& meet dozens of singles today!

User blogs

Meesho said on Monday it has raised $300 million in a new financing round led by SoftBank Vision Fund 2 as the Indian social commerce startup works to become the “single ecosystem that will enable all small businesses to succeed online.”

The new round — a Series E — gives the five-year-old startup a valuation of $2.1 billion, up from about $600 million in 2019 Series D investment. The Indian startup, which has raised about $490 million to date, said existing investors Facebook, Prosus Ventures, Shunwei Capital, Venture Highway, and Knollwood Investment also participated in the new round.

Bangalore-based Meesho operates an eponymous online marketplace that connects sellers with customers on social media platforms such as WhatsApp, Facebook and Instagram. The startup claims to have a network of more than 13 million entrepreneurs, a majority of whom are women, from hundreds of Indians towns who largely deal with apparel, home appliances and electronics items.

Meesho said it will deploy the fresh capital to help 100 million individuals and small businesses in the country to sell online. “In the last one year, we have seen tremendous growth across small businesses and entrepreneurs seeking to move their businesses online,” said Vidit Aatrey, co-founder and chief executive of Meesho, in a statement.

“We have been closely tracking Meesho for the last 18 months and have been impressed by their growth, daily engagement metrics, focus on unit economics and ability to create a strong team. We believe Meesho provides an efficient platform for SME suppliers and social resellers to onboard the e-commerce revolution in India and help them provide personalized experience to consumers,” said Sumer Juneja, partner at SoftBank Investment Advisers, in a statement.

In a recent report, UBS analysts identified social commerce and business-to-business marketplaces as potential sources of competition to e-commerce firms such as Amazon and Flipkart in India.

This is a developing story. More to follow…

Welcome back to The TechCrunch Exchange, a weekly startups-and-markets newsletter. It’s broadly based on the daily column that appears on Extra Crunch, but free, and made for your weekend reading. Want it in your inbox every Saturday? Sign up here.

Happy Saturday, everyone. I do hope that you are in good spirits and in good health. I am learning to nap, something that has become a requirement in my life after I realized that the news cycle is never going to slow down. And because my partner and I adopted a third dog who likes to get up early, please join me in making napping cool for adults, so that we can all rest up for Vaccine Summer. It’s nearly here.

On work topics, I have a few things for you today, all concerning data points that matter: Q1 2021 M&A data, March VC results from Africa, and some surprising (to me, at least) podcast numbers.

On the first, Dan Primack shared a few early first-quarter data points via Refinitiv that I wanted to pass along. Per the financial data firm, global M&A activity hit $1.3 trillion in Q1 2021, up 93% from Q1 2020. U.S. M&A activity reached an all-time high in the first quarter, as well. Why do we care? Because the data helps underscore just how hot the last three months have been.

I’m expecting venture capital data itself for the quarter to be similarly impressive. But as everyone is noting this week, there are some cracks appearing in the IPO market, as the second quarter begins that could make Q2 2021 a very different beast. Not that the venture capital world will slow, especially given that Tiger just reloaded to the tune of $6.7 billion.

On the venture capital topic, African-focused data firm Briter Bridges reports that “March alone saw over $280 million being deployed into tech companies operating across Africa,” driven in part by “Flutterwave’s whopping $170 million round at a $1 billion valuation.”

The data point matters as it marks the most active March that the African continent has seen in venture capital terms since at least 2017 — and I would guess ever. African startups tend to raise more capital in the second half of the year, so the March result is not an all-time record for a single month. But it’s bullish all the same, and helps feed our general sentiment that the first quarter’s venture capital results could be big.

And finally, Index Ventures’ Rex Woodbury tweeted some Edison data, namely that “80 million Americans (28% of the U.S. 12+ population) are weekly podcast listeners, +17% year-over-year.” The venture capitalist went on to add that “62% of the U.S. 12+ population (around 176 million people) are weekly online audio listeners.”

As we discussed on Equity this week, the non-music, streaming audio market is being bet on by a host of players in light of Clubhouse’s success as a breakout consumer social company in recent months. Undergirding the bets by Discord and Spotify and others are those data points. People love to listen to other humans talk. Far more than I would have imagined, as a music-first person.

How nice it is to be back in a time when consumer investing is neat. B2B is great but not everything can be enterprise SaaS. (Notably, however, it does appear that Clubhouse is struggling to hold onto its own hype.)

Look I can’t keep up with all the damn venture capital rounds

TechCrunch Early Stage was this week, which went rather well. But having an event to help put on did mean that I covered fewer rounds this week than I would have liked. So, here are two that I would have typed up if I had had the spare hours:

- Striim’s $50 million Series C. Goldman led the transaction. Striim, pronounced stream I believe, is a software startup that helps other companies move data around their cloud and on-prem setups in real time. Given how active the data market is today, I presume that the TAM for Striim is deep? Quickly flowing? You can supply a better stream-centered word at your leisure.

- Kudo’s $21 million Series A. I covered Kudo last July when it raised $6 million. The company provides video-chat and conferencing services with support for real-time translation. It had a good COVID-era, as you can imagine. Felicis led the A after taking part in the seed round. I’ll see if I can extract some fresh growth metrics from the company next week. One to watch.

And two more rounds that you also might have missed that you should not. Holler raised $36 million in a Series B. Per our own Anthony Ha, “[y]ou may not know what conversational media is, but there’s a decent chance you’ve used Holler’s technology. For example, if you’ve added a sticker or a GIF to your Venmo payments, Holler actually manages the app’s search and suggestion experience around that media.”

I feel old.

And in case you are not paying enough attention to Latin American tech, this $150 million Uruguayan round should help set you straight.

