront thing to come in on top everything else and be the glue connecting things.”

The platform has been used to create more than 300 stores worldwide. Friday said adoption has accelerated as the pandemic and resulting growth in e-commerce have driven businesses to realize they’re using “this legacy platform, using outdated frameworks and technologies from a good four or five years ago.”

Rakowski added, “We also see that many customers actually come to us deciding that Vue Storefront can be the first step of migration to another platform. We can quickly migrate the front-end and write back-end agnostic code.”

Because it had just raised funding, the Vue Storefront team did not participant in the recent YC Demo Day, and will be presenting at the next Demo Day instead. In the meantime, it will be holding its own virtual Vue Storefront Summit on April 20.