Various and sundry

Finally this week, some good news. If you’ve read The Exchange for any length of time, you’ve been forced to read me prattling on about the Bessemer cloud index, a basket of public software companies that I treat with oracular respect. Now there’s a new index on the market.

Meet the Lux Health + Tech Index. Per Lux Capital, it’s an “index of 57 publicly traded companies that together best represent the rapidly emerging Health + Tech investment theme.” Sure, this is branded to the extent that, akin to the Bessemer collection, it is tied to a particular focus of the backing venture capital firm. But what the new Lux index will do, as with the Bessemer collection, is track how a particular venture firm is itself tracking the public comps for their portfolio.

That’s a useful thing to have. More of this, please.

Amazon kicked off the holiday weekend by backtracking slightly on a social media offensive that unfolded in the waning days of a historic unionization vote. The earlier comments reportedly arrived as Jeff Bezos was pushing for a more aggressive strategy.

Along with taking on Senators Bernie Sanders and Elizabeth Warren, the Amazon News Twitter account went toe to toe with Congressman, Mark Pocan. The Wisconsin Democrat cited oft-reported stories of Amazon workers urinating in bottles in reaction to comments from Consumer CEO, Dave Clark.

“You don’t really believe the peeing in bottles thing, do you?” the account asked. “If that were true, nobody would work for us. The truth is that we have over a million incredible employees around the world who are proud of what they do, and have great wages and health care from day one.”

1/2 You don’t really believe the peeing in bottles thing, do you? If that were true, nobody would work for us. The truth is that we have over a million incredible employees around the world who are proud of what they do, and have great wages and health care from day one.

— Amazon News (@amazonnews) March 25, 2021

The Congressman’s initial response was pithy and to the point: “[Y]es, I do believe your workers. You don’t?”

Subsequent reports have served to cement those stories. One called the urination issue “widespread” among Amazon drivers, adding that defecation had also, reportedly, become a problem. Last night, the company offered a mea culpa of sorts, saying it “owe[s] an apology to Representative Pocan.”

Things break down a bit from there. Amazon’s apology acknowledges that workers peeing in bottles is a thing, but appears to imply that it’s limited to drivers and not the fulfillment center staff at the center of this large scale unionization effort. From there, the company adds that drivers peeing in bottles is an “industry-wide issue and is not specific to Amazon.”

The company helpfully includes a list of links and tweets that are, at very least, an indictment of the gig economy and the treatment of blue collar workers, generally. Essentially, Amazon is admitting to being a part of the problem, while working to spread the blame across an admittedly faulty system.

Reports of workers urinating in bottles also go beyond drivers, including stories of warehouse employees resorting to the act in order to meet stringent quotas.

“A typical Amazon fulfillment center has dozens of restrooms, and employees are able to step away from their work station at any time,” company writes in the post attributed to anonymous Amazon Staff. “If any employee in a fulfillment center has a different experience, we encourage them to speak to their manager and we’ll work to fix it.”

Union vote counting for the company’s Bessemer, Alabama warehouse began last week. Results could have a wide-ranging impact on both Amazon and the industry at large.

NASA’s SBIR program regularly doles out cash to promising small businesses and research programs, and the lists of awardees is always interesting to sift through. Here are a dozen companies and proposals from this batch that are especially compelling or suggest new directions for missions and industry in space.

Sadly these brief descriptions are often all that is available. These things are often so early stage that there’s nothing to show but some equations and a drawing on the back of a napkin — but NASA knows promising work when it sees it. (You can learn more about how to apply for SBIR grants here.)

Martian Sky Technologies wins the backronym award with Decluttering of Earth Orbit to Repurpose for Bespoke Innovative Technologies, or DEORBIT, an effort to create an autonomous clutter-removal system for low Earth orbit. It is intended to monitor a given volume and remove any intruding items, clearing the area for construction or occupation by another craft.

Image Credits: Getty Images

Ultrasonic additive manufacturing

There are lots of proposals for various forms of 3D printing, welding, and other things important to the emerging field of “On-orbit servicing, assembly, and manufacturing” or OSAM. One I found interesting uses ultrasonics, which is weird to me because clearly, in space, there’s no atmosphere for ultrasonic to work in (I’m going to guess they thought of that). But this kind of counterintuitive approach could lead to a truly new approach.

Robots watch each other’s backs

Doing OSAM work will likely involve coordinating multiple robotic platforms, something that’s hard enough on Earth. TRAClabs is looking into a way to “enhance perceptual feedback and decrease the cognitive load on operators” by autonomously moving robots not in use to positions where they can provide useful viewpoints of the others. It’s a simple idea and fits with the way humans tend to work — if you’re not the person doing the actual task, you automatically move out of the way and to a good position to see what’s happening.

3D printed Hall effect thrusters

Hall effect thrusters are a highly efficient form of electric propulsion that could be very useful in certain types of in-space maneuvering. But they’re not particularly powerful, and it seems that to build larger ones existing manufacturing techniques will not suffice. Elementum 3D aims to accomplish it by developing a new additive manufacturing technique and cobalt-iron feedstock that should let them make these things as big as they want.

Venus is a fascinating place, but its surface is extremely hostile to machines the way they’re built here on Earth. Even hardened Mars rovers like Perseverance would succumb in minutes, seconds even in the 800F heat. And among the many ways they would fail is that the batteries they use would overheat and possibly explode. TalosTech and the University of Delaware are looking into an unusual type of battery that would operate at high temperatures by using atmospheric CO2 as a reactant.

When you’re going to space, every gram and cubic centimeter counts, and once you’re out there, every milliwatt does as well. That’s why there’s always a push to switch legacy systems to low size, weight, and power (low-SWaP) alternatives. Intellisense is taking on part of the radio stack, using neuromorphic (i.e. brainlike – but not in a sci-fi way) computing to simplify and shrink the part that sorts and directs incoming signals. Every gram saved is one more spacecraft designers can put to work elsewhere, and they may get some performance gains as well.

Astrobotic is becoming a common name to see in NASA’s next few years of interplanetary missions, and its research division is looking at ways to make both spacecraft and surface vehicles like rovers smarter and safer using lidar. One proposal is a lidar system narrowly focused on imaging single small objects in a sparse scene (e.g. scanning one satellite from another against the vastness of space) for the purposes of assessment and repair. The second involves a deep learning technique applied to both lidar and traditional imagery to identify obstacles on a planet’s surface. The team for that one is currently also working on the VIPER water-hunting rover aiming for a 2023 lunar landing.

Bloomfield does automated monitoring of agriculture, but growing plants in orbit or on the surface or Mars is a little different than here on Earth. But it’s hoping to expand to Controlled Environment Agriculture, which is to say the little experimental farms we’ve used to see how plants grow under weird conditions like microgravity. They plan to use multi-spectral imaging and deep learning analysis thereof to monitor the state of plants constantly so astronauts don’t have to write “leaf 25 got bigger” every day in a notebook.

The Artemis program is all about going to the Moon “to stay,” but we haven’t quite figured out that last part. Researchers are looking into how to refuel and launch rockets from the lunar surface without bringing everything involved with them, and Exploration Architecture aims to take on a small piece of that, building a lunar launchpad literally brick by brick. It proposes an integrated system that takes lunar dust or regolith, melts it down, then bakes it into bricks to be placed wherever needed. It’s either that or bring Earth bricks, and I can tell you that’s not a good option.

Several other companies and research agencies proposed regolith-related construction and handling as well. It was one of a handful of themes, some of which are a little too in the weeds to go into.

Another theme was technologies for exploring ice worlds like Europa. Sort of like the opposite of Venus, an ice planet will be lethal to “ordinary” rovers in many ways and the conditions necessitate different approaches for power, sensing, and traversal.

NASA isn’t immune to the new trend of swarms, be they satellite or aircraft. Managing these swarms takes a lot of doing, and if they’re to act as a single distributed machine (which is the general idea) they need a robust computing architecture behind them. Numerous companies are looking into ways to accomplish this.

You can see the rest of NASA’s latest SBIR grants, and the technology transfer program selections too, at the dedicated site here. And if you’re curious how to get some of that federal cash yourself, read on below.

Welcome back to This Week in Apps, the weekly TechCrunch series that recaps the latest in mobile OS news, mobile applications and the overall app economy. The app industry is as hot as ever, with a record 218 billion downloads and $143 billion in global consumer spend in 2020.

Consumers last year also spent 3.5 trillion minutes using apps on Android devices alone. And in the U.S., app usage surged ahead of the time spent watching live TV. Currently, the average American watches 3.7 hours of live TV per day, but now spends four hours per day on their mobile devices.

Apps aren’t just a way to pass idle hours — they’re also a big business. In 2019, mobile-first companies had a combined $544 billion valuation, 6.5x higher than those without a mobile focus. In 2020, investors poured $73 billion in capital into mobile companies — a figure that’s up 27% year-over-year.

This Week in Apps will soon be a newsletter! Sign up here: techcrunch.com/newsletters

This week we’re looking into app store trends, Apple’s upcoming WWDC, new App Store rejections and what they mean for ATT (App Tracking Transparency), and whatever happened to that Arizona App Store bill, among other stories.

Top Stories

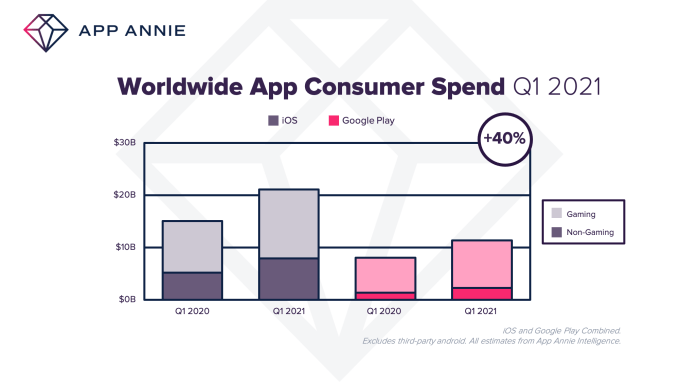

Apps just had the biggest quarter on record

Big news for the app economy this week, as App Annie reported that consumer spending on mobile apps broke a new record. According to new data, worldwide consumers in Q1 2021 spent $32 billion on apps across both iOS and Google Play, up 40% year-over-year from Q1 2020. It’s the largest-ever quarter on record, with mobile consumers spending roughly $9 billion more in Q1 2021 compared with Q1 2020, in part due to the pandemic’s continued impacts.

Image Credits: App Annie

Although iOS saw larger consumer spend than Android in the quarter — $21 billion versus $11 billion, respectively — both stores grew by the same percentage, 40%. Gaming drove a majority of the quarter’s consumer spending, as usual, accounting for $22 billion of the spend — $13 billion on iOS (up 30% year-over-year) and $9 billion on Android (up 35%).

Apple begins rejecting apps with fingerprinting tech

With the launch of iOS 14.5 looming, reports circulated this week that Apple has begun rejecting apps that use third-party SDKs that track users via a method called device fingerprinting. The Adjust SDK was one that didn’t yet comply with Apple’s new App Tracking Transparency guidelines, causing apps that included the SDK to be rejected. That could have been a large number of possible rejections, as Adjust’s website claims it’s trusted by more than 50,000 apps. But Adjust soon updated its SDK (open-sourced and here on GitHub), to hopefully re-enable app updates for its customers.

Per a number of developers, Apple has begun rejecting app updates that include the Adjust SDK related to its collection of data used for device fingerprinting.

— Eric Seufert (@eric_seufert) April 1, 2021

The App Tracking Transparency (ATT) changes have thrown a whole industry into disarray as companies scramble to comply and diversify their revenues. Snap, however, was found to be looking into alternative ways to bypass ATT by gathering data like IP addresses from companies that analyze ad campaigns to see if it could then cross-reference that data with its own, in order to continue tracking its users. Snap told the Financial Times it had tested the technique, called probabilistic matching, to test the impact of Apple’s policies, but claimed it intended to discontinue the program after Apple introduced its changes. (Sure Jan!) The company says it believes that tracking individual users will no longer be allowed going forward, but gathering data on “cohorts” would be. On Thursday, Apple sent letters to developers warning them to remove code that supported probabilistic matching, just in case.

WWDC 2021 announced

WWDC will again be virtual, Apple announced this week. The online event will take place June 7 to 11, as it did last year, allowing developers worldwide to tune in to watch prerecorded keynotes and sessions, and virtually network and learn from Apple engineers and employees. Though April 18, students can submit their Swift playground to this year’s Swift Student Challenge to win exclusive outerwear and Apple pins.

is that the picture you got? this is what i got pic.twitter.com/tdpvfktZiH

— Jonathan Khoo (@jonk) March 30, 2021

Everyone has already begun to read wayyyy too much into the imagery Apple published, which shows Memoji characters wearing glasses looking at a Mac screen. Is Apple teasing AR glasses?, some wondered. That doesn’t seem likely, though. The glasses are just a way to reflect the computer screen in a picture whose message largely conveys, yep, it’s another virtual event this year.

The Arizona App Store bill is dead

The bill was the work of the Coalition for App Fairness, led by Epic Games, Spotify, Tile and other developers who want alternatives to paying app store commissions and alternative distribution channels. Last week, it had been unclear why the AZ Senate skipped the vote on the bill, which had been passed by the AZ House. But according to the bill’s (HB2005) backer, Rep. Regina Cobb, speaking to The Verge, the decision was due to heavy lobbying by Apple and Google, which caused Senate members who had agreed to a vote to waiver. When the votes weren’t there, the Senate decided to skip bringing it up altogether.

The bill was the work of the Coalition for App Fairness, led by Epic Games, Spotify, Tile and other developers who want alternatives to paying app store commissions and alternative distribution channels. Last week, it had been unclear why the AZ Senate skipped the vote on the bill, which had been passed by the AZ House. But according to the bill’s (HB2005) backer, Rep. Regina Cobb, speaking to The Verge, the decision was due to heavy lobbying by Apple and Google, which caused Senate members who had agreed to a vote to waiver. When the votes weren’t there, the Senate decided to skip bringing it up altogether.

Cobb, in an email to TechCrunch, confirmed the same. “We have been working with members on the committee and had the votes a few days prior,” she said. “Just before the committee was set to proceed, the Chairman notified the lobbyist for App Fairness that the votes were not there so he did not want to waste committee time on the issue.”

Weekly News

Platforms: Apple

Apple released the iOS 14.5 beta 6 to developers, which includes one major change: the release of new Siri voices. With iOS 14.5, Siri will no longer default to a female voice, but will rather allow customers to choose from a set of voices, presented in random order. Prior to the release, there had been some expectation that beta 5 would be the last before the public release, but that turned out to not be the case. However, now that beta 6 has arrived, the Release Candidate could follow as soon as next week.

Apple released the iOS 14.5 beta 6 to developers, which includes one major change: the release of new Siri voices. With iOS 14.5, Siri will no longer default to a female voice, but will rather allow customers to choose from a set of voices, presented in random order. Prior to the release, there had been some expectation that beta 5 would be the last before the public release, but that turned out to not be the case. However, now that beta 6 has arrived, the Release Candidate could follow as soon as next week.

I’ll stick with Siri Voice 4. I don’t know if I ever want to change. pic.twitter.com/znmfMAvWQq

— Wesley Hilliard (@HilliTech) March 31, 2021

Ahead of WWDC 2021, Apple updated its Apple Developer app. The app offers an updated look-and-feel, which now supports a sidebar navigation on iPad, full-screen video on larger Mac displays and a new way to discover content to watch and read in an updated Search section. As with last year’s WWDC, attendees will be able to connect with and tune into announcements, sessions and 1:1 labs via the Developer app.

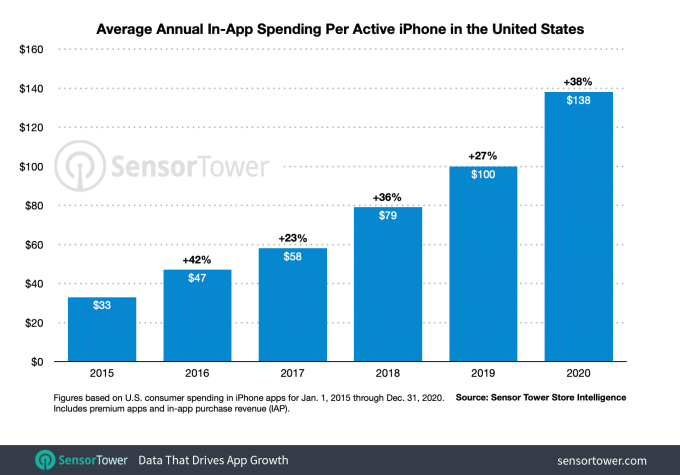

U.S. users spent an average of $138 on iPhone apps in 2020, and the number is expected to grow to $180 in 2021, reported Sensor Tower. Throughout 2020, consumers turned to iPhone apps for work, school, entertainment, shopping and more, driving per-user spending to a new record and the greatest annual growth since 2016. Per-device spending on mobile games was a large part of that figure, growing 43% year over year from $53.80 in 2019 to $76.80 in 2020. That’s more than 20 points higher than the 22% growth seen between 2018 and 2019, when in-game spending grew from $44 to $53.80.

Image Credits: Sensor Tower

Platforms: Google

Google will begin to limit Android 11+ apps from being able to see what other apps the user has installed on their devices starting on May 5. The company now considers this “sensitive information,” though for years had allowed the practice. That made it easy for data-gathering apps that catalog to operate. Now, Google will only allow a few exceptions — apps that will be able to use the permission include antivirus, file managers and browsers. Expect to see data-gathering firms quietly release those sorts of apps in the near future.

Google will begin to limit Android 11+ apps from being able to see what other apps the user has installed on their devices starting on May 5. The company now considers this “sensitive information,” though for years had allowed the practice. That made it easy for data-gathering apps that catalog to operate. Now, Google will only allow a few exceptions — apps that will be able to use the permission include antivirus, file managers and browsers. Expect to see data-gathering firms quietly release those sorts of apps in the near future.

Augmented Reality

Google expanded the AR virtual art galleries in its Arts & Culture app to include three new Pocket Galleries from the Jean Pigozzi Collection and J. Paul Getty Museum.

Health & Fitness

A feature in The Cut this week raises questions about the viability and effectiveness of therapy apps like Talkspace, BetterHelp and AbleTo, some which use dating app-like models for matching clients to therapists as well as similar business models, where you can upgrade to live video and more features. The article questions whether the apps are able to deliver on their promises and notes how some have already faced questions over their use of data, sponsorship deals, treatment of workers and healthcare rule violations.

The global airline industry body IATA said it will launch a digital travel pass for COVID-19 test results and vaccine certificates on iOS by mid-April. The travel pass, meant to help speed up check-ins, is being tested already by U.K.-based Virgin Atlantic, which is using the IATA app on its London to Barbados flight on April 16.

Apple Maps adds COVID-19 travel guidance for over 300 airports worldwide in its recent update. The app will now show COVID-19 health measure information for airports when searched via the app, either through a link to the airport’s own COVID-19 advisory page, or directly on the in-app location card itself.

Social Networks

Image Credits: Facebook

Facebook teamed up with the U.S. Department of Health and Human Services (HHS) and Centers for Disease Control and Prevention (CDC) to launch a set of profile frames that will help to encourage vaccinations against COVID-19. The frames, offered in either English or Spanish, will say “Let’s Get Vaccinated” or “I Got My COVID-19 Vaccine.” Research shows that social norms can impact people’s behavior when it comes to their health, so the hope is that, as more adopt the frames, those hesitant about the vaccine will be encouraged to get one. Facebook will also begin showing users how many of their family and friends have been vaccinated, based on the frame usage.

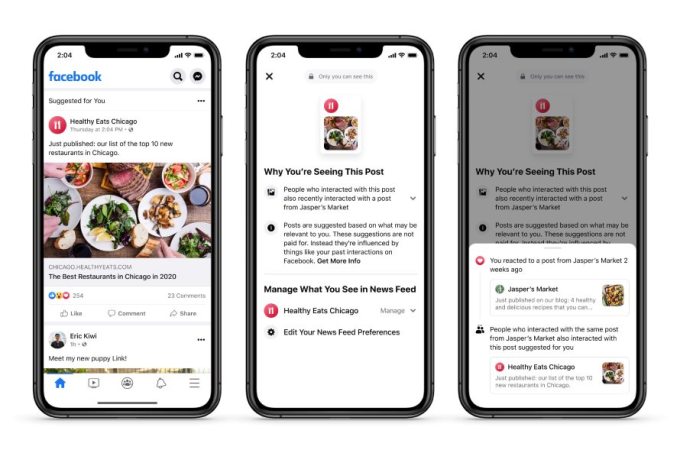

Facebook this week introduced new tools that allow users to more easily switch to the “Most Recent” view or “Favorites” view of their News Feed, as well as tools to limit comments on posts and other changes. The launch came at the same time as the company argued in a long-winded post how its personalization algorithms are not at fault for the world’s ills and the rising spread of misinformation and dangerous health content. Rather, it blames the users who seek out this content and then engage with it. The company is pushing regulators to give it guidelines on misinformation, knowing that it will have an easier time with increased regulations than any new social media upstarts.

Image Credits: Facebook

Instagram launched Remix on Reels, a TikTok Duets-like feature that allows users to record a video alongside someone else’s content in order to react, collaborate and more. Snapchat is developing its own Duets feature with the same name of Remix, too.

Snap is planning to expand further into hardware, The Information reported, with a new, more advanced version of its Spectacles smart glasses that include AR effects. It’s also reviving an older effort to build its own drone.

Instagram appears to be developing a new way to block the trolls. Reverse engineer Alessandro Paluzzi found in the app’s code a reference to a new option, “Hide More Comments,” which will automatically hide comments with frequently reported words.

#Instagram is working on a new option to filter comments: Hide more comments

When active, comments containing frequently reported words will be automatically hidden.

— Alessandro Paluzzi (@alex193a) March 31, 2021

Instagram announced it’s expanding its IGTV ads internationally for the first time, initially to markets including the U.K. and Australia.

Facebook extended the deadline for iOS apps using its Facebook Audience Network monetization platform to migrate their apps to bidding only — a response to Apple’s iOS 14 changes. The previous deadline was March 31, which has now been pushed to May 31. Android apps have until September 30.

Streaming & Entertainment

Business-focused social network LinkedIn confirmed it’s building a Clubhouse rival that will offer a speaker stage, as well as tools to join and leave the room, react to comments, request to speak and more. The company sees the feature as an extension of its existing offerings for creators, which also includes things like LinkedIn Live, Stories and newsletters. It says that it believes its offering will be able to differentiate from others because its network will be connected with people’s professional identity, not just a social profile.

Image Credits: LinkedIn

Spotify significantly expanded its personalized playlist lineup with the launch of three new categories of playlists, called “Spotify Mixes.” Inspired by Daily Mixes, these new options offer easy-to-understand titles that include artist mixes (e.g. Drake Mix), genre mixes (e.g. Pop Mix) and decade mixes (e.g. 2010s Mix).

Audioburst launches a platform that will allow developers to integrate podcast feeds into mobile apps. The platform supports both partial or complete podcasts and radio shows and other streaming audio.

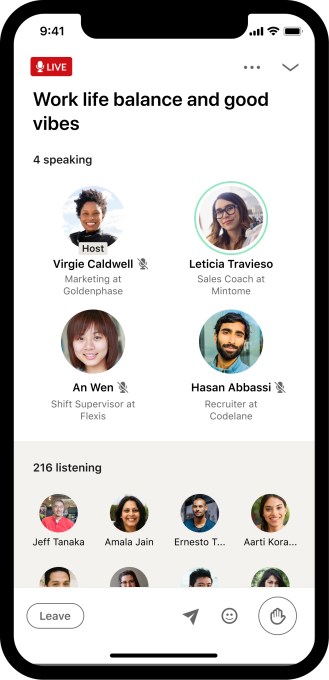

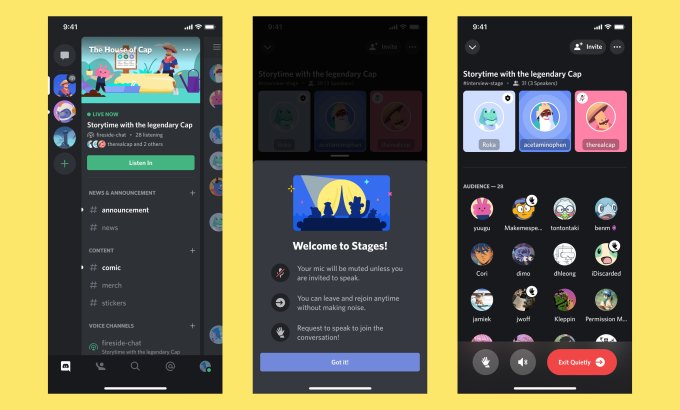

Discord became yet another tech company to offer its own Clubhouse-like feature with the launch of Stage Channels. The feature allows certain people to broadcast to a group of listeners, who can raise their hand to ask questions, while moderators can bring people onstage, remove them or put them on mute. Stage Channels are available on desktop, web and in Discord’s mobile apps.

Image Credits: Discord/TechCrunch

Gaming

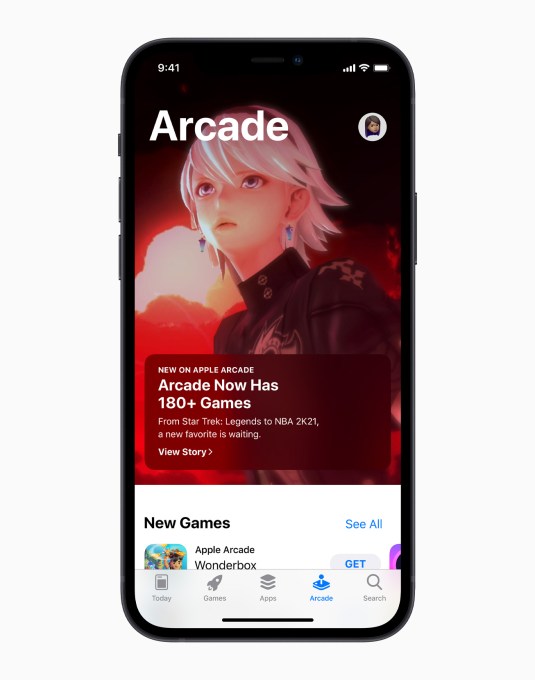

Apple’s subscription-based gaming service, Apple Arcade, was significantly expanded this week with the addition of more than 30 new titles, including new exclusives like NBA 2K21, Star Trek: Legends and a new version of The Oregon Trail from Gameloft. But it also notably adopted a new strategy as well, with the addition of older titles in two new categories called “Timeless Classics” and “App Store Greats.”

Image Credits: Apple

The former will include well-loved games like chess, backgammon, sudoku, crosswords, solitaire and others, while the App Store Greats will bring award-winning titles to Arcade like Threes!, Mini Metro, Fruit Ninja Classic, Monument Valley and Chameleon Run — all of which will be free and unlocked. With the additions, Apple Arcade has now grown to more than 180 total games for $4.99/mo (or included with an Apple One subscription.)

Finnish mobile gaming giant Supercell, developers of Clash of Clans and Clash Royale, announced it’s making three new Clash titles: a turn-based tactical game, Clash Quest; a virtual board game, Clash Mini; and a co-op action roleplaying game, Clash Heroes. The games are in early stages of development and will be killed if they don’t meet Supercell’s high standards.

Fintech

Following the meme stock frenzy, free stock trading app Robinhood will remove its controversial digital confetti feature, which critics said was a gamification technique — and not something that should be associated with financial investing.

WhatsApp Pay, the messaging app’s P2P payments feature, is now authorized in Brazil. The feature was first announced to roll out in Brazil last year, but had to be delayed after the country’s central bank said it could damage existing payments systems. It also said WhatsApp had failed to obtain proper licensing. On Tuesday, the bank said the service could go forward — now that it’s launched its own payments system called Pix, which has been widely adopted.

Bakkt released a digital wallet app for trading fiat currency for crypto, but also supports other digital assets not on the blockchain like frequent flier miles, loyalty points, gift cards and in-game assets.

Productivity

Microsoft’s Cortana mobile app for iOS and Android officially shut down on Wednesday, March 31. The AI-based personal assistant was Microsoft’s answer to Siri, Alexa and Google Assistant, but with more integration into Microsoft’s own apps. The mobile version, however, never caught on and Microsoft has since refocused on AI assistance built directly into its Microsoft 365 apps instead.

Google’s in-house incubator Area 120 launches Stack, an Android app that digitizes personal documents, IDs, receipts and more. It can then automatically name the files, extract key info (like the bill’s due date) and organize them, with help from Google’s DocAI technology. The app can also sync your scans to Google Drive for easy access.

Image Credits: Google

Amazon reports rising demand and engagement for productivity apps on Amazon Fire tablets. During 2020, the pandemic-fueled changes to work and home life led to a 62% increase in productivity by app users month over month across the tablet app store, and a 226% growth in app engagement amongst productivity customers in the last year. The company says it expects these trends to continue in 2021.

Government & Policy

Republicans on the House and Senate antitrust committees wrote letters to Apple, Google and Amazon, asking them about Parler’s removal from their respective platforms, framing it as targeting “one small business.” The tech companies had removed Parler for failing to follow their community guidelines over content and moderation after finding that the app had been used to plan, coordinate and facilitate the storming of the U.S. Capitol.

Apple’s App Store has been found to be hosting more than a dozen apps created by a China paramilitary group accused of Uyghur genocide, The Information reported. The organization, which has been sanctioned by the U.S. for human rights abuses, has published apps that offer news, info about government services and provides aid to small businesses with e-commerce orders, and more.

South Korea’s antitrust regulator said Wednesday it’s going to refer Apple’s local unit and one of its executives to the prosecution for allegedly impeding the regulator’s probe into unfair business practices. It also said it will fine Apple Korea 330 million won ($265,000 USD) for hampering the investigation.

Security & Privacy

The Odyssey Team announced the release of its new Taurine jailbreak for all devices running iOS 14-iOS 14.3. The jailbreak is installed using AltServer, similar to the unc0ver jailbreak.

A research report covered by Ars Technica found that Google collects up to 20x more data on Android users than Apple collects from iOS users. The report had analyzed the telemetry data transmitted directly to the companies themselves through pre-installed apps and when idle. Google disagreed with the report’s finding and says there were flaws in the researcher’s methodology that caused findings to be off by “an order of magnitude.”

The Washington Post covered a story about how an App Store scammer stole a user’s life savings, $600,000, in bitcoin. The user believed the app was safe because Apple markets its App Store as trustworthy, but the app itself had been designed to trick users by pretending to be associated with Trezor, the maker of a hardware device used to store cryptocurrencies. The actual Trezor said it’s been notifying Apple and Google for years about fake apps that were scamming its customers, to no avail. The fake app got through App Review then changed itself to a crypto wallet without Apple’s knowledge.

Funding and M&A

Image Credits: Cameo

Celebrity video request app Cameo raised $100 million in Series C funding in a round led by Jonathan Turner with e.ventures. The new funds value the business at just north of $1 billion.

Celebrity video request app Cameo raised $100 million in Series C funding in a round led by Jonathan Turner with e.ventures. The new funds value the business at just north of $1 billion.

Spotify acquired Betty Labs, the maker of the live audio app Locker Room with the goal of taking on Clubhouse. The app currently focuses on sports talk but will be expanded to cater to a wider range of fans and creators across “a range of sports, music, and cultural programming.” It will also add “a host of interactive features that enable creators to connect with audiences in real time,” like Clubhouse. The rise of live audio has offered a potential threat to Spotify’s investment in podcasts, as it connects users to audio programming in real time, instead of through recorded and produced shows. Spotify had earlier said it would add interactivity to its Anchor podcast recording app to better connect podcasters and listeners, but with the Locker Room sale it’s taking a further step towards fully embracing live audio.

Spotify acquired Betty Labs, the maker of the live audio app Locker Room with the goal of taking on Clubhouse. The app currently focuses on sports talk but will be expanded to cater to a wider range of fans and creators across “a range of sports, music, and cultural programming.” It will also add “a host of interactive features that enable creators to connect with audiences in real time,” like Clubhouse. The rise of live audio has offered a potential threat to Spotify’s investment in podcasts, as it connects users to audio programming in real time, instead of through recorded and produced shows. Spotify had earlier said it would add interactivity to its Anchor podcast recording app to better connect podcasters and listeners, but with the Locker Room sale it’s taking a further step towards fully embracing live audio.

Holler raised $36 million from CityRock Venture Partners and New General Market Partners to power “conversational media” in your favorite apps. The company works with partners like PayPal-owned Venmo and The Meet Group to bring AI-powered recommendations of GIFs and stickers to use when messaging in the apps. The content is monetized in partnership with companies like HBO Max, IKEA and Starbucks for branded stickers. Holler’s content now reaches 75 million users monthly, up from 19 million last year.

Madison-based Fetch Rewards raised a $210 million Series D for its customer loyalty and retail rewards app, valuing the business at more than $1 billion. The round was led by SoftBank through its Vision Fund 2, and makes Fetch Rewards one of the Midwest’s few unicorns. The app’s 7 million active users earn points by sharing photos of their receipts, which allows them to earn gift cards and participate in sweepstakes. The funding will help the company speed up its ability to process online receipts.

Funko, makers of pop culture collectibles, entered the NFT market by acquiring a majority stake in TokenWave, the makers of the TokenHead mobile app. The app allows users to showcase and track their NFT holdings, and today has over 10 million NFTs on display. Funko aims to launch its first NFTs in June, at starting prices of $9.99, with a unique property offered each week. Its products will be sold on the Worldwide Asset Exchange.

Chinese video streaming platform Bilibili invested HK$960 million (around $123 million USD) into X.D. Network, the makers of the game distribution platform TapTap, giving it a 4.72% stake in the company. X.D. is seen as a competitor with traditional game distributors in China, including the Android app stores operated by smartphone makers.

Chinese grocery app Nice Tuan raised $750 million from Alibaba, DST Global, and others to bolster its supply chain and increase its fresh produce offerings. The company today serves 1,598 cities and counties across China, and sees 15 million orders per day.

U.K.-based Nested raised an additional £5 million for its modern real estate agency that connects home buyers and agents using technology across web and mobile.

Expense tracking app Ensemble raised $3 million in seed funding for its app that helps divorced parents track shared expenses, like medical bills, extracurricular activities, transportation and other things that may fall outside of child support, which tends to cover just food, shelter and clothing needs.

China’s Q&A site Zhihu, a Quora rival, dropped 11% to the bottom of its marketed range following its $522.5 million U.S. IPO. The company is the largest Q&A community by average mobile monthly users and revenue, with 75.7 million MAUs in the last quarter.

China’s Q&A site Zhihu, a Quora rival, dropped 11% to the bottom of its marketed range following its $522.5 million U.S. IPO. The company is the largest Q&A community by average mobile monthly users and revenue, with 75.7 million MAUs in the last quarter.

Stockholm-based sport fishing app Fishbrain raised $31 million in funding for its mobile app that offers both a social network and social commerce platform for fishing with nearly 12 million registered users worldwide.

Indonesian investment app Ajaib added $65 million to its Series A, bringing the round to $90 million, in an extension led by Ribbit Capital — the fintech investor who also led Robinhood’s $3.4 billion round last month. This is its first investment in Southeast Asia.

Gaming startup Lowkey raises $7 million from Andreessen Horowitz for its app that allows gamers to both create and view short gaming clips. The company sees an opportunity in helping gamers cut down their existing content for distribution to short-form video platforms, like Instagram and TikTok.

Downloads

Smart Photo Widget

Image Credits: Cromulent Labs

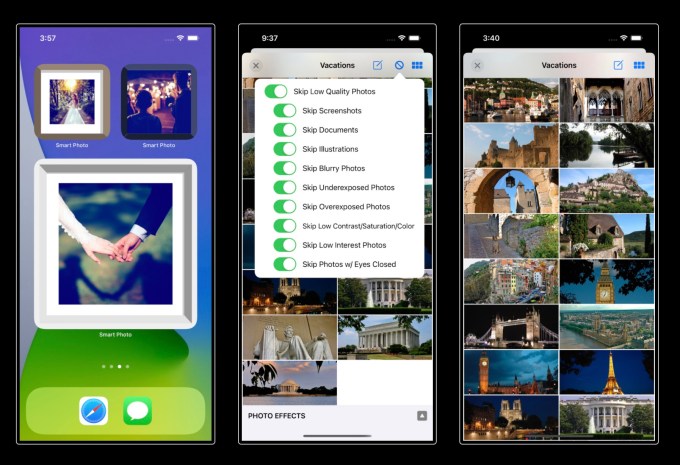

Cromulent Labs, the makers of Launcher and other apps, this week introduced a Smart Photo Widget that automatically frames each photo to fit the widget size you selected. You can also configure the widget to skip any bad photos from album (blurry, dark, screenshots, etc.) as it rotates through the best photos throughout the day. In the Premium version, you can add a date and time or other overlays and filter your photos to match your style. The app is free on iOS with in-app purchases.

Frenzic: Overtime (Soon)

Image Credits: Iconfactory

The popular app publisher and Twitterific developer Iconfactory announced on Friday it will soon launch Frenzic: Overtime, a sequel to the game that first launched on the iPhone App Store 13 years ago. The title will bring players over 45 levels with multiple gameplay modes and hundreds of mini-goals to achieve as they unlock the secrets of Frenzic Industries in this arcade style puzzler. The title will be available on Apple Arcade, but subscribers can already visit the game’s listing page and set a notification to be alerted to its launch.

SPIN Safe Browser

Image Credits: SPIN Safe Browser

A parental control app maker Boomerang, which continues to face App Review roadblocks, pivoted this year to develop safe browser technology. A new version of its SPIN Safe Browser designed for schools in need of filtering content was released this week. The app leverages AppConfig for content filter management through MDMs like Jamf School and Jamf Pro. Administrators can use the feature to enable or disable any of the categories as well as specific URLs that should be blocked or allowed.

Tweets

This is a story about how I lost $10,000,000 by doing something stupid.

Ten. Million. Dollars.

Literally up in smoke. Money bonfire.

That’s enough to retire with $250,000+ in annual income.

Here’s what happened…

— Andrew Wilkinson (@awilkinson) March 30, 2021

Ad-maggedon has started https://t.co/vhJ5oUrtGa

— Ouriel Ohayon (@OurielOhayon) April 2, 2021

really gotta teach my parents how to use emojis pic.twitter.com/KKSd38UCDT

— koby (@kobzilla_001) March 31, 2